- Australia’s CPI inflation came in at 4.6% YoY in March 2026, according to ABS data, remaining well above the RBA’s 2–3% target range. Core inflation measures also remain elevated, suggesting that price pressures are not limited to the most volatile components.

- The labour market continues to give the RBA room to tighten, with unemployment holding at 4.3% and participation remaining high. However, the key risk for the RBA is persistent services inflation, which may remain sticky even as goods disinflation progresses.

- The global backdrop has deteriorated due to increased volatility in energy markets, particularly following escalating tensions in the Middle East and disruptions to oil supply routes. Higher energy prices could push inflation higher again in Q2, especially through fuel, transport, and broader production costs.

- According to T. Rowe Price, the RBA is likely to prefer acting sooner to limit second-round effects and prevent inflation expectations from rising. Ahead of the decision, markets were pricing a 75% probability of a 25 bps hike and around 2.5 additional hikes by the end of 2026.

- VanEck, in turn, assessed the hike as a “foregone conclusion,” noting that inflation had already been sticky even before the escalation in Middle East tensions. Anthony Malouf from Ebury argued that the case for tightening was clear: inflation remains elevated and the labour market continues to show resilience.

Trimmed mean inflation remains at 3.3%, reinforcing the view that domestic price pressures are still too high for the RBA. Employment growth remains solid, driven largely by full-time jobs, reducing the risk of an immediate slowdown following the rate hike. The RBA remains in inflation-fighting mode, with the rate path now largely dependent on energy prices, services inflation, and labour market resilience.

Summary (RBA – post-decision and Governor Bullock’s remarks)

- The RBA points to a structural supply problem in the economy, with activity approaching capacity constraints.

- The central bank emphasizes the need to cool demand to better align it with limited supply.

- Real wage growth is seen as a risk factor that could hinder the return of inflation to target if it remains too strong.

- The RBA signals that earlier excess demand relative to supply was a key driver of tightening, even before the Middle East conflict.

- The central bank highlights the role of fiscal policy, noting that additional government support for households may make it harder to dampen demand.

- The labour market remains tight, with employment expected to continue growing despite tighter monetary policy.

- The RBA stresses that its mandate includes both inflation and full employment, but the balance between them depends on prevailing macro risks.

- Currently, greater emphasis is placed on controlling inflation, while still monitoring labour market risks.

- The RBA acknowledges that further rate hikes are burdensome for households, but inflation is also eroding real incomes.

- Inflation is projected to peak around 4.8% in June, although the outlook remains uncertain due to geopolitical developments.

- The oil shock has increased inflationary pressure, spilling over into other sectors through higher energy and transport costs.

- Even if oil prices decline, inflationary effects are expected to persist for some time.

- The RBA suggests that without the Middle East conflict, the rate path could have been less restrictive, but current conditions require a tighter stance.

- Rising fuel prices are reducing real household incomes, worsening overall economic conditions.

- The central bank acknowledges recession risks if the conflict is prolonged but stresses these will be assessed continuously.

- Monetary policy implication: the RBA remains data-dependent and flexible, ready to adjust its stance depending on the balance between inflation, growth, and the labour market.

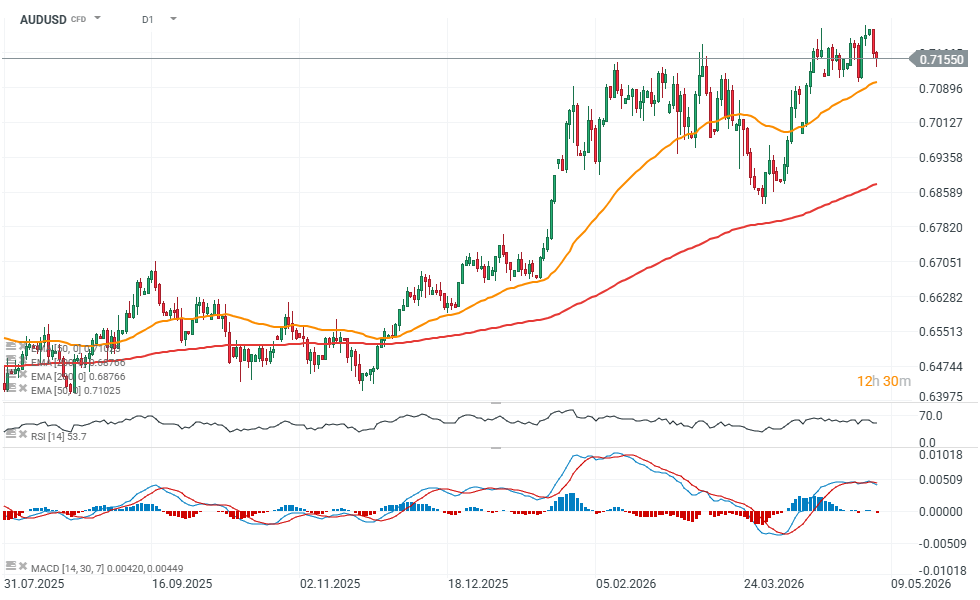

AUDUSD chart (D1)

Source: xStation5

Oil Prices Fall: Renewed Hopes for the Opening of the Strait of Hormuz

Economic Calendar: The US, the UK, and parts of Europe will be closed for trading 💡 (25.05.2026)

Morning Wrap: Geopolitical Risk-On After the Weekend🟩 (25.05. 2026)

💯Daily Summary - Wall Street Close to Records Ahead of Long Weekend

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.