Wall Street is rebounding today on optimism around Axios reports about the finalization of a peace agreement between the U.S. and Iran, as well as strong macro data. The data helped ease inflation concerns, with month-on-month PCE coming in slightly below forecasts at 0.4% versus 0.5% expected, while also pointing to solid underlying conditions in the broader economy.

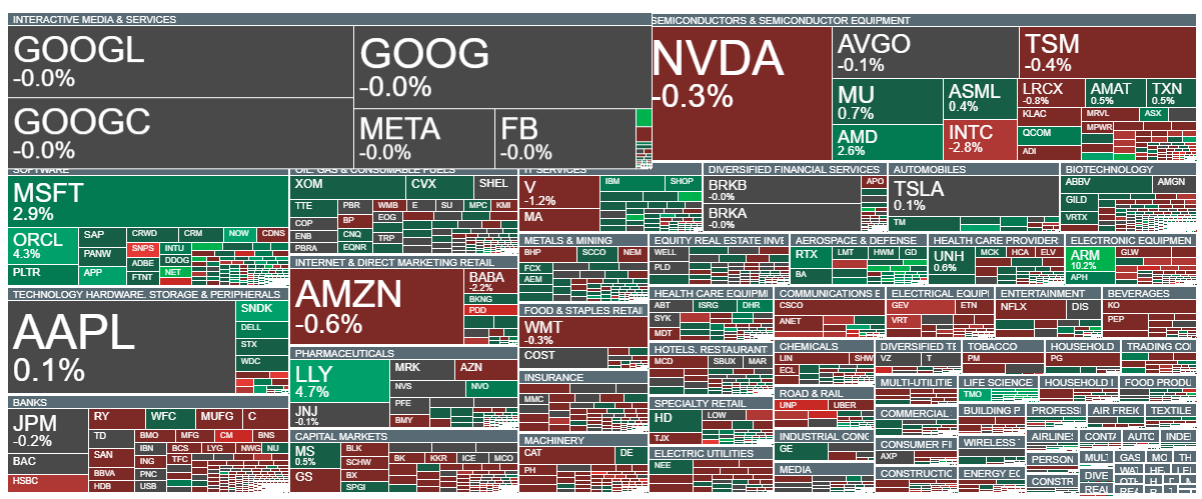

Microsoft is gaining after reports about the launch of new AI models, while the software sector is outperforming semiconductors, where names such as Intel and Nvidia are under pressure. Companies such as ServiceNow, Oracle, and NetApp are among today’s gainers.

On the other hand, Axios reports have already been repeatedly denied by Tehran in the past. This time appears similar. Shortly after the Axios publication, i24NEWS sources indicated that negotiations conducted by Iran’s Araghchi and U.S. envoy Witkoff ultimately failed to receive approval from Iran’s leadership. Iran’s spiritual leader, Mojtaba Khamenei, reportedly did not agree to proceed with the deal.

Markets, however, did not reverse their gains after these reports. The rally continued, supported by declining concerns over a potential rise in oil prices and inflation.

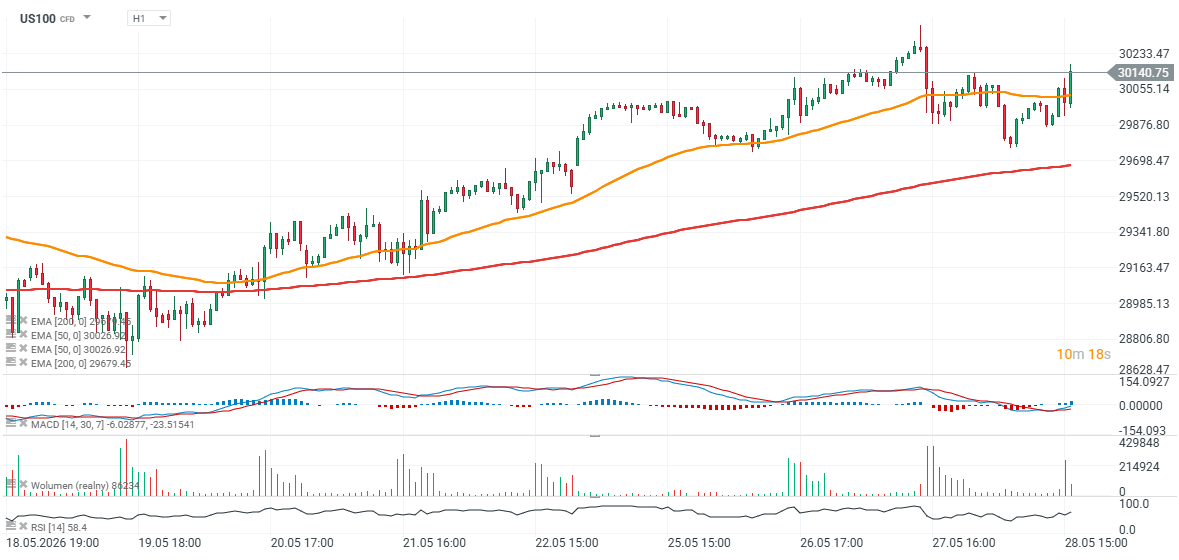

The Nasdaq 100 futures contract moved back above 30,000 points around one hour after the U.S. cash session opened and quickly erased the initial losses from the first part of the session. Key support is now around 29,700–29,900 points, while the main resistance zone remains near 30,400 points, around all-time highs.

Source: xStation5

Source: xStation5

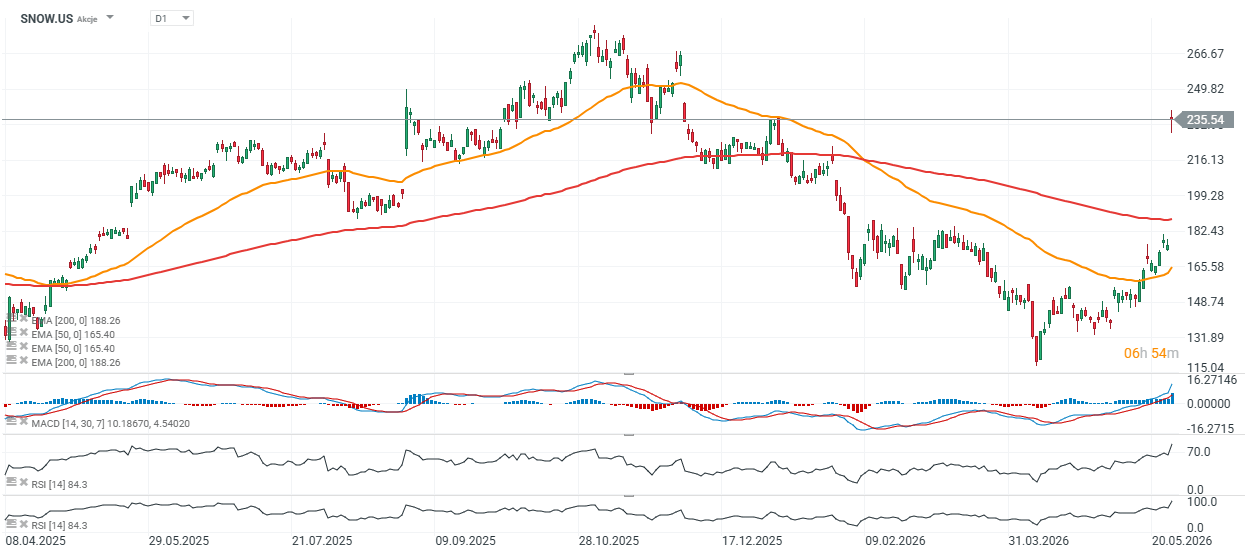

Snowflake surges 35% amid strong earnings and AWS deal

Snowflake (SNOW.US) shares are soaring in premarket trading after the AI-focused cloud data company delivered one of its strongest quarterly reports in recent years. The company not only beat Wall Street expectations on both revenue and earnings, but also raised guidance and announced a massive new $6 billion partnership expansion with Amazon Web Services (AWS). Investors interpreted the report as a strong signal that fears surrounding the so-called “SaaSpocalypse” may have been exaggerated.

Key facts

-

Snowflake reported Q1 FY2027 revenue of $1.39 billion, up 33% year-over-year.

-

Product revenue rose 34% YoY to $1.33 billion, accelerating from previous quarters.

-

EPS came in at $0.39 versus analyst expectations of around $0.32.

-

Q2 product revenue guidance of $1.415–1.42 billion exceeded Wall Street expectations of roughly $1.37 billion.

-

The company raised its full-year product revenue forecast to $5.84 billion.

-

Snowflake announced a new five-year, $6 billion infrastructure commitment with Amazon Web Services.

-

Shares surged more than 30% following the report, hitting a new year-to-date high.

AI growth is accelerating, not slowing

Management emphasized that artificial intelligence is becoming a major growth driver for the company. CEO Sridhar Ramaswamy described Q1 as a “clear inflection point” for Snowflake’s AI strategy, highlighting strong adoption of both the company’s core platform and its first-party AI products.

One of the most closely watched metrics — net revenue retention rate — improved to 126%, marking the first increase after several quarters of stagnation. This suggests existing customers are once again increasing spending at a faster pace.

Snowflake also noted that adoption of its AI assistant products more than doubled sequentially, reinforcing the view that enterprise customers are actively investing in AI-native software infrastructure.

Investors see Snowflake as a winner in the AI era

The results are particularly important because many investors had feared that generative AI could disrupt the traditional SaaS business model. Those concerns led to weakness across several software stocks over the past year.

Snowflake’s report challenges that narrative. Instead of AI replacing SaaS platforms, the company’s results suggest that businesses are actively looking for cloud-based AI data solutions capable of handling large-scale AI workloads and agentic AI applications.

The massive AWS agreement was also interpreted as a strong vote of confidence in future demand. Snowflake committed to spending $6 billion on Amazon infrastructure and AI chips over the next five years — a level of investment that signals management expects significant future growth in AI-related workloads.

Strong report, but valuation remains demanding

Despite the extremely bullish market reaction, some investors remain cautious about valuation. Following the rally, Snowflake trades at a very high price-to-sales multiple of around 17, leaving little room for operational disappointments. The company clearly appears to be entering a stronger growth phase again, supported by AI demand acceleration and improving customer spending trends. However, after such a sharp rally, much of the positive news may already be reflected in the stock price. For now, Snowflake’s earnings report represents one of the clearest signs yet that selected SaaS companies can still thrive - and potentially even accelerate growth — in the AI era.

Source: xStation5

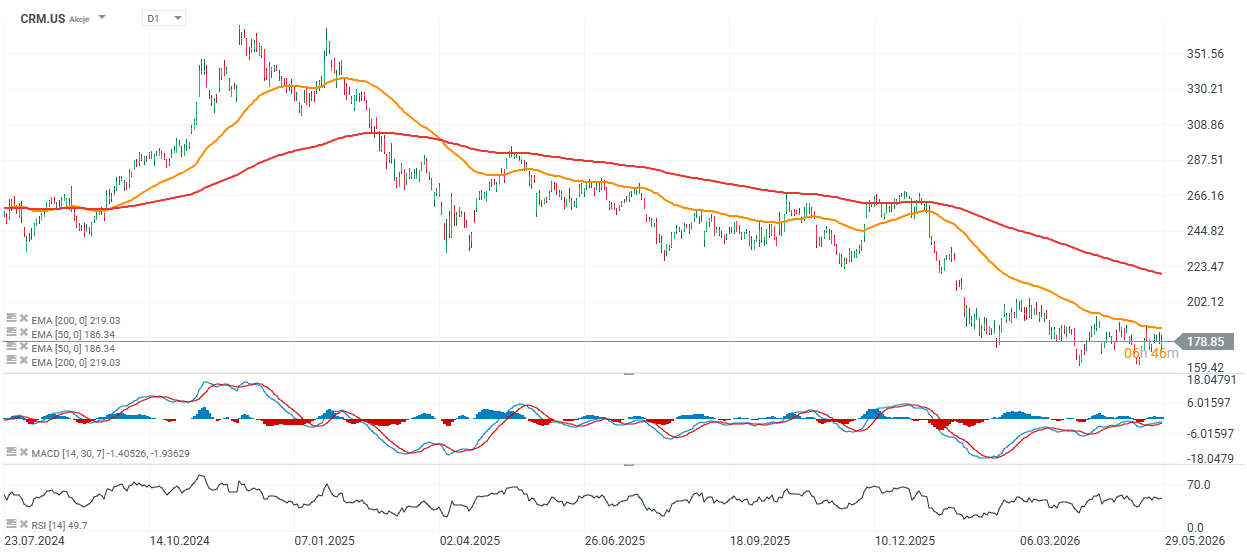

Salesforce shares react positively to a solid quarter - but risks remain in play

Salesforce (CRM.US) reported results that exceeded Wall Street expectations on both revenue and earnings, although the market reacted more cautiously to the company’s full-year guidance and weaker backlog metrics. At the same time, Salesforce showed very strong growth in its AI Agentforce business, with annualized revenue surpassing the $1 billion mark for the first time.

Key facts

-

Salesforce reported EPS of $3.88 versus expectations of $3.12.

-

Revenue came in at $11.13 billion compared to forecasts of $11.05 billion.

-

Revenue increased 13% year-over-year.

-

Net income rose to $2.11 billion from $1.54 billion a year earlier.

-

Agentforce annualized revenue reached $1.2 billion (+205% YoY).

-

Full-year revenue guidance came in slightly below market expectations.

-

Remaining Performance Obligation (RPO) totaled $67.9 billion versus expectations of $68.6 billion.

-

Shares were little changed following the earnings release.

AI is helping Salesforce, but the market remains cautious

The biggest focus for investors was the growth of Agentforce — Salesforce’s AI platform designed to automate sales and customer service processes. The company reported that Agentforce annualized revenue increased 205% year-over-year to $1.2 billion, surpassing the billion-dollar threshold for the first time.

CEO Marc Benioff emphasized that AI is becoming an increasingly important growth driver for Salesforce, while Slack and generative AI tools are being used more frequently in large enterprise contracts.

At the same time, investors remain cautious toward the broader software sector. The market continues to worry that AI could disrupt the traditional SaaS business model and pressure the long-term growth outlook for major software companies.

Guidance and backlog slightly disappointed

Despite strong quarterly results, Salesforce issued full-year revenue guidance that came in slightly below Wall Street expectations.

The company expects FY2026 revenue in the range of $45.9–46.2 billion, versus analyst consensus of around $46.12 billion. The guidance reflects:

-

weaker performance in the marketing and commerce segment,

-

deteriorating Tableau trends,

-

increased volatility following the Informatica acquisition.

Investors also reacted negatively to the Remaining Performance Obligation (RPO) figure, which measures contracted future revenue. The metric came in at $67.9 billion versus market expectations of $68.6 billion.

Salesforce continues investing aggressively in AI and Slack

Salesforce continues to aggressively expand its AI business while further integrating Slack, which the company acquired in 2020 for more than $27 billion.

Marc Benioff highlighted that Slack was involved in nearly half of Salesforce’s contracts worth more than $1 million during the latest quarter. The CEO also suggested that Slack could eventually become a business generating as much as $10 billion in annual recurring revenue.

The company is also increasing headcount primarily in sales, arguing that despite the rise of AI agents, traditional sales teams remain essential for expanding its enterprise business.

The market is still trying to determine whether AI will help or hurt SaaS

Salesforce’s results show that AI can simultaneously support growth for major software platforms while also creating concerns about the future of the SaaS model itself. On one hand, Agentforce is growing rapidly and AI is increasing usage of Salesforce products. On the other hand, investors remain concerned about slowing growth in traditional software segments and rising competitive pressure tied to generative AI. For now, Salesforce’s earnings report can be viewed as operationally solid, but not strong enough to completely shift investors’ cautious stance toward large SaaS companies.

Source: xStation5

Daily Summary: Is the End of the War Drawing Near? (28.05.2026)

NATGAS up by 6%

BREAKING: Crude oil inventories higher than expected

🚨BREAKING: Axios reports that the USA and Iran have reached an agreement, but still need Trump's final approval

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.