UK bond yields continue to rise on Friday. The 10-year yield is now close to the 2007 peak, if we break above 5.2%, currently yields are 5.16%, that would be a significant milestone, and could drive 10-year yields to their highest level since the 90s. Back then the UK 10-year yield peaked around 6.5%, which was not a comfortable place for the country to be in.

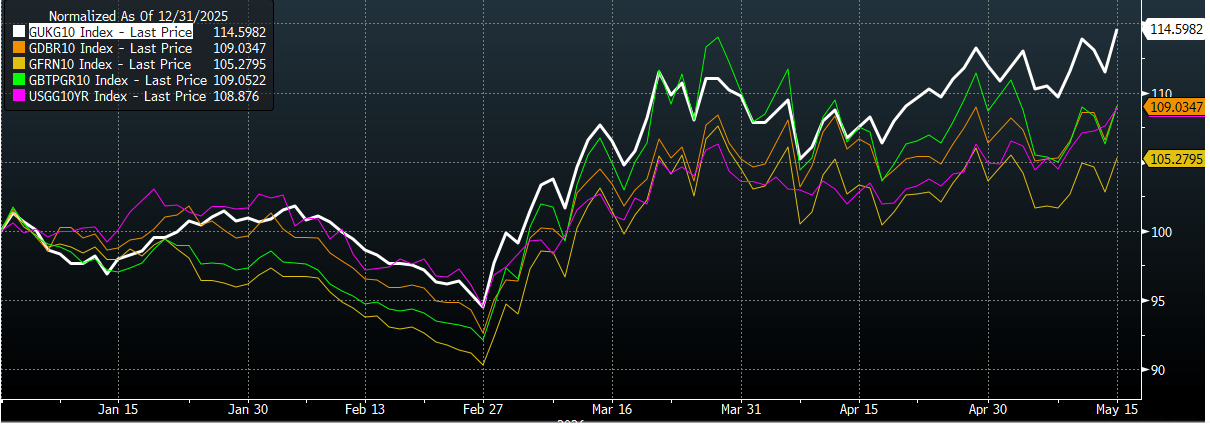

While global bond yields are rising on the back of inflation fears, there is a clear political risk premium in the UK market, and UK yields have broken away from the developed market pack, as you can see below. The 10-year yield is significantly higher in the UK compared to our peers. The market is facing more months of political chaos, this time under the Labour party. The risk is that a prolonged battle, one of the candidates is not even an MP yet, could lead to a race to the bottom, driven by the hard left of the Labour Party membership.

Are we going back to the 1970’S? Labour could be

The soft left is already in power in the UK, while Starmer promised a centrist economic and fiscal policy in his manifesto, his moves have been anything but, and bond yields have been rising throughout his tenure. The main risk for bond markets is that the current political turmoil leads to the UK having its most leftist Labour government since the 1970’s, even through we don’t know when a leadership contest will take place.

A weak pound erodes attractiveness of our debt

The bigger issue for the UK is that it is a big sovereign borrower and the pound is unstable. The reasons to hold UK debt are weak enough already without replacing the current PM with a politician who has said he would not be in ‘hock to the bond market’. While no one wants to say this out loud, any UK government absolutely needs to be in hock to the bond market. The tax burden is at a record high and is growing at the fastest rate in the OECD, so if Rayner and Burnham etc. want to double down on left-wing policies like bosting public sector wages and paying out ever more in benefits, then they will need access to sovereign debt markets to do this.

GBP/USD is lower by nearly 7% in the last 10 years, as political ructions including Brexit, Covid and then a succession of prime Ministers, Starmer is the 5th in 6 years, have weighed on the currency. This is a big deal. As UK pension funds have moved away from defined benefit plans to defined contribution plans, at least for the private sector, then domestic buyers of bonds have dwindled, as defined contribution pension plans typically invest in equities. This leaves the government looking to foreign buyers to purchase our debt. This is less attractive if the currency is weak. The pound is eking out a small gain so far this year vs. the USD, but it has deteriorated dramatically in the past 2 weeks and is the weakest of the major currencies over the past month.

What can calm the Gilt market?

For the pound to recover, we need to see UK gilts also stage a recovery. So, what could calm the bond market? Andy Burnham has been silent since announcing his plans to stand in the Makerfield by-election. He needs to address the bond market’s concerns, firstly by saying that he will watch the bond market, and secondly that he will tackle the UK’s welfare bill. This may not be popular with Labour backbenchers, but it is popular with voters, including a decent number of Labour voters. Burnham and the other candidates also need to confirm that they will adhere to the UK’s fiscal rules and commit to keeping Rachel Reeves in place.

Political risk premium now permanently attached to UK debt

There is a good chance that this will not happen, and Burnham and co. will not address the UK’s soaring bond yields. For now, the country, the voters, the politicians and the owners of UK debt need to face the fact that a political risk premium could be permanently attached to UK Gilts. The Labour party promised stability and ‘securenomics’, it has delivered neither.

Looking elsewhere, risk is selling off across global equity markets today, and US futures point to large losses of more than 1% for the S&P 500 and the Nasdaq, as tech stocks sell off. European indices are tumbling, the FTSE 100 is down nearly 2% and the Dax is also down more than 2%.

FTSE 100 also hit by political turmoil

In the UK, the FTSE 100 is weighed down by miners, banks and defense names. UK banks are down sharply as they find themselves in the political crosshairs. Burnham and co. have threatened to tax UK banks if they get into power. Also, a prolonged leadership battle means that long-awaited legislation, such as the financial services bill, could be delayed, which may impact the City. Barclays, whose CEO was a big fan of Reeves, has seen its share price slide nearly 4% today. Rolls Royce is also down 3.7% and more than 7% for the week, as rising borrowing costs makes it harder to fathom how the UK government will fund defense spending going forward.

While the left wing of the Labour party might argue that bond yields are rising everywhere on Friday, there is undoubtedly more upside pressure on UK Gilt yields and more downside pressure on the pound. The Labour rebels could not have chosen a worse time to try to unseat the Prime Minister.

Chart 1: UK 10-year Gilt yields, vs Germany, France, Italy and the US

Source: XTB

Daily summary: A week closed with declines – is the market starting to fear inflation?

Three markets to watch next week: US100, GBPUSD, GOLD (15.05.2026)

US OPEN: Wall Street Bleeds After Trump's Beijing Visit

Bond Markets Sell Off❗️TNOTE Dips Below 1-Year Low 📉

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.