AeroVironment shares (AVAV.US) are gaining around 15% after the company announced a $500 million contract with the U.S. Army to supply counter-drone systems. The deal further strengthens positive sentiment following record fiscal fourth-quarter 2026 results released just a few days earlier. The company is currently growing not only through unmanned systems, but also through the rapidly expanding counter-drone defense segment. Management believes this area could become one of AeroVironment’s key growth drivers over the next several years.

Pentagon focuses on drone defense

The contract was awarded by the U.S. Army Contracting Command at Detroit Arsenal and is structured as a firm-fixed-price framework agreement. AeroVironment will provide commercial Counter-UAS systems and solutions designed to detect and neutralize small drones used on the modern battlefield.

Work will be carried out through June 2029, with funding allocated as subsequent orders are placed by the U.S. Army.

The contract announcement came just days after AeroVironment reported very strong financial results. In the fiscal fourth quarter of 2026, AeroVironment delivered:

- revenue of $641.6 million, up 133% year-over-year,

- adjusted EBITDA of $140.1 million,

- adjusted EBITDA margin of 22%,

- adjusted earnings per share of $1.84 versus $1.61 a year earlier.

The sharp revenue increase was partly driven by the acquisitions of BlueHalo and Empirical Systems Aerospace, although organic growth still reached around 31%.

Backlog continues to grow

At the end of the fiscal year, funded backlog increased to $1.2 billion from $726.6 million a year earlier.

Total bookings reached $2.7 billion, compared with roughly $2 billion in revenue, resulting in a book-to-bill ratio of 1.4.

This means the company is winning new contracts faster than it is converting them into revenue, improving visibility for future sales.

Counter-UAS could become the next growth pillar

Although AeroVironment is best known for its Switchblade loitering munitions, management is increasingly focused on the counter-drone systems segment.

In fiscal 2026, the Counter-UAS business generated approximately $200 million in revenue.

The company is currently developing three main solutions:

- Titan radio-frequency jamming systems,

- LOCUST directed-energy weapons,

- Freedom Eagle-1 kinetic interceptors designed to destroy incoming drones.

CEO Wahid Nawabi believes that within the next 3–5 years, the Counter-UAS segment could match the scale of the company’s current business or even become two to three times larger.

Guidance remains strong

Management expects fiscal 2027 revenue of $2.1 billion to $2.2 billion, implying roughly 10% growth year-over-year.

The company also highlights very strong demand for its military solutions, especially in unmanned systems and counter-drone technologies.

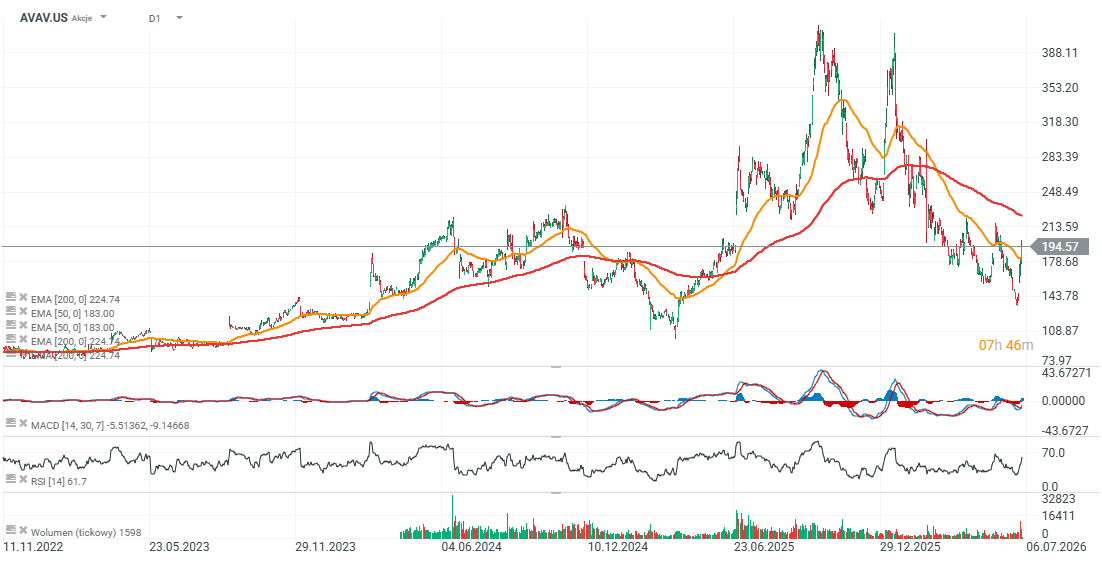

Market still sees risks as shares remain 50% below their highs

Despite the latest rally, AeroVironment remains one of the more expensive defense stocks. Shares trade at roughly 54 times the midpoint of management’s fiscal 2027 adjusted earnings guidance.

Some investors remain concerned about the high price paid for the BlueHalo acquisition, while elevated short interest may keep the stock vulnerable to higher volatility. At the same time, the record backlog, strong Counter-UAS growth, and additional contracts with the U.S. Department of Defense continue to support the company’s long-term outlook.

AeroVironment shares are still trading roughly 50% below their record highs, which took the stock close to $400 per share in 2025. From current levels, the stock remains around 10% below a key resistance area marked by the 200-day Exponential Moving Average (EMA200), shown by the red line. Key support is located around $140–150 per share, based on previous price reactions.

Source: xStation 5

US100 falls almost 2% 🚩 Semiconductor stocks plunge as SanDisk tumbles 13%

Stock of the Week: Adobe: is AI taking its future away?

US Open: Nasdaq surges amid semiconductor rebound 🔼 Tesla shares down despite strong deliveries report

AMS OSRAM: Is it the next Micron?

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.