🌍 GEOPOLITICS – Strait of Hormuz / Iran

-

The US–Iran conflict remains the main driver of the markets. On Saturday, Trump announced that an agreement on opening the Strait of Hormuz was “largely negotiated” and that the deal would be announced shortly. However, on Sunday he reversed his stance, saying that there was no rush and that the naval blockade would remain in place until the agreement had been signed and ratified.

-

Secretary of State Rubio confirmed that a “substantial proposal” regarding the reopening of the Strait is on the table, emphasising that diplomacy will be given every opportunity before alternatives are considered. Physical evidence of a partial reopening: two LNG tankers have left the Strait of Hormuz bound for Pakistan and China, and a supertanker carrying Iraqi oil for China left the Gulf on Saturday after being stranded for almost three months.

🏦 MACRO / CENTRAL BANKS

-

The new Fed Chair, Kevin Warsh, has taken office against a backdrop of stagflation – the markets are fully pricing in a 25-basis-point rate hike in January 2027, which marks a dramatic reversal from expectations prior to the outbreak of the conflict (two cuts in 2026). US consumer sentiment fell to record lows in May against a backdrop of rising fuel prices.

-

Lagarde has signalled a revision of the ECB’s inflation forecasts ahead of the 11 June meeting – the market is closely watching to see whether the ECB will adjust its interest rate path in the face of the energy shock. The NZIER recommends that the RBNZ keep rates at 2.25% this week (27 May), but indicates that rises are likely in the coming quarters.

-

The PBOC set the USD/CNY fixing at 6.8318 – a significantly stronger yuan than market estimates (6.7880) – which is seen as a subtle signal of support for the Chinese currency’s appreciation. Singapore beat GDP growth forecasts for Q1, and the local central bank, the MAS, signalled a stabilisation in interest rate policy, although the Ministry of Trade is warning of risks from the Middle East.

📈 MARKETS – OVERVIEW

-

Risk-on sentiment dominated the start of the week: S&P 500 futures are up +0.7%, Nasdaq futures +1.2%, and gold is gaining +1.4% on a weaker dollar. On Friday, the Dow Jones closed at a record high of 50,579 points (+0.58%), the S&P 500 at 7,473 points (+0.37%) and the Nasdaq at 26,343 points (+0.19%).

-

Note on market liquidity – markets are closed today in the US (Memorial Day), the UK (Spring Bank Holiday), Hong Kong and South Korea. Some European stock exchanges are also observing Whit Monday (Germany, France, Switzerland, Austria), although Euronext and Xetra will be open – the Swiss stock exchange will be closed. Thin liquidity could dramatically amplify any news from Tehran or Washington.

🌏 ASIA

-

The Nikkei 225 hit a record high, successively breaking through the 64,000 and 65,000-point marks – closing at 65,263 points (+3.04%). This was a direct reaction to the fall in oil prices and progress in talks with Iran. Taiwan’s Taiex also reached an all-time high above 43,000 points (+2.91%).

-

The Australian ASX 200 rose by +0.47%, the Chinese CSI 300 rose by +0.91%, and the Indian Nifty 50 rose by +1.03%. There are no major economic releases scheduled for Asia today – no significant data is due.

-

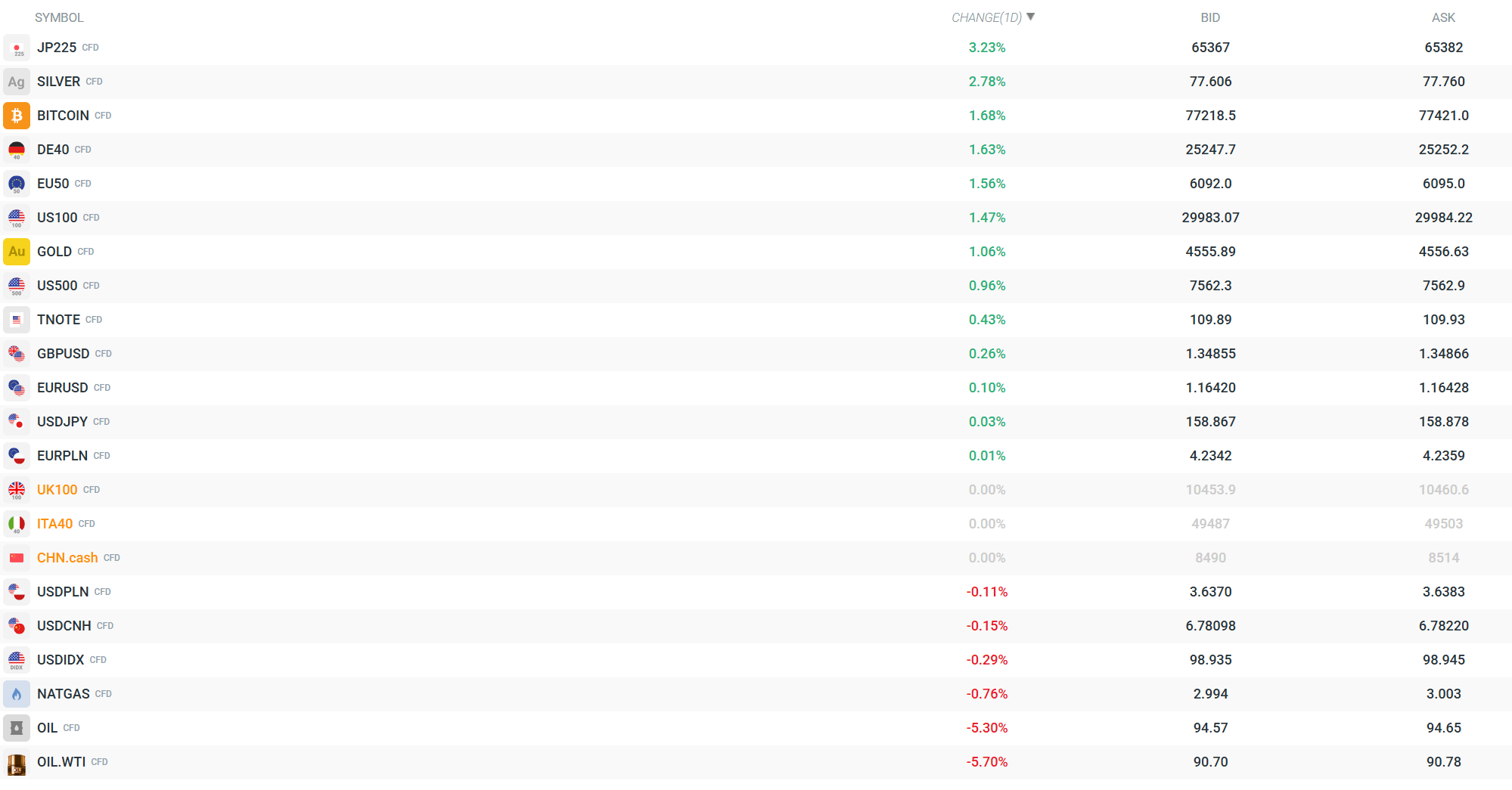

JP225 (CFD) is up 3.24% today at 65,372 – the biggest gain among the major indices. The DE40 is up 1.65% (25,252) and the EU50 is up 1.60% (6,094) – European futures are opening strongly in risk-on mode.

💱 CURRENCIES

-

The CHF is by far the strongest currency today (Currency Strength Meter), with the GBP and AUD in second and third place. At the other end of the scale, the JPY, USD and NZD are the weakest – a clear shift away from safe-haven currencies towards riskier currencies.

-

EUR/USD is up +0.11% to 1.1643, GBP/USD is up +0.26% to 1.3486. USD/JPY is virtually unchanged at 158.86. EUR/PLN is stable at 4.2343, whilst USD/PLN is down slightly (-0.12%) to 3.6367 – the zloty is gaining slightly on the back of a weaker dollar.

-

The NOK and CHF are strengthening significantly against other currencies, whilst the JPY and TRY are under pressure. The USDIDX (dollar index) is down 0.30% to 98.93.

🛢️ COMMODITIES

-

Oil is the biggest loser of the session: OIL (Brent CFD) is down 5.35% to $94.52/bbl, whilst OIL.WTI has fallen 5.75% to $90.65/bbl – the lowest levels in two weeks. The fall is a direct reaction to progress in US–Iran talks and signs that the Strait of Hormuz is being physically unblocked.

-

Gold (GOLD CFD) is up +1.21% to $4,562/oz – paradoxically, it is being supported by a weaker dollar rather than the usual safe-haven demand. Silver (SILVER CFD) is rising more sharply, up +2.91% to $77.70/oz. Natural gas (NATGAS) is down -0.86% to $2.99.

-

Oil prices remain above pre-war levels (up 30% since 28 February), and analysts warn that even after the Strait of Hormuz reopens, it will take months for the energy supply chain to return to normal – the inflationary pressure will not disappear quickly.

₿ CRYPTOCURRENCIES

-

Bitcoin (CFD) is up +1.68% to $77,215 – it is moving in line with the broader risk-on sentiment, benefiting from a weaker dollar and improved market sentiment. The movement is moderate compared to the performance of Asian equities.

🔑 WHAT TO WATCH OUT FOR TODAY

-

Every headline from the US–Iran talks is crucial – the market is teetering between euphoria and disappointment. With low liquidity (the US, UK and parts of Europe are closed), every tweet or post from Trump or Rubio could trigger sharp movements in oil, the dollar and index futures. A proper trading session with full liquidity will not return until Tuesday.

Volatility observed across major instruments. Source: xStation

Oil Prices Fall: Renewed Hopes for the Opening of the Strait of Hormuz

Economic Calendar: The US, the UK, and parts of Europe will be closed for trading 💡 (25.05.2026)

💯Daily Summary - Wall Street Close to Records Ahead of Long Weekend

🔴A New Era at the Fed: Kevin Warsh Takes the Helm. US30 above 50k

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.