The main factor influencing volatility

The dominant topic of the day was a report in *The New York Times* about a possible delay of OpenAI’s IPO until 2027, due in part to SpaceX’s poor performance following its IPO and the overall volatility of AI-related stocks. JPMorgan explicitly warned that such a scenario “could slow the pace of spending on AI infrastructure,” and analysts at Vital Knowledge confirmed that the market is reacting primarily to the risk of a slowdown in infrastructure spending. Paradoxically, however, postponing the IPO date may actually sustain the narrative of expectations surrounding AI, which could benefit valuations in the long run.

Geopolitics

Trump reported on Truth Social that Iran had launched at least four kamikaze drones at ships in the Strait of Hormuz, calling it a “stupid violation of the ceasefire agreement.” One of the drones struck the deck of a large container ship, while the other three were shot down. The Strait of Hormuz is a route for approximately 20% of global oil supplies, but the oil market reacted with limited price volatility, with oil prices trending downward. Toward the end of the day, however, significant signs of de-escalation emerged: the U.S., Israel, and Lebanon signed a trilateral framework agreement, which, according to Israel’s ambassador to the U.S., is results-based and will be reviewed in stages. At the same time, U.S. Secretary of Commerce Howard Lutnick announced that Europe had passed historic legislation regarding the U.S.-EU trade agreement, reducing its tariffs to zero for the first time in history—a move Lutnick described as a breakthrough for American manufacturers, farmers, and fishermen.

Macro data

Data from the U.S. turned out to be mixed. The University of Michigan Consumer Sentiment Index came in at 49.5 points, compared to a forecast of 50.0 points, although consumer expectations surprised on the upside at 50.7 points. The U.S. goods trade balance came in well below expectations, reaching a deficit of $105.8 billion versus a forecast of a $85.0 billion deficit, signaling ongoing tensions in foreign trade. Minneapolis Fed President Neel Kashkari revised his March scenario from one rate cut to one rate hike this year, citing supply-side inflation, including the expansion of AI infrastructure.

Indices

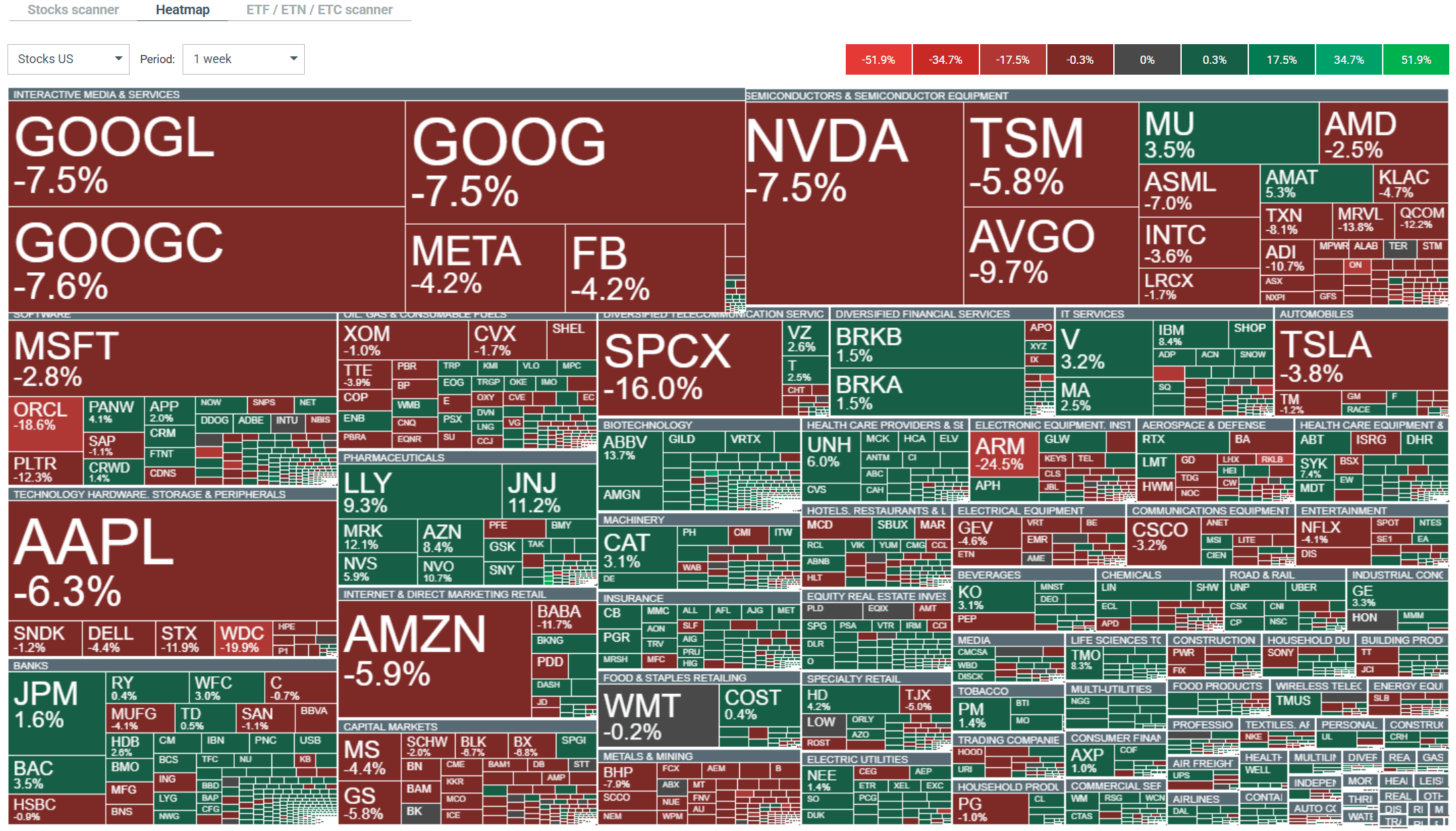

The U.S. trading session is drawing to a close amid mixed sentiment. The S&P 500 rose 0.3% on the day but is down more than 1% for the week; the Nasdaq is heading for a weekly loss of about 4%; and the Dow Jones posted a weekly gain of 0.6%. In Europe, all major indices closed in the red. The DAX fell 1.22%, the Italian ITA40 dropped 0.83%, and the British UK100 lost 0.17%. Losses were particularly severe in Asia, where Japan’s JP225 lost 1.86% according to the ticker, the Nikkei 225 ended the day down more than 4%, and South Korea’s Kospi plummeted 5.81%.

Stocks

On the Nasdaq 100, the top performers were AppLovin (up 7.43%), Workday (up 7.25%), and Axon Enterprise (up 6.90%), while on the other end of the spectrum, the biggest losers were Western Digital (down 10.22%), Seagate Technology (down 8.65%), and Analog Devices (down 7.40%). On the Dow Jones, the top gainers were IBM (up 4.82%), Microsoft (up 4.80%), and Salesforce (up 4.62%), while the biggest losers were Caterpillar (down 3.95%), Goldman Sachs (down 3.42%), and Cisco (down 3.08%). It is worth noting that Michael Burry partially closed his short position in Palantir and opened long-term LEAPS options on Microsoft expiring in December 2028. The healthcare sector was on track for its best week since 2022, with the entire sector rising by over 7%, led by Bio-Techne and Incyte.

Weekly capital turnover on the U.S. stock market. Source: xStation

Currencies

The EURUSD pair gave back some of its morning gains, trading around 1.13896, and during the day, momentum clearly shifted to the sellers. The dollar remained under moderate pressure, with the USDIDX index at 101.091 and a daily change of -0.15%. GBP/USD gained a symbolic 0.09% and was trading around 1.32037, while the USD/JPY pair hovered around 161.734.

Commodities

Gold continued to recover its losses, gaining 1.41% to trade above $4,082 per ounce, while silver rose 2.44% to nearly $59.20. Crude oil was under significant pressure despite the geopolitical escalation in the Strait of Hormuz. WTI lost 3.14% to around $69.21, and Brent fell 3.24% to $72.55, suggesting that the market is pricing in lasting stability in the region after all. Natural gas rose 2.14% to $3.339 and broke above the 200-day EMA.

Three Markets to Watch Next Week: EURUSD, Gold, S&P 500 (26.06.2026)

Fed's Kashkari says AI will force a rate hike; EURUSD and USD reverse early moves ❗

University of Michigan sentiments lower than expected

Andy Burnham and financial markets, the initial impact

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.