- ตลาดคาดการณ์ว่าการลดอัตราดอกเบี้ยของสหรัฐฯ จะถูกเลื่อนออกไปนานขึ้น

- กิจกรรมทางธุรกิจและการใช้จ่ายของผู้บริโภคยังคงสนับสนุนการขยายตัวของเศรษฐกิจ ทำให้ความเสี่ยงเงินเฟ้อฟื้นตัวมีสูงขึ้น

- ในขณะเดียวกัน ตลาดแรงงานดูเหมือนจะเริ่มทรงตัว ส่งผลให้นโยบายของเฟดเข้าใกล้ สมดุลความเสี่ยง มากขึ้น

- ตลาดคาดการณ์ว่าการลดอัตราดอกเบี้ยของสหรัฐฯ จะถูกเลื่อนออกไปนานขึ้น

- กิจกรรมทางธุรกิจและการใช้จ่ายของผู้บริโภคยังคงสนับสนุนการขยายตัวของเศรษฐกิจ ทำให้ความเสี่ยงเงินเฟ้อฟื้นตัวมีสูงขึ้น

- ในขณะเดียวกัน ตลาดแรงงานดูเหมือนจะเริ่มทรงตัว ส่งผลให้นโยบายของเฟดเข้าใกล้ สมดุลความเสี่ยง มากขึ้น

พรุ่งนี้ 20:00 น. CET

เฟดจะประกาศอัตราดอกเบี้ยครั้งแรกของปี 2026

-

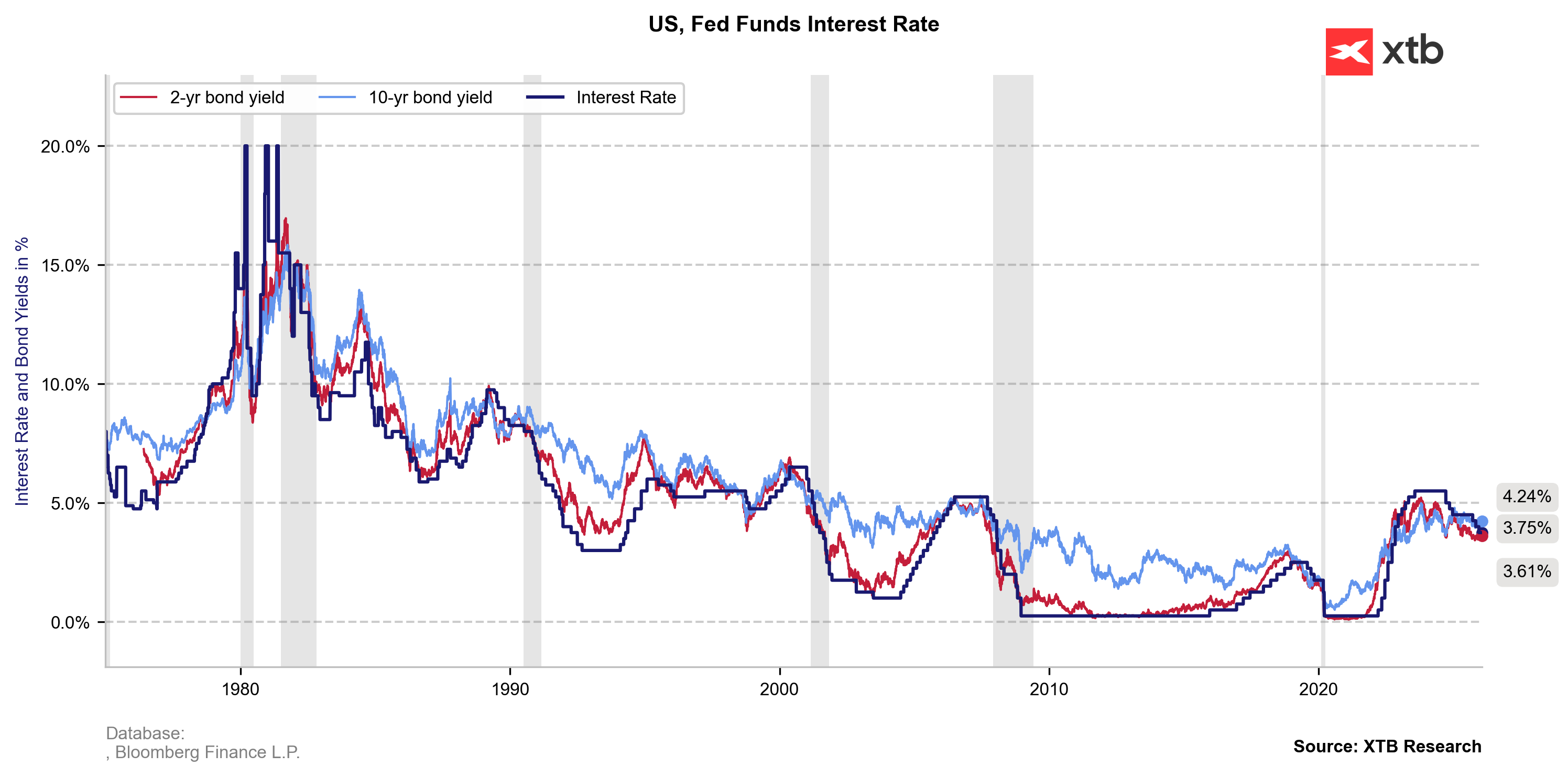

หลังการลดดอกเบี้ย 25 bp ในเดือนธันวาคม สู่ช่วง 3.50–3.75%

-

ตลาดแทบไม่คาดหวังมาตรการผ่อนคลายเพิ่มเติมแล้ว

-

คาดว่าเฟดจะ ไม่ลดดอกเบี้ย ในการประชุม FOMC ครั้งนี้ และอาจ คงอัตราดอกเบี้ยยาวไปจนถึงครึ่งหลังของปี 2026

คำถามสำคัญ: นโยบายเฟดกลับสู่ระดับ เป็นกลาง (neutral) แล้วหรือยัง?

Two-year Treasury yields have risen about 10 bps since the start of the year, signaling a clear increase in medium-term rate expectations. Source: XTB Research

The economy is accelerating with inflation near 3%

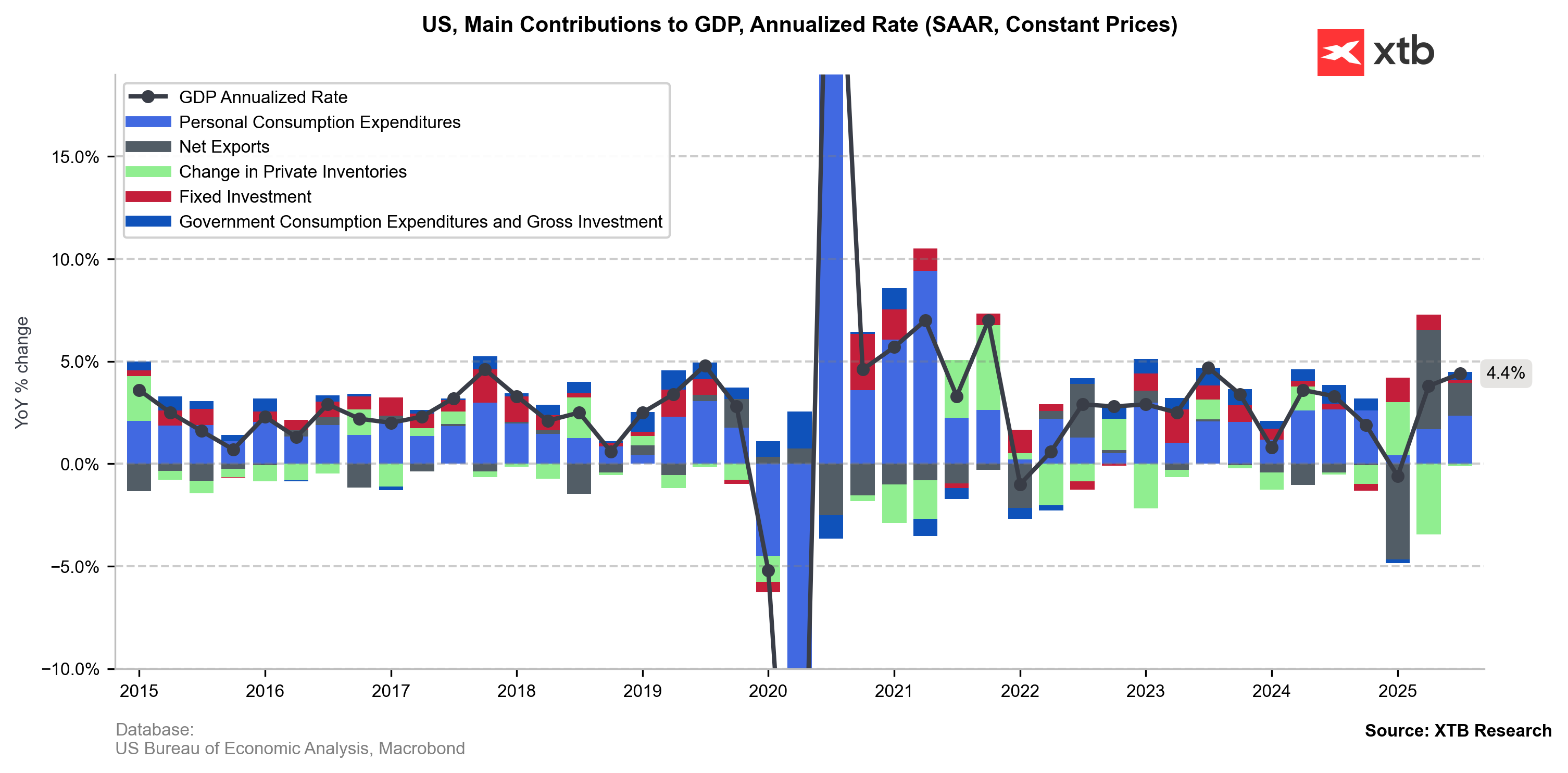

Recent U.S. data point to stronger-than-expected economic activity, which in 2025 had been dampened by uncertainty surrounding Donald Trump’s tariff policy. The latest upward GDP revision may not have been spectacular (from 4.3% to 4.4%), but it sent an optimistic signal that both consumers and businesses navigated a turbulent period, defined by rising costs (especially medical and food), restrained capital spending and fears of a labor market downturn.

The Q3 2025 GDP revision confirmed that consumer demand remains the main growth driver and revealed stronger-than-expected business investment. This dual optimism poses a risk for sticky inflation, which is once again approaching 3%. Source: XTB Research

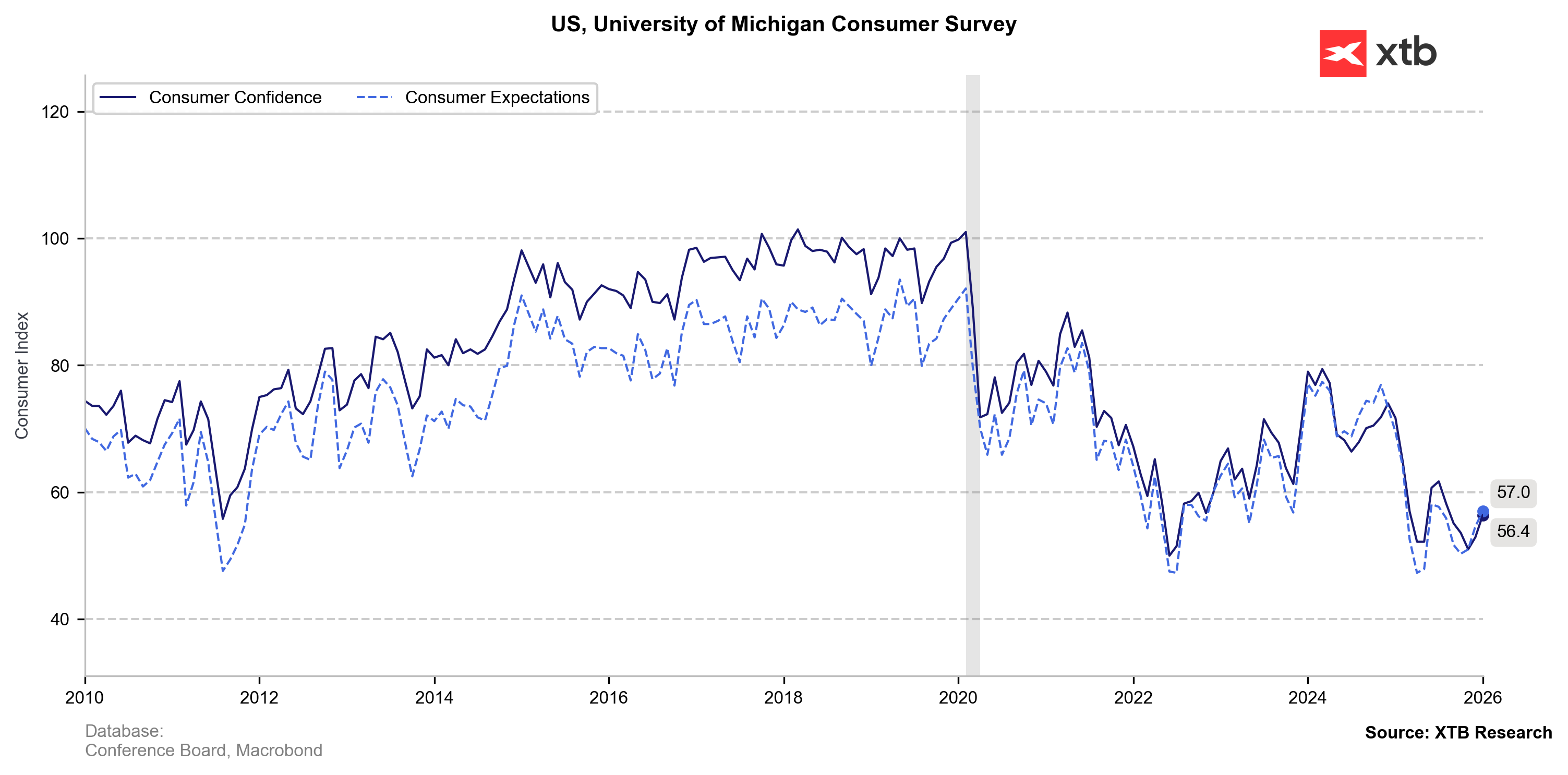

High-frequency data tell a similar story. The University of Michigan consumer sentiment index rose for a second straight month (from 52.9 in December to 56.4 in January), matching an increase in consumer spending (PCE) of +0.5% m/m in both October and November. Americans are also becoming less cautious, saving less despite recent labor market tensions and the government shutdown (savings rate fell from 3.7% in October to 3.5% in November; January 2025: 5.1%).

ความเชื่อมั่นผู้บริโภคสหรัฐฯ ฟื้นตัวจากจุดต่ำสุดล่าสุด

ที่มา: XTB Research

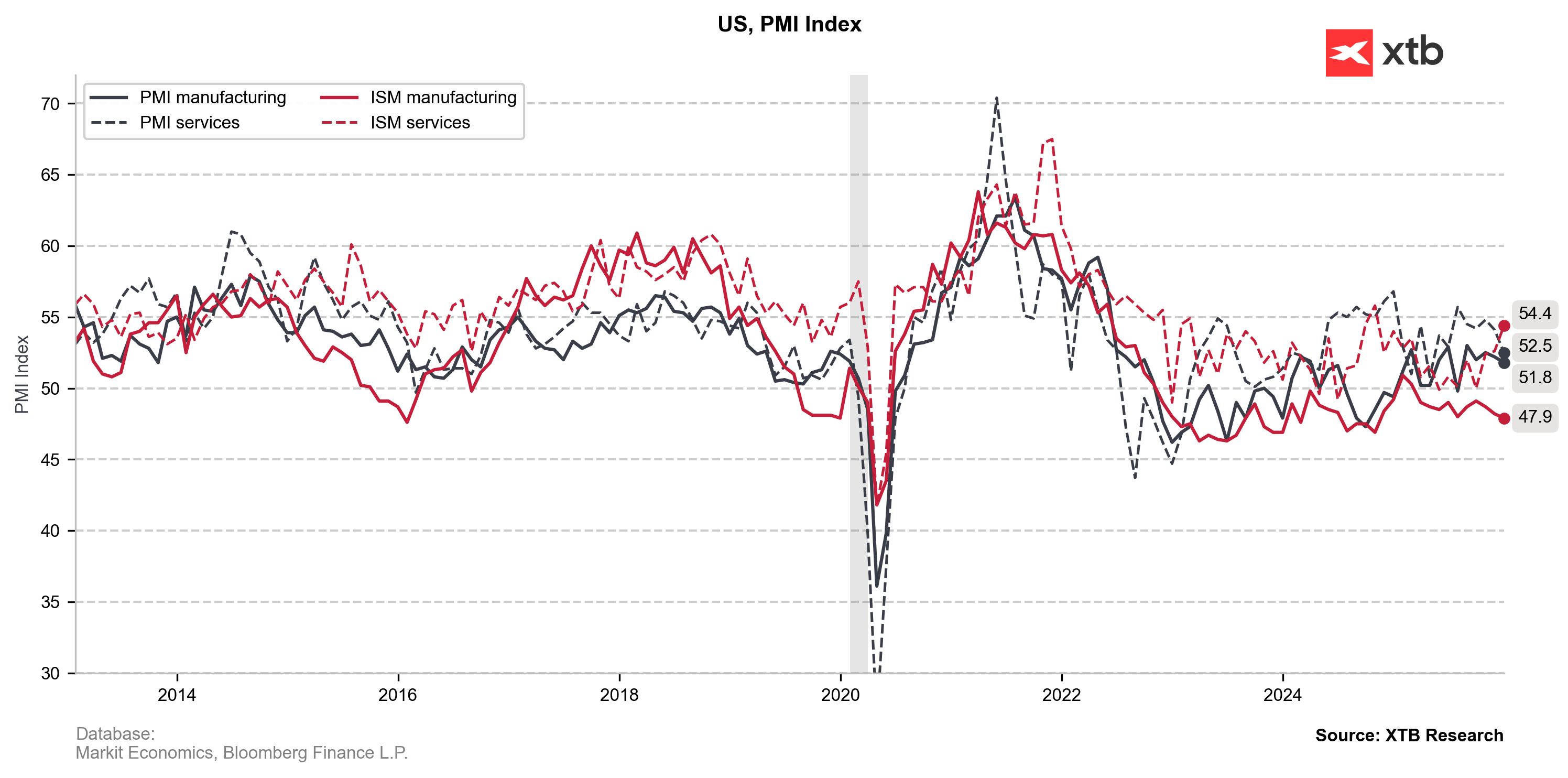

ควบคู่ไปกับความเชื่อมั่นด้านอุปสงค์ที่แข็งแกร่ง กิจกรรมเศรษฐกิจในภาคสำคัญของสหรัฐฯ เพิ่มขึ้น

-

ภาคบริการ โดดเด่นที่สุด โดยรายงาน ISM ล่าสุดชี้การขยายตัวเร็วที่สุดตั้งแต่เดือนตุลาคม 2024 (ISM Services: 54.5)

-

11 จาก 16 ภาคเศรษฐกิจ รายงานการเติบโตสูงสุด นำโดย ค้าปลีก, การเงิน, และที่พัก/บริการอาหาร

→ สะท้อนความเชื่อมั่นที่กว้างขวาง ไม่ได้พึ่งเฉพาะภาคเทคโนโลยี

ภาคการผลิต ยังคงหดตัว (ISM Manufacturing: 47.9) แต่มีสัดส่วนต่อ GDP และผลกระทบต่อเงินเฟ้อค่อนข้างจำกัด

ดัชนี PMI และ ISM ของสหรัฐฯ

ที่มา: XTB Research

ทั้งภาค การผลิต และ บริการ มีจุดร่วมสำคัญคือ แรงกดดันด้านราคาอย่างต่อเนื่อง ส่วนใหญ่เกิดจาก อัตราภาษีของ Trump

-

ธุรกิจรายงานความตึงตัวจาก อุปสงค์สูง และ ต้นทุนแรงงาน-วัตถุดิบที่เพิ่มขึ้น

-

ราคาที่ตอบสนองต่อภาษีในปี 2025 ยังไม่ชัดเจน เนื่องจาก สินค้าคงคลังระดับสูง ที่สะสมตั้งแต่ปี 2021–2022, 2024 และก่อนการเก็บภาษีตอบโต้ใน 2025

-

แบฟเฟอร์นี้จำกัด → คาดว่า ราคาสินค้าอาจปรับสูงขึ้นในปี 2026

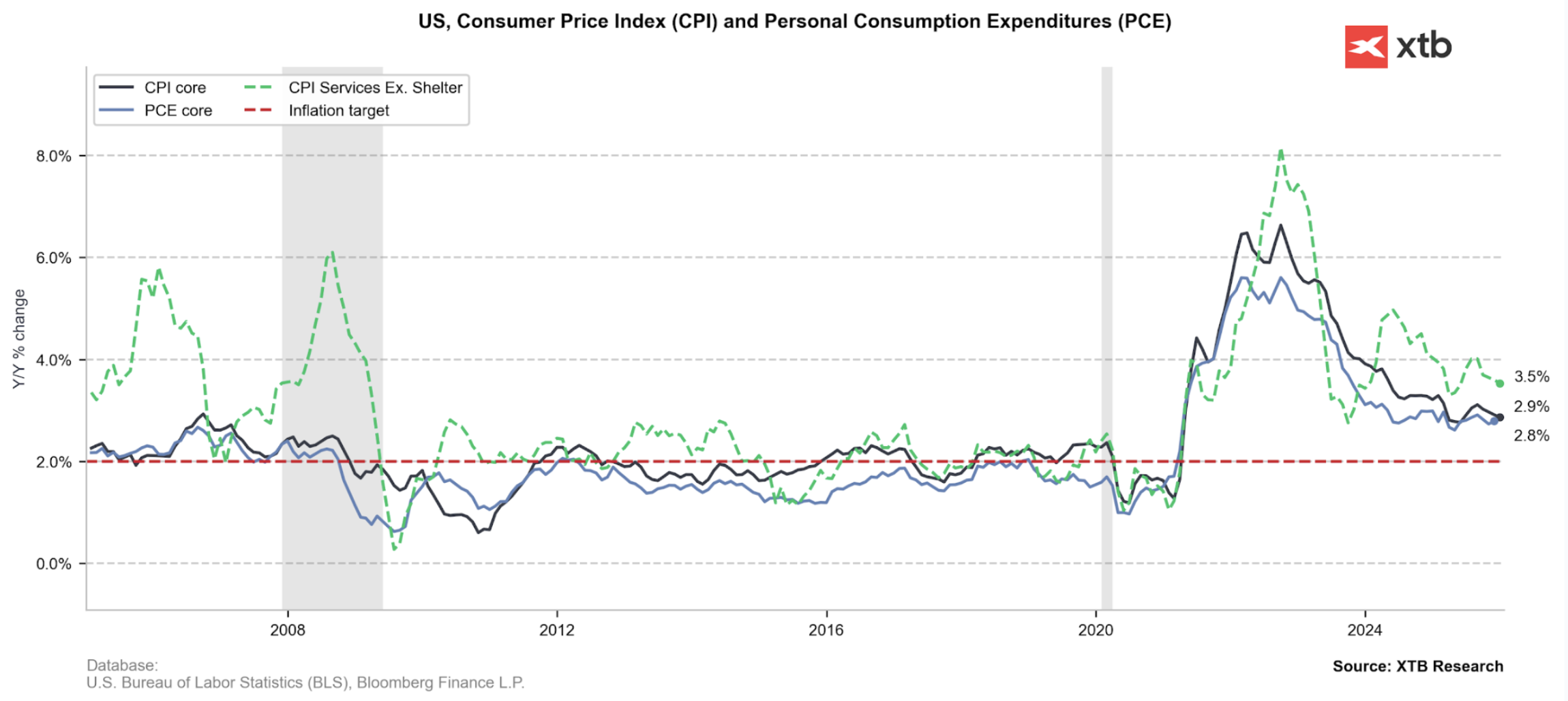

เงินเฟ้อ Core PCE ของสหรัฐฯ

-

กลับมาที่ 2.8% ในเดือนพฤศจิกายน

-

การถ่ายโอนภาษีเพิ่มเติม (tariff pass-through) ร่วมกับกิจกรรมเศรษฐกิจที่แข็งแกร่ง เพิ่มความเสี่ยงที่เงินเฟ้อจะกลับขึ้นใกล้ 3%

ที่มา: XTB Research

ตลาดแรงงานเริ่มมีความชัดเจนมากขึ้น

-

ตลาดแรงงานสหรัฐฯ ยังอยู่ในโหมด “ไม่จ้าง ไม่ปลด” แต่ข้อมูลโดยรวมช่วยลดความกังวลเฟดต่อการล่มสลายของการจ้างงานฉับพลัน

-

รายงาน ISM แสดงองค์ประกอบการจ้างงานที่ดีขึ้นทั้งในภาคการผลิต (ชะลอการลดลง) และบริการ (ปรับเพิ่มครั้งแรกตั้งแต่พฤษภาคม 2025) → สะท้อน แรงจ้างงานเริ่มฟื้นตัวอย่างค่อยเป็นค่อยไป

-

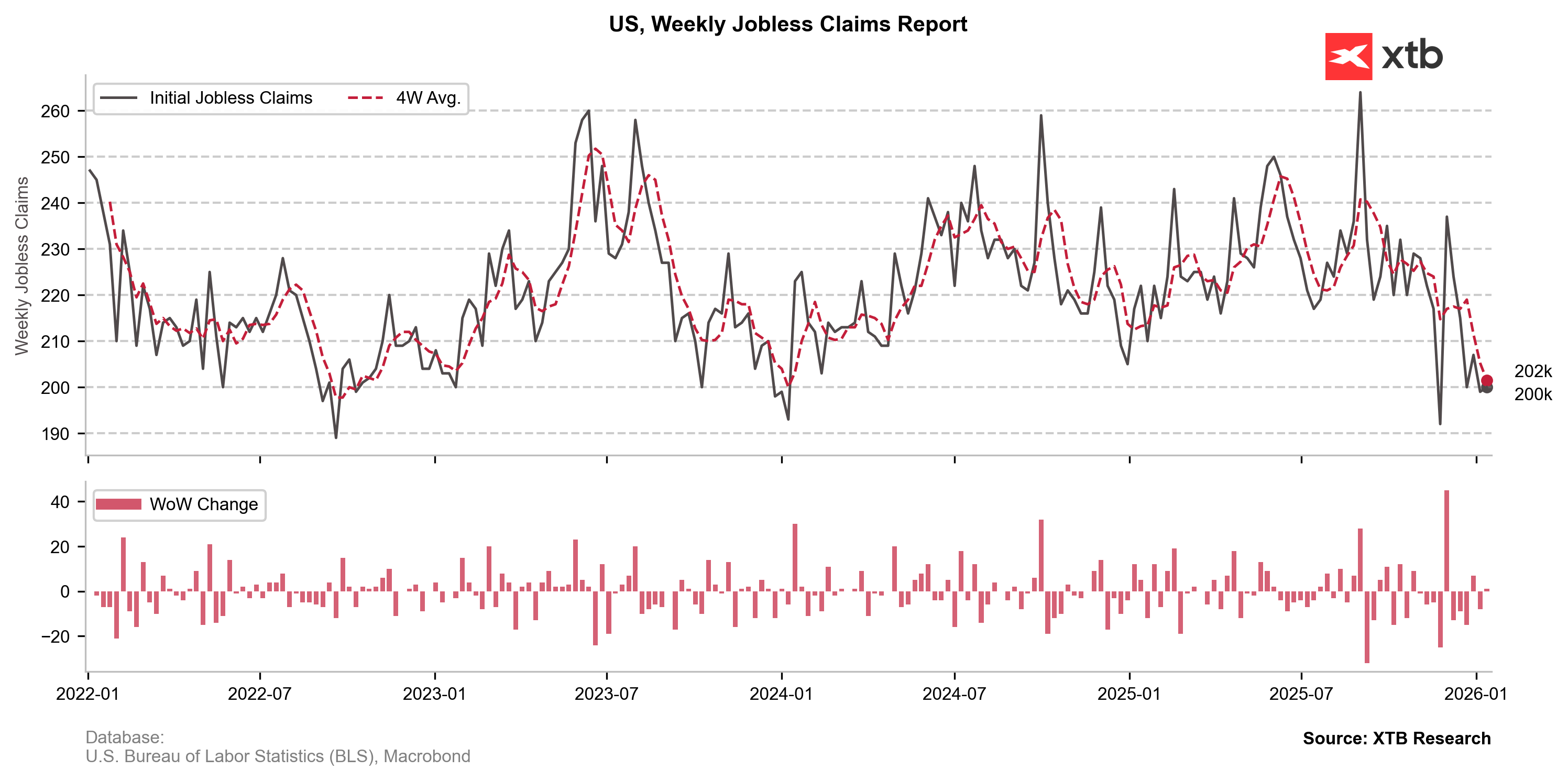

Initial jobless claims ลดลงอย่างมาก แม้มีความวุ่นวายในภาครัฐ ปัจจุบันอยู่ใกล้ระดับต่ำสุดของปี 2022 และ 2024 (~200k)

-

แนวโน้มนี้สนับสนุน อัตราการว่างงานลดลงอย่างไม่คาดคิด จาก 4.5% → 4.4%

-

ข้อมูล NFP ไม่มีทิศทางชัดเจน แต่ไม่ได้สัญญาณการสูญเสียงานจำนวนมาก

-

ตัวเลขล่าสุดต่ำกว่าคาด (50k vs 66k)

-

แต่ การเติบโตงานสุทธิใน Q4 2025 ยังคงเป็นบวก แม้จะมีการหยุดจ้างชัดเจน

-

The sharp downtrend in jobless claims should reduce fears of a renewed rise in unemployment. Source: XTB Research

“Soft” arguments for a more hawkish Fed

Beyond hard macro data, sentiment within the Fed may turn more hawkish due to recent political developments. The U.S. Department of Justice proceedings against Jerome Powell are widely viewed as an unprecedented challenge to central bank independence. This atmosphere alone encourages greater caution in adjusting rates, to avoid any perception that the Fed is bowing to White House pressure.

Another reason for the Fed’s “wait mode” is data quality. The longest government shutdown in history raises concerns about noise in recent data releases, especially CPI. The FOMC may argue that waiting carries less risk than acting on potentially distorted data.

Summary

Core PCE inflation hovering just below 3% should once again draw the Fed’s attention. While economic activity and sentiment had previously been subdued, allowing the Fed to focus on labor market uncertainty, the risk balance now appears even, and rates look closer to neutral. As disinflation slows near target, the Fed is likely to keep rates at current levels at least this quarter to guard against a renewed inflation pickup.

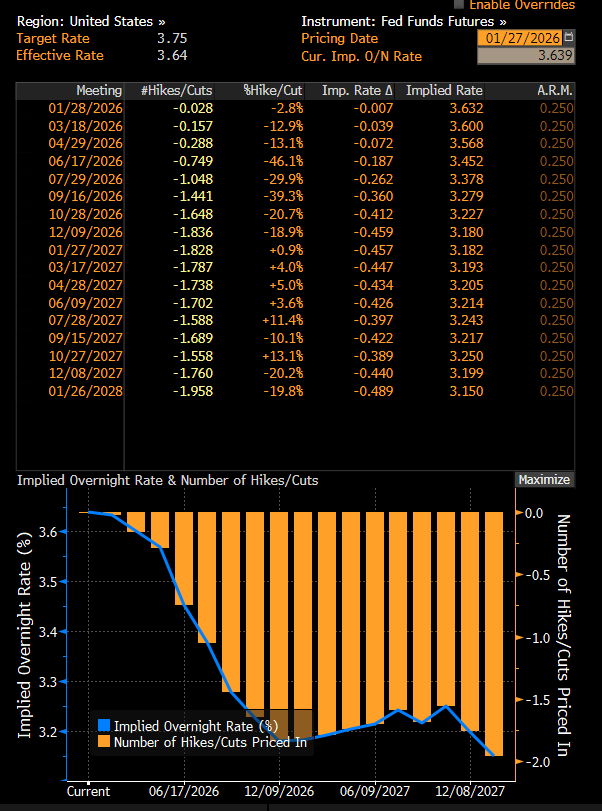

The futures market now fully prices the first U.S. rate cut only in July 2026. Source: Bloomberg Finance LP

Aleksander Jablonski

Quant Analyst XTB

US500 ทำระดับสูงสุดก่อน Fed 🗽 BigTech จะยังหนุนต่อได้ไหม?

ทองคำพุ่งแรง 2% ทดสอบระดับ $5,300 ท่ามกลางการอ่อนค่าของดอลลาร์สหรัฐ 📈

AUDUSD: RBA จะกลับมาขึ้นดอกเบี้ยหรือไม่?

ปฏิทินเศรษฐกิจ: การตัดสินใจของเฟด – ตลาดปรับลดคาดการณ์การลดดอกเบี้ยลงอย่างรวดเร็ว 🔎