- The Trump-Xi meeting has yielded no major revelations.

- Issues surrounding rare earth metals and the war in Iran remain unresolved.

- The headlines are not particularly favourable for the semiconductor sector.

- US bond yields continue to rise – 10-year yields are at their highest level in a year.

- The Trump-Xi meeting has yielded no major revelations.

- Issues surrounding rare earth metals and the war in Iran remain unresolved.

- The headlines are not particularly favourable for the semiconductor sector.

- US bond yields continue to rise – 10-year yields are at their highest level in a year.

All major US stock indices are reporting losses today. The Russell 2000 (-2.4%) is leading the decline, with NASDAQ Composite (-1.4%) and S&P 500 (-1.1%) also down by more than a percentage point.

Why are we seeing a sell-off?

1. Not a very impressive list of deals announced by President Trump during his recently concluded visit to Beijing.

The lack of an agreement regarding the sale of NVIDIA chips is particularly pessimistic. Trump said that the Chinese side has decided against purchasing American technology, instead planning to improve its own solutions.

- NVIDIA's share price opened down 3.6%, the biggest drop since April 30 (currently down 4.4%).

- Other companies producing microprocessors are also seeing declines – Intel (-7,4%), Micron (-6,8%), AMD (-5%) and ARM Holdings (-7,8%).

Key issues for the AI sector remain unresolved, including rare earths trade. There has also been no news regarding joint efforts to open the Strait of Hormuz.

2. Growing concerns about the inflation situation following the publication of higher-than-expected inflation readings in recent days.

- Consumer inflation highest since May 2023 (3.8%). The rise in the core measure for the services sector (3.4%) is particularly concerning.

- Producer inflation highest since December 2022 (6%). Above expectations on all measures, including core (5.2%) and super-core (4.4%)

- Import prices (4.2%) and export prices (8.8%) also increased.

This led to:

- A significant increase in US bond yields. The 10-year yield rose 18 basis points on a weekly basis. 4.57% is the highest level in a year.

- An upward repricing in FOMC interest rate expectations. A hike before the end of the year is currently the market's baseline scenario (60% implied probability).

- The dollar strengthened. The US currency appreciated by nearly 1.5% against the euro.

None of the above factors could be considered favorable for the US stock market.

3. The exposure of indices to declines due to profit-taking after the very impressive gains recorded in recent weeks.

- The NASDAQ 100 has increased by nearly 30% since the late March-low.

- The P/E ratio for the NASDAQ 100 recently exceeded 38, significantly above the historical median (around 25).

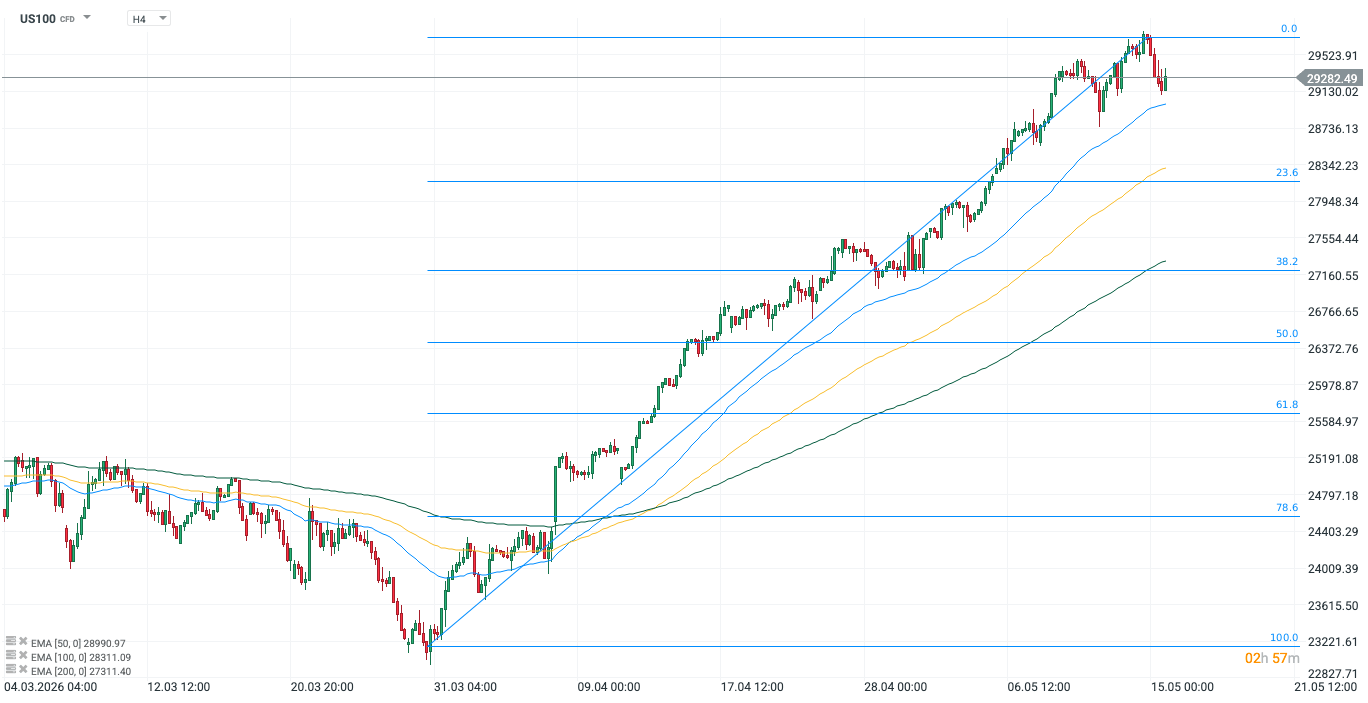

Technical analysis

US100 (H4)

Source: xStation, 15/05/2026

Source: xStation, 15/05/2026

The upward wave slowed down its momentum around 29,700 points, encountering a strong supply barrier in the area of historical highs. Although the system of exponential averages (EMA 50, 100, 200) maintains a strongly upward geometry, the price is starting to get dangerously close to a test of the EMA 50 (currently around 29,000 points). The scale and steepness of the current impulse itself suggests the need for a technical cooling of sentiment before a possible attack on the round, psychological level of 30,000 points. The closest significant static support remains FIBO 23.6%, which coincides with previous price extremes and may be the first stop of a possible correction.

Company news

- NVIDIA (NVDA.US): The company's shares are suffering from a clear divergence between the initial declarations and the final results of President Trump's diplomatic trip to Beijing. The Trump-Xi summit initially brought optimistic headlines about the opening of the Chinese market to H200 chips, but today's reports of a lack of formal approvals from Beijing and the reluctance of Chinese giants to finalize purchases have triggered a wave of disappointment. This has prompted investors to take profits and close positions just before the key financial report scheduled for May 20.

- Intel Corp. (INTC.US): Intel's stock price plummeted more than 6% today (to around $109), continuing a trend that began earlier this week. Since the beginning of the year, the company's shares have tripled in value, fueled by a groundbreaking contract with Apple for the production of M-series processors at the Intel Foundry, among others. This created significant room for profit-taking in the face of even a slight shift in market sentiment. The company's fundamentals appear to be the strongest in years, but some investors fear that the current valuation is overly optimistic ahead of the actual rate of margin growth.

- Figma (FIG.US): The digital product design and prototyping platform, which debuted on the NYSE in July 2025, has released its Q1 2026 results. Revenue increased 46% y/y to $333.4 million, driven by the growing monetization of AI products. Shares are up over 13%, but the company is still down over 70% y/y.

- Klarna (KLAR.US): The Swedish deferred payments and digital banking giant released its Q1 2026 results, surprising the market with the scale of its profitability improvement. EPS was -$0.01, compared to the expected -$0.20, and revenue exceeded $1 billion (consensus below $945 million). Adjusted operating profit jumped to $68 million from just $3 million a year earlier, and net profit finally turned positive – $1 million, compared to a loss of $99 million in Q1 2025. The number of active users increased by 21% y/y to 119 million. Sentiment is clouded by a weaker-than-expected forecast for Q2, although management maintained its full-year guidance. After initial gains, shares fell to $15, representing a level more than 65% lower than a year ago.

---

Michał Jóźwiak, Financial Markets Analyst at XTB

Daily summary: A week closed with declines – is the market starting to fear inflation?

Market Wrap: Stocks and metals dip as Trump-Xi summit fails to break Iran deadlock 📉 (15.05.2026)

Market Wrap: What does Trump's Beijing visit mean for the markets?

Economic Calendar: All eyes on US consumer 🇺🇸 (14.05.2026)

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.