Gold is down nearly 0.7% today, trading below $4,100 per ounce, as Deutsche Bank significantly revised its outlook for the precious metal market. The bank lowered its average gold price forecast for Q3 2026 to $4,300 per ounce and for Q4 2026 to $4,800 per ounce, representing cuts of more than 22% and 17%, respectively. As recently as April, Deutsche Bank had projected gold could rise toward $6,000 per ounce, citing fiscal deficits, de-dollarization trends, and reduced exposure to U.S. Treasuries by emerging-market central banks.

The shift in outlook is largely driven by a more hawkish repricing of Federal Reserve policy expectations and continued strength in U.S. economic data. Deutsche Bank argues that Fed repricing and the resilience of the U.S. economy have become the primary headwinds for gold. Its base-case scenario assumes the Fed keeps rates unchanged through the end of 2026, but the bank warns that three to four additional rate hikes could push gold as low as $3,800 per ounce.

Why Are Gold and Silver Falling?

- Goldman Sachs also lowered its year-end gold forecast by $500 to $4,900 per ounce and no longer expects Fed rate cuts in 2026.

- Bank of America has stepped back from its previous $6,000 target, arguing that persistent inflation may require tighter monetary policy.

- Outflows from gold-backed ETFs suggest investor demand is significantly weaker than during previous bull markets.

- Discounts in Chinese gold prices relative to Comex indicate that Chinese imports are unlikely to provide meaningful support for the market.

- Central banks remain the strongest pillar of demand and are expected to continue supporting the market over the longer term.

- Gold has fallen more than 22% since the outbreak of the U.S.-Iran conflict at the end of February, despite traditionally benefiting from heightened geopolitical risk.

- Silver has performed even worse, losing roughly one-third of its value since late February and dropping more than 5% during the latest session.

- Gold futures ended Tuesday down approximately 1.3% near $4,149 per ounce, while spot prices briefly approached $4,090.

- The stronger U.S. dollar continues to weigh on precious metals, with the Dollar Index rising roughly 0.8% since the last Fed meeting.

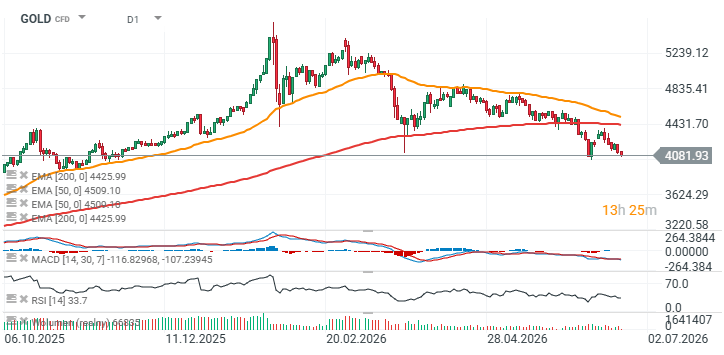

Markets Await the PCE Inflation Report – GOLD Chart (D1)

The next major test for gold will be the upcoming U.S. PCE inflation report. A stronger-than-expected reading could reinforce the hawkish Fed narrative and provide further support for both the dollar and Treasury yields. For gold, this would represent a more challenging environment, as the metal does not generate income and competes directly with increasingly attractive yield-bearing assets.

The current macro backdrop suggests that geopolitics alone is no longer sufficient to drive precious metals higher. As long as the U.S. economy remains resilient, the dollar stays strong, and the Federal Reserve maintains a restrictive stance, gold and silver may struggle to regain their previous upward momentum.

Looking at the chart, gold is currently testing local lows in the $4,000–4,100 per ounce range, while the daily RSI has fallen to just under 34, approaching oversold territory. Recent sessions have also been characterized by predominantly selling volume.

Source: xStation5

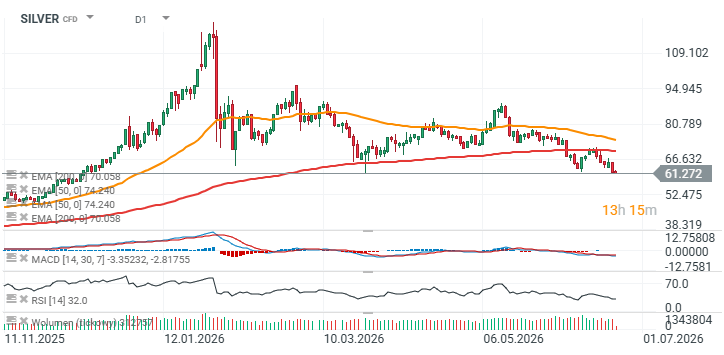

Silver has already broken below its local March 23 low and briefly fell to its weakest level since mid-December 2025.

Source: xStation5

Market Wrap: Defense stocks in panic🚨Rheinmetall tumbles 13%

Chart of the day: EURUSD deepens decline 🚩 What's next for the pair? (24.06.2026)

Economic calendar: German Ifo data and Micron earnings in focus (24.06.2026)

Morning wrap: Indices stabilize after the sell-off 🔼 Markets await Micron earnings (24.06.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.