The European stock market extended losses today in response to Donald Trump’s unilateral declaration, imposing 30% tariffs on all European goods, effective August 1st. Most of the major indices are trading in the red, with German DAX leading losses (-0.85%) due to high exposure of the German industrial sector to American levies. French CAC40 (-0.4%), Italian FTSE MIB (-0.05%), Swiss SMI (-0.2%) and Spanish IBX35 (0.25%) are all recording losses, with British FTSE 100 (+0.4%) and Polish WIG20 (+0.2%) being the main exceptions.

The EU has warned that President Trump’s threat could effectively end transatlantic trade, making current trade levels “almost impossible.” With EU-US trade worth nearly €1.7 trillion last year, the bloc is pushing for a negotiated solution and has delayed planned retaliatory tariffs on $25 billion of US exports.

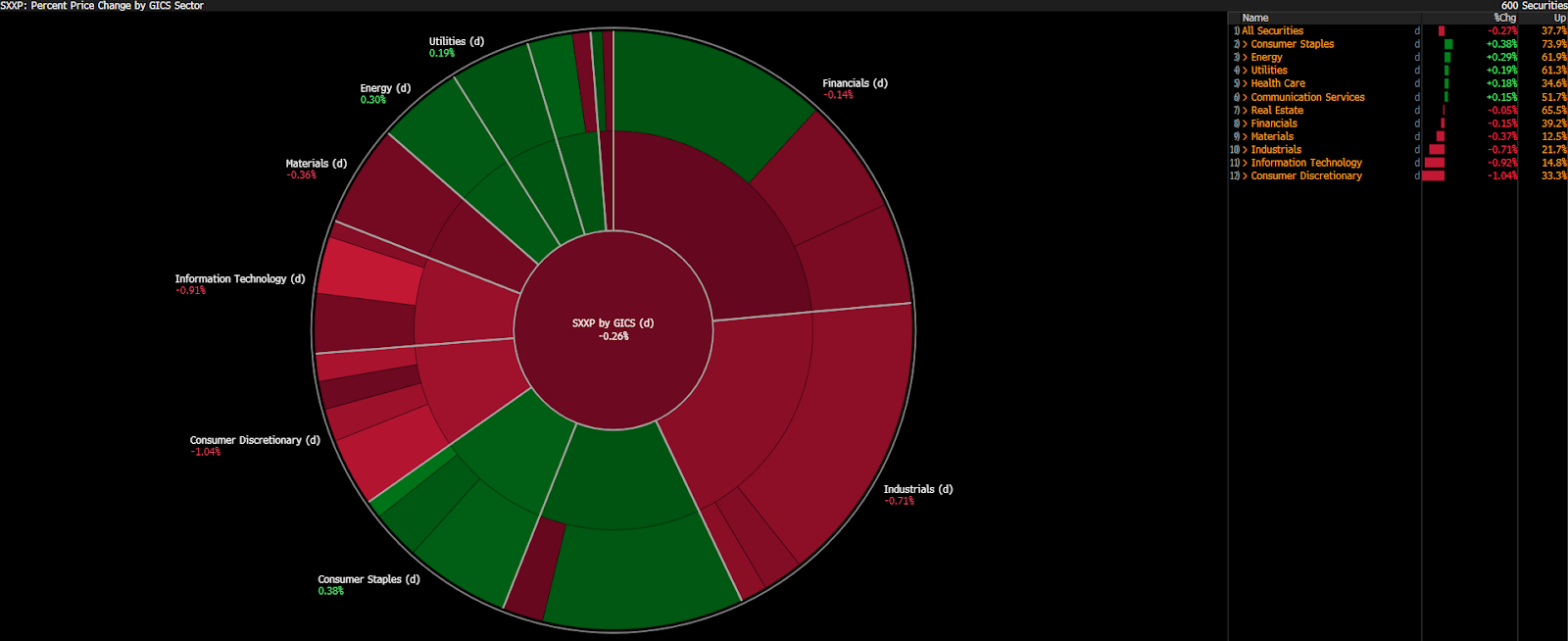

Among Euro Stoxx 600 sectors, consumer discretionary goods stocks sink the most, especially the German automotive sector (BMW: -1.75%, Mercedes-Benz: -1.5%, Volkswagen: -1.45%, Porsche: -1%), as well as the German tech big caps (SAP: -1.4%, Infineon: -1.9%). Similar weakness is visible in French luxury stocks (LVMH: -1.6%, Kering: -1.2%, Dior: -1.75%). Aside from energy-related companies, some resilience is posted by major healthcare stocks (Astra Zeneca: +1.4%, Sanofi: +0.17%, Bayer: +0.6%, Novo Nordisk: +0.1%).

Discretionary consumer goods stocks take the largest hit today, as automotive companies lead losses in the face of Trump’s aggressive move regarding levies on European goods. Source: Bloomberg Finance LP

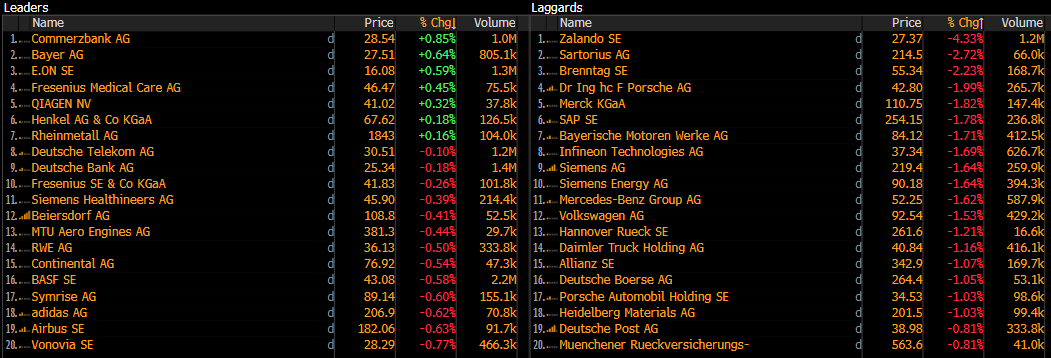

Today’s performance of DAX-listed companies. Source: Bloomberg Finance LP

DE40 (D1)

DAX futures are down for a third consecutive session, weighed by the 30% tariffs on European goods announced by Donald Trump last Saturday. The DE40 contract has now reached the 38.2% Fibonacci retracement level, which is acting as key support. Worth noting, the contract only briefly dipped below its 30-day exponential moving average (EMA100, dark purple), despite heightened uncertainty throughout the negotiation period, signaling an underlying resilience. With the tariff negotiation deadline approaching and tensions between Trump and the European Commission unresolved, further downside pressure is likely. However, if the proposed levies are scaled back—potentially to levels seen around Liberation Day or lower—we could see a rebound toward historical highs.

Source: xStation5

Company news:

-

BASF (BAS.DE) shares are down 0.4% after it cut its 2025 guidance, a move widely expected by analysts who viewed it as a realistic reset. While EBITDA forecasts were lowered to €7.3–€7.7 billion, strong free cash flow and better performance from higher-value units offered reassurance. Analysts see the revised outlook as credible, reducing the risk of further downgrades.

-

Brenntag (BNR.DE) shares dropped over 4.4% after an unscheduled cut to its full-year EBITA guidance, driven by weaker demand, FX headwinds, and pricing pressure. While the downgrade was partly expected, the scale surprised the market, with preliminary Q2 results missing estimates and the outlook for the second half clouded by ongoing macroeconomic and geopolitical uncertainty.

-

A Milan court placed Loro Piana under judicial administration for one year amid an investigation into alleged labor exploitation by its suppliers. Reports say the luxury brand, owned by LVMH (MC.FR), is accused of indirectly supporting illegal labor practices. LVMH has declined to comment, and Loro Piana has not responded. LVMH's shares are down 1.7%

-

Saab’s (SAABB.SE) Gripen fighter jet is seeing renewed export interest as European defense budgets grow amid geopolitical tensions. With potential deals in Thailand, Colombia, and beyond, Gripen's lower lifecycle costs and independence from U.S. suppliers make it attractive to buyers rethinking reliance on American-made arms. Saab sees this as the strongest sales momentum in years. Shares are up 0.15%.

หุ้นเด่นรายสัปดาห์ – Jabil Inc

Broadcom (AVGO.US) หุ้นร่วง 5% แม้รายงานผลประกอบการแข็งแกร่งและความต้องการ AI สูง 🗽

สรุปข่าวเช้า

ข่าวเด่นวันนี้