-

Strong turnaround in LVMH's earnings and a 13% jump in share prices at the opening after a quarterly surprise.

-

Sales growth in the China region and exceeding forecasts in most segments.

-

Positive outlook for 2026 thanks to improving trends in Asia and stabilizing demand in the US and Europe.

-

Strong turnaround in LVMH's earnings and a 13% jump in share prices at the opening after a quarterly surprise.

-

Sales growth in the China region and exceeding forecasts in most segments.

-

Positive outlook for 2026 thanks to improving trends in Asia and stabilizing demand in the US and Europe.

LVMH (MC.FR) latest quarterly report has delivered a surprisingly positive turnaround, suggesting luxury fashion may be winning back investor favor. After two quarters of declines, LVMH (MC.FR) halted the trend of weakening demand for high-end goods, posting 1% organic sales growth and a marked improvement in key business segments—most notably strong demand at Moët & Chandon and Dior. This surprise triggered a more than 13% spike in share price at market open, briefly leading to a trading halt due to rapid volatility.

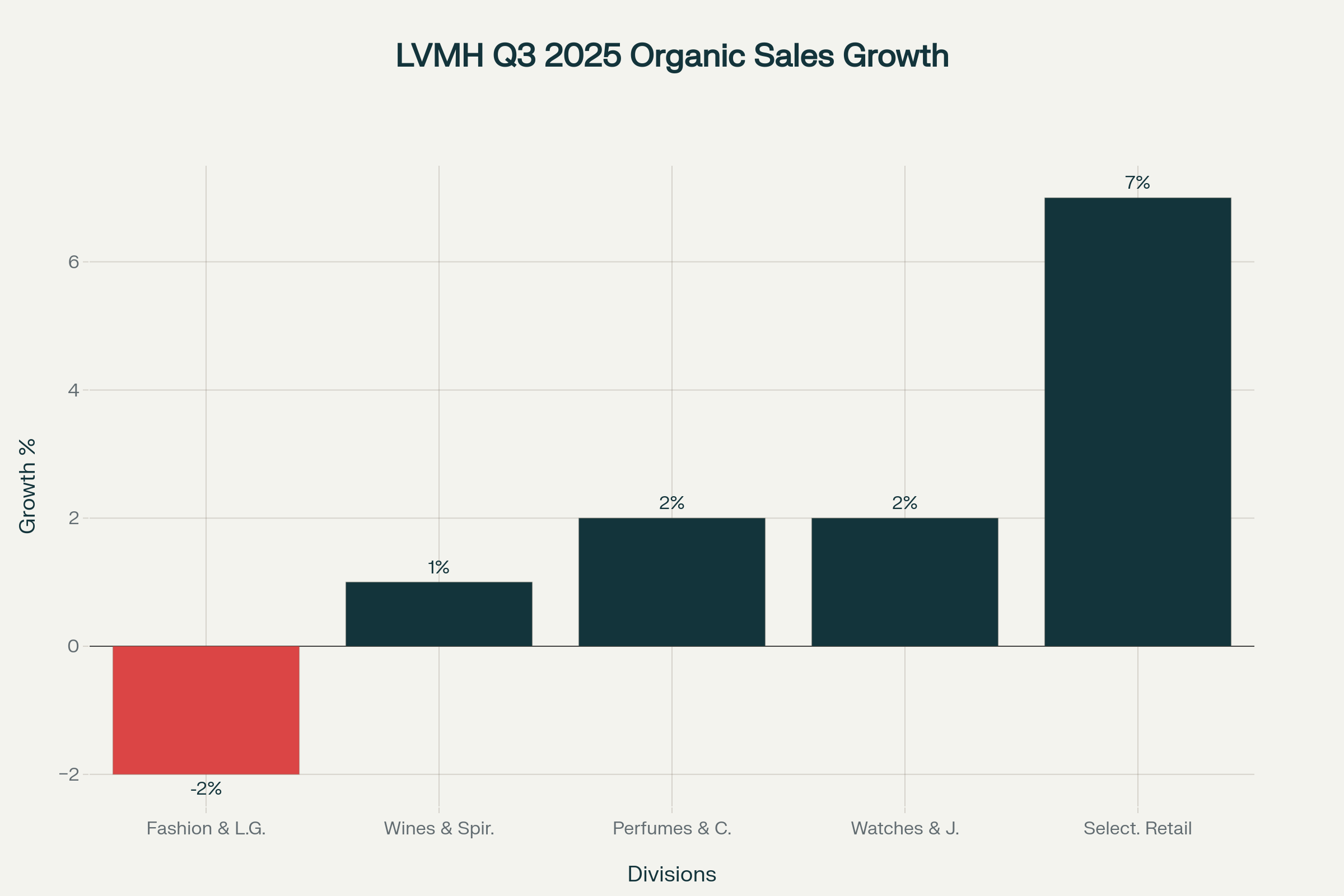

Third-quarter results also highlighted improvement in regions that previously saw declines. In China, sales rose 2% after a prior 9% drop in the first half, seen as an early sign of recovery (also backed by today’s CPI data from China showing increased demand for luxury jewelry despite ongoing general deflation). All divisions outperformed analyst expectations, with fashion & leather goods falling less than forecast (-2% vs. -3.5%).

Key results and forecasts:

-

LVMH Q3 revenue: €18.28bn (+1% y/y; forecast: -0.72%)

-

Fashion & Leather Goods: -2% (forecast: -3.48%), revenue €8.50bn (-7.1% y/y)

-

Wines & Spirits: +1% (forecast: -3.18%), revenue €1.33bn (-4% y/y)

-

Perfumes & Cosmetics: +2% (forecast: +1.73%), revenue €1.96bn (-2.7% y/y)

-

Watches & Jewelry: +2% (forecast: +1.05%), revenue €2.32bn (-2.8% y/y)

-

Selective Retailing: +7% (forecast: +4.61%), revenue €3.99bn (+1.7% y/y)

-

US sales: +3% (forecast: +1.93%)

-

Asia ex-Japan: +2% (forecast: -3.63%)

-

Europe: -2% (forecast: +1.5%)

-

Analysts (JP Morgan, Morgan Stanley) are forecasting continued improvement, with a possible return to sustained growth in 2026, driven especially by a rebound in Chinese demand and stabilization in the US and European markets.

LVMH organic sales growth by division, Q3 2025. Source: XTB

Outlook:

Management and leading analysts point to a gradual recovery, with the strongest rebound in Asia ex-Japan (mainly China, a key market for luxury), and continued growth potential fueled by high post-pandemic savings among Chinese consumers. Management cautions that the Q4 comparison base will be tougher, but strong brand visibility at events like those for Louis Vuitton and Dior supports a positive outlook for next year. Expectations are that 2026 will offer easier year-over-year comparisons, providing a solid foundation for the global luxury sector to rebound.

LVMH's latest quarterly results and the dynamic growth of the company's share price clearly indicate that the fashion and luxury sector may be returning to favor with investors after a period of uncertainty and decline. LVMH's reversal of the negative trend, illustrated by a 13% jump in its share price, is a strong signal, especially as the improvement in sales is also visible in key segments and demanding markets such as China.

Importantly, the rebound is not limited to the Parisian giant. In recent days, other companies in the industry, such as Kering, have also recorded solid growth. Until recently, the improvement in sentiment was mainly explained by short-term speculation on a rebound, but new data from LVMH shows that the turnaround in valuations is also driven by real, better-than-expected financial results.

LVMH Q3 2025: Organic sales growth by region (actual vs. forecast). Source: XTB

LVMH shares started trading today with a clear upward gap and broke back above their 200-day exponential moving average, which previously acted as a major resistance level in the stock’s downtrend. Source: xStation

TSMC Earnings Preview: Will the Key Semiconductor Supplier Surprise the Market?

US Open: American Indices Rally on Anticipated End of Fed Balance Sheet Reduction

Bank of America, Wells Fargo, and Morgan Stanley: Q3 2025 Earnings Overview

Abbott reports no surprises in Q3, but tariff risks and lowered forecasts drag the share price down💡

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.