Dell Technologies (DELL.US) reported fiscal Q1 2027 results that reinforce its position as one of the biggest beneficiaries of the artificial intelligence boom. The server, data center infrastructure, and personal computer manufacturer delivered record revenue, explosive earnings growth, and significantly raised its full-year guidance. The company’s AI server business remains the primary growth engine, with management now expecting approximately $60 billion in annual AI server revenue. Results also demonstrate strong demand for traditional IT infrastructure, storage solutions, and enterprise PCs.

The market reaction was immediate, with Dell shares surging nearly 40% in after-hours trading after the company exceeded virtually every Wall Street expectation.

Key Highlights

-

Q1 revenue increased 88% year-over-year to a record $43.8 billion.

-

Adjusted EPS (non-GAAP) rose 214% year-over-year to $4.86.

-

AI server orders reached $24.4 billion during the quarter.

-

AI server revenue totaled $16.1 billion.

-

AI backlog expanded to a record $51.3 billion.

-

Dell raised its full-year revenue outlook to $165–169 billion, a new company record.

-

Management expects approximately $60 billion in AI server revenue during the current fiscal year.

-

Shares climbed nearly 40% following the earnings release.

AI Is Becoming Dell’s Largest Business

Just a few years ago, Dell was primarily associated with personal computers and enterprise hardware. Today, an increasingly large portion of its business revolves around infrastructure supporting artificial intelligence.

During the quarter, Dell secured $24.4 billion in AI server orders while generating $16.1 billion in AI server revenue. More importantly, the company ended the quarter with a record $51.3 billion backlog of AI-related orders.

According to COO Jeff Clarke, demand for AI solutions continues to accelerate. Management emphasized that the pipeline of potential projects remains several times larger than the current backlog. Dell’s customers include hyperscalers and compute providers such as CoreWeave and Nscale, as well as enterprises building private AI infrastructure and organizations developing their own AI models.

Financial Results Far Exceeded Expectations

Dell generated $43.8 billion in revenue during the first quarter, compared with $23.3 billion a year earlier. This significantly exceeded Wall Street consensus estimates of approximately $35.5 billion.

Profitability was even more impressive. Adjusted EPS reached $4.86, well above analyst expectations of $2.99.

Additional highlights include:

-

Operating income increased 154% to $4.2 billion.

-

Net income rose 194% to $3.2 billion.

-

Gross profit increased 57% to $7.9 billion.

These results show that Dell is not only selling more hardware but also benefiting from the higher-margin nature of AI infrastructure products.

AI Infrastructure Drives the Entire Data Center Business

The strongest-performing segment remains the Infrastructure Solutions Group (ISG), which includes servers, networking equipment, and storage systems.

ISG revenue surged 181% year-over-year to a record $29 billion, while operating income climbed 206% to $3.1 billion.

Importantly, growth is not limited to AI servers. Revenue from traditional servers and networking solutions increased 92% to $8.5 billion.

This reflects a broader wave of infrastructure modernization as large enterprises expand computing capacity and upgrade data centers to support AI workloads. Management also noted that the rise of AI inference and agent-based systems is increasing demand for traditional CPUs, which perform many supporting tasks alongside GPU accelerators.

Dell Is Building a Full AI Ecosystem

Dell’s strategy extends well beyond selling servers. The company is developing a comprehensive AI platform that includes infrastructure, storage, data management, and integrated solutions developed with strategic partners.

Current partnerships include:

-

NVIDIA

-

Google Cloud

-

OpenAI

-

xAI

-

Palantir

-

ServiceNow

-

Mistral

-

CrowdStrike

One of Dell’s flagship initiatives is Dell AI Factory with NVIDIA, which enables enterprises to deploy AI environments outside public cloud platforms.

This addresses a major industry trend as organizations increasingly adopt on-premises AI deployments due to concerns around data security, cost efficiency, and regulatory compliance.

The PC Business Is Also Returning to Growth

Although AI attracts most investor attention, Dell also delivered strong results in its traditional PC business.

Revenue from the Client Solutions Group (CSG) increased 17% to $14.6 billion.

The commercial PC segment generated $13 billion in revenue, up 18%, marking its seventh consecutive quarter of growth.

Management highlighted that a large portion of the global PC installed base is now more than four years old, creating a natural upgrade cycle. Additional demand is being driven by enterprise migration to Windows 11 and growing interest in AI-enabled PCs.

Supply, Not Demand, Is the Main Constraint

One of the most notable messages from management was that demand is no longer the limiting factor for growth.

Dell pointed to shortages of:

-

DRAM memory

-

NAND flash memory

-

Processors

-

Various data center components

According to Jeff Clarke, the company continues to operate in an inflationary environment and regularly adjusts pricing. At the same time, many customers are accelerating purchases to secure infrastructure capacity for several years ahead.

The situation resembles earlier stages of the cloud computing boom, when component shortages became the primary bottleneck for infrastructure providers.

Dell Raises Full-Year Guidance

Management significantly upgraded its financial outlook.

Dell now expects:

-

Revenue of $165–169 billion

-

Approximately $60 billion in AI server revenue

-

Adjusted EPS of roughly $17.90

In practical terms, this represents an increase of approximately $27 billion in projected revenue compared with previous guidance.

For the second quarter, Dell expects:

-

Revenue of $44–45 billion

-

AI server revenue of approximately $15.5 billion

Dell Is Emerging as One of the Biggest Winners of the AI Boom

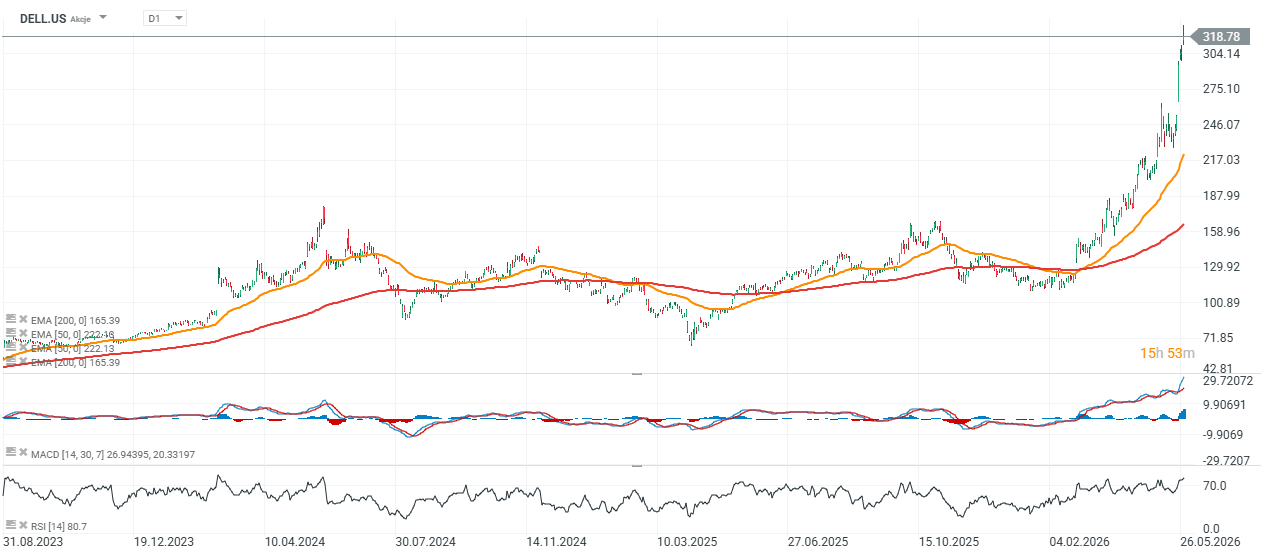

Not long ago, investors primarily viewed Dell as a personal computer manufacturer. The latest results demonstrate that the company has evolved into one of the most important infrastructure providers powering the AI ecosystem. A record backlog, accelerating growth across every major business segment, and management’s projection of $60 billion in AI revenue suggest that the generative AI investment cycle is still in its early stages. For Dell, the key challenge is no longer finding customers but securing enough components to fulfill the unprecedented volume of demand. As we can see on the chart - Dell shares surge significantly up almost 130% YTD, but opening 40% higher would signal even bigger YTR result, closer to 200% YTD gain.

Source: xStation5

US OPEN: Dell soars and keeps pushing tech stocks higher 🚀

EU50 near record highs: broad-based gains and buybacks support european equities 🔎

Daily Summary: Is the End of the War Drawing Near? (28.05.2026)

Nasdaq climbs on software rebound 📈 Is the Wall Street rally far from over?

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.