Today at 4:00 PM CET, Kevin Warsh will be addressing the U.S. Congress, reporting on the monetary policy conducted by the Fed. It is worth noting that the text of the speech was published earlier, which has not necessarily been the case in recent years. Kevin Warsh's first appearance before the House of Representatives will go down in history, not only for the tribute paid to the recently deceased Alan Greenspan. Warsh presents himself as a reformer who, on the one hand, wants a tough monetary policy to get rid of persistent inflation, and on the other, is launching a deep, structural revision of the Fed's existing operating methods.

Key Points from Kevin Warsh's Address

- Absolute Priority, i.e., the End of Inflation: Warsh declared that if the Fed conducts policy properly (and he is convinced that it will), the five-year period of elevated inflation will become history. In the text of the speech, he emphasized that long-term inflation depends almost exclusively on monetary policy, and the Fed has "zero tolerance" for its elevated level.

- Interest Rates Unchanged: During the June FOMC meeting, rates were maintained at 3.50% – 3.75%.

- Economy Strong, but Uneven: Household consumption is growing moderately, and industrial production is steadily climbing. The real estate sector, however, remains the weak point.

- AI-Driven Investment Boom: Spending on modern technologies is increasing at a rapid pace. Investment in equipment grew by 8% year-on-year, and spending on the technology sector soared by almost 25%. According to Warsh, the strong productivity growth is due to the implementation of artificial intelligence.

- Stable Labor Market: Unemployment remains low, layoffs are limited, and nominal wage growth is solid and keeping pace with the influx of new workers.

- Major Audit of the Federal Reserve: Warsh appointed as many as 5 special task forces to verify the fundamentals of the Fed's operations:

- Market Communication (whether the current method of announcing decisions makes sense).

- Balance Sheet Policy (including an analysis of the so-called abundant reserves system)

- Data Methodology (access to more accurate real-time data).

- The Impact of AI on Productivity and Employment.

- Inflation Models (checking whether the Fed's existing economic theories still work).

- Optimism with a Note of Caution: The latest inflation data (both core and consumer) were lower than expected, which pleases the Fed. However, Warsh warns that the ongoing war and high oil prices could quickly reverse this positive trend.

Commentary on the Address Text

Kevin Warsh's address signals a significant change in communication from the Fed. The appointment of five task forces (including those for the balance sheet and inflation models) shows that the new head is rejecting old dogmas in favor of flexibility and real-time data analysis. This means that, for example, today's lower inflation reading may be crucial when the central bank makes short-term decisions.

The current interest rate range with an upper level of 3.75% will likely remain with us for longer. Falling inflation eliminates the need for further hikes, but geopolitical risks and a strong economy block quick cuts. Crucially, the AI revolution and the surge in technological investment are driving productivity, allowing the US to grow without causing new inflationary pressure. On the other hand, AI poses a threat to energy-related inflation, but this may primarily have a short-term effect that should not be of great significance to the central bank.

For the dollar, this is a good, though not necessarily the best, arrangement. On the one hand, the dollar still has no alternative, and investors do not have a clear view on where monetary policy in the US is heading. Nevertheless, maintaining the current level of interest rates and the market's still-high expectations for hikes will limit the currency's weakness. A sell-off of the dollar may occur when the risk of an energy shock subsides, although it is difficult to say when such a situation would happen.

It is worth remembering that after the text is read, we will have a series of questions from congressmen, and tomorrow the same statement will be read before the Senate committee.

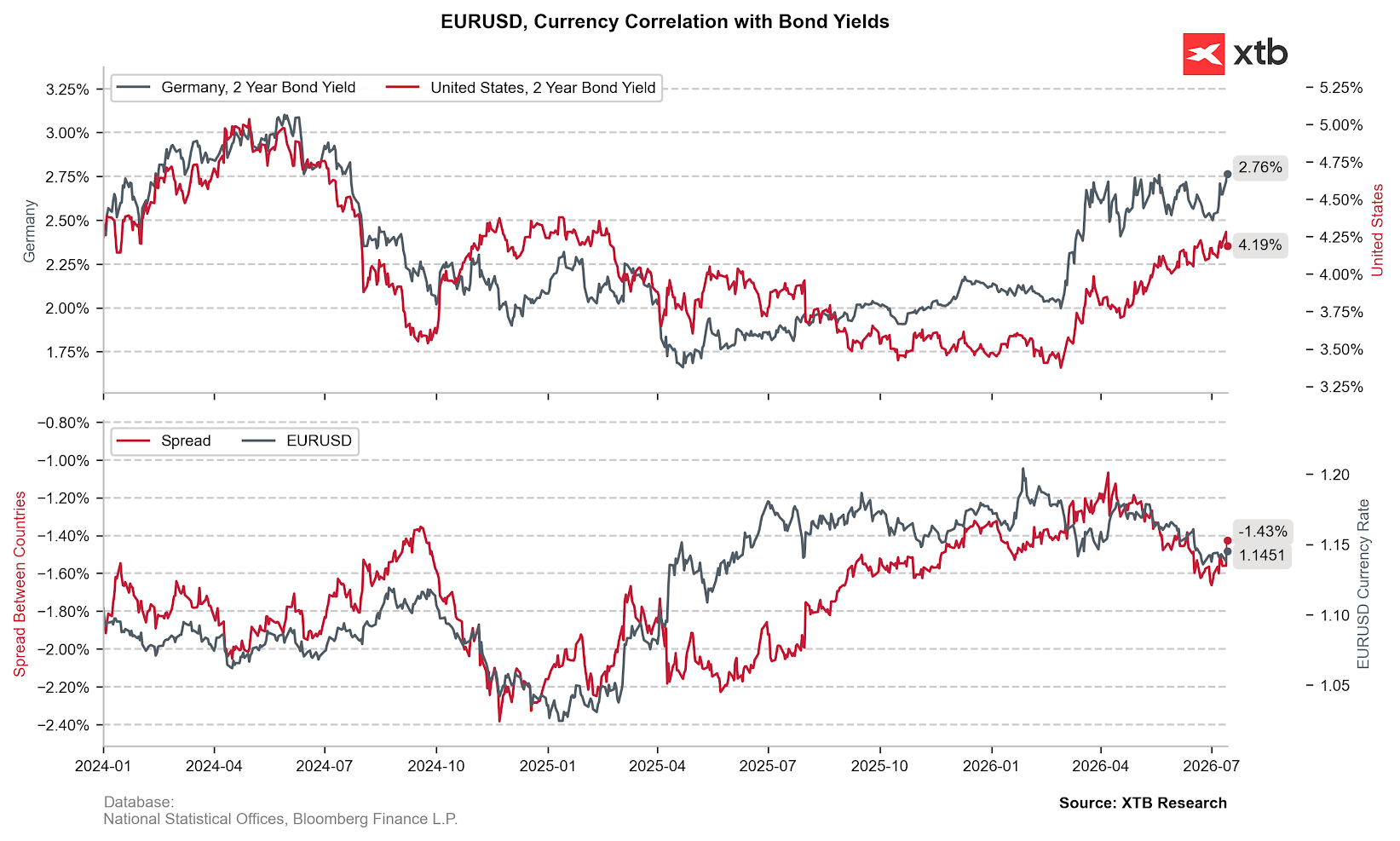

It is worth noting that despite the growing expectations for US rates, 2-year yields remain relatively calm, though at an elevated level. On the other hand, yields in Germany are rising to the highest levels since mid-2024, signaling greater pressure on the ECB to raise interest rates. The yield spread may indicate that in the short term, EURUSD may be slightly undervalued, but it will largely react primarily to the behavior of the US debt market. Source: Bloomberg Finance LP, XTB

It is worth noting that despite the growing expectations for US rates, 2-year yields remain relatively calm, though at an elevated level. On the other hand, yields in Germany are rising to the highest levels since mid-2024, signaling greater pressure on the ECB to raise interest rates. The yield spread may indicate that in the short term, EURUSD may be slightly undervalued, but it will largely react primarily to the behavior of the US debt market. Source: Bloomberg Finance LP, XTB

Daily Summary: Lower inflation weakens the dollar and awakens gold and S&P 500 to gains

Fed Chair Kevin Warsh’s Q&A from Congress Testimony: Inflation stability is a key

Bypassing Hormuz: Gulf States Race Against Time

Time to test the strength of the dollar