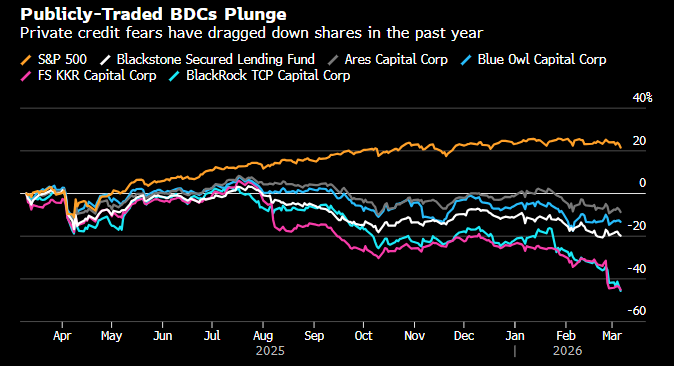

The private credit market is off to a weak start to the year. After Blue Owl restricted withdrawals from one of its private credit funds a few weeks ago, the market began openly questioning the solvency and valuations of many funds.

This weekend, BlackRock joins the list of firms fueling investors’ concerns.

Source: Bloomberg Finance LP

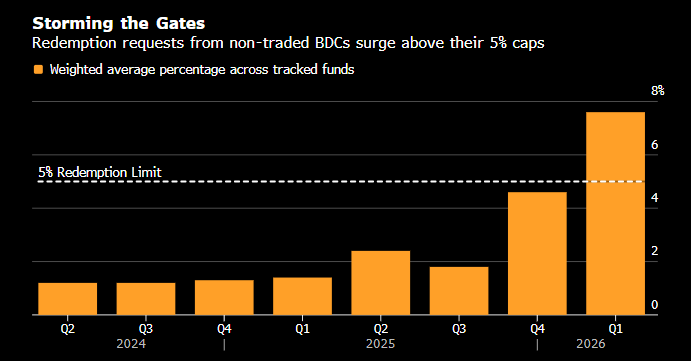

Capital outflows from the private credit market are reaching unprecedented levels. Given the nature of this market and its lack of liquidity, this puts funds in a difficult position.

Source: Bloomberg Finance LP

This difficult situation is also clearly reflected in valuations.

Companies such as BlackRock and Blue Owl are now paying the price for flaws in their own strategy. The idea behind the growth of private credit was to expand the offering to retail investors, but they have a very different risk profile and a much lower tolerance for having their capital locked up for the long term. Investors’ concerns are not unfounded either: the private credit market plays a fundamental role in financing the build-out of AI infrastructure, an area whose promised returns are increasingly being called into question.

What are funds hiding?

The lack of liquidity in the private credit market is not, in itself, a reason to panic. Illiquidity is a fundamental feature of this market, not something extraordinary. What could be a major problem, evoking memories of 2007, is that, according to a Bloomberg investigation, many funds and positions in the private credit market have greater exposure to the software sector than they report.

In practice, this means that many funds may be masking their full exposure to software in order to obtain financing without paying the appropriate risk premium. The very existence of such a premium—and evidence of attempts to conceal exposure to avoid it, suggests that the situation of tech companies and the private credit market may be worse than the financial metrics of many of these firms would imply.

BLK.US (D1)

Source: xStation5

While the problems in the private credit market will not disappear overnight, and may, over time, prove worse than expected, this does not change the fact that, as of today, the chart action looks more like an emotionally driven, temporary correction. An RSI around ~25 signaled a “bottom” in previous sell-off episodes.

Daily Summary: Middle East Sparks Oil Market

Live Nation climbs on antitrust deal

Is the FDA sabotaging medical companies? UniQure’s valuation rollercoaster

Oil Under Pressure as G7 Decision Remains Pending

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.