-

Intervention at 160: Breaking the psychological USDJPY barrier forced Tokyo to act, pushing the rate down to 155 amid low liquidity during Golden Week.

-

Buying Time: Market interventions provide only temporary relief; a long-term trend reversal requires BoJ rate hikes and a shift in U.S. dollar strength.

-

Path to 1.0%: Despite the slow pace, high inflation and a weak yen are fueling a hawkish shift within the BoJ, with eyes on a 1.0% rate later in 2026.

-

Intervention at 160: Breaking the psychological USDJPY barrier forced Tokyo to act, pushing the rate down to 155 amid low liquidity during Golden Week.

-

Buying Time: Market interventions provide only temporary relief; a long-term trend reversal requires BoJ rate hikes and a shift in U.S. dollar strength.

-

Path to 1.0%: Despite the slow pace, high inflation and a weak yen are fueling a hawkish shift within the BoJ, with eyes on a 1.0% rate later in 2026.

Japan has once again found itself at the center of attention in global financial markets. Massive problems related to the energy crisis, high bond yields, prospects of resurgent inflation, and economic slowdown have led to another wave of yen sell-offs. Ultimately, when USDJPY once again broke through the 160 level, a currency intervention most likely took place. Although there has been no direct confirmation yet and we must wait for official, significantly delayed data from the Ministry of Finance, officials are confirming the situation between the lines and announcing a possible further fight against speculators.

A Repeat of the Past: What Happened on April 30th?

The final session of April brought dramatic scenarios. The USDJPY pair once again breached the psychological 160 barrier, triggering an avalanche of orders and forcing Tokyo to act. We quickly observed a strengthening of the yen, and the USDJPY pair dropped to the 155 level. Such a sharp move occurred during a period of low liquidity—the Golden Week in Japan. It is also worth noting that this move coincided with record highs on the June Brent crude oil contract, which also dropped significantly at the moment of the Japanese intervention.

Golden Week is a 7-day period at the turn of April and May, featuring four national holidays. Authorities in Tokyo, led by Atsushi Mimura, sent a clear signal: "Golden Week" will not be a safe haven for speculation.

History of Interventions: Is This a Good Time for the Yen? (2022–2024)

Japan has a rich, albeit bittersweet history of fighting market trends. Recent history shows that interventions are an effective "emergency brake," but they rarely change the direction of travel in the long term. It is also worth remembering that there were years when the Ministry of Finance sold the yen due to excessive strength to boost export power.

History of recent interventions:

-

September/October 2022: The first large-scale market operations in decades conducted at a record-weak yen. The result was approximately a 15% strengthening of the yen against the dollar, a move that lasted about 3 months. USDJPY returned to the October 2022 peaks after about 10 months.

-

April/May 2024: Action aimed at defending the previous 2022 peaks and the approach to the psychological level of 160 USDJPY. It brought immediate success, and the situation on the currency pair only stabilized longer-term following dovish signals from the U.S. Federal Reserve (Fed).

-

July 2024: Another strike against speculators, this time supported by hawkish rhetoric from the Bank of Japan. The effect was much more lasting than in previous cases because the intervention was accompanied by an actual interest rate hike by the BoJ. On the other hand, the downward move lasted 2 months and amounted to approximately 13.5% on the USDJPY pair.

What is the conclusion? Intervention alone is only "buying time." Real change depends on the divergence (or lack thereof) between the policies of the Bank of Japan and the U.S. Federal Reserve.

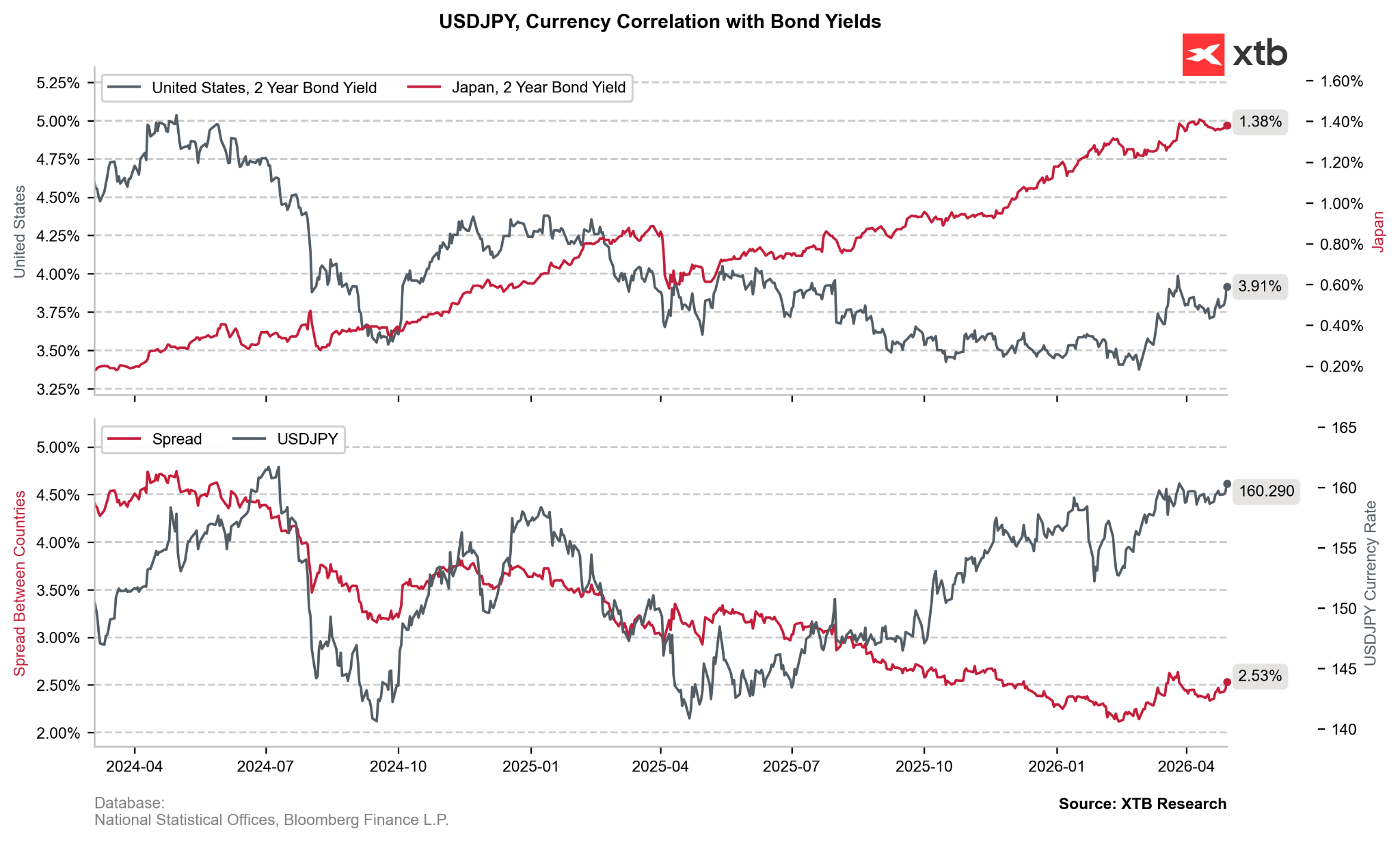

It is worth noting that the spread should have clearly favored the yen for nearly a year now, but the rise in yields in Japan is a result not only of higher interest rates but primarily concerns regarding the massive debt situation and further fiscal expansion plans. Source: Bloomberg Finance LP, XTB

It is worth noting that the spread should have clearly favored the yen for nearly a year now, but the rise in yields in Japan is a result not only of higher interest rates but primarily concerns regarding the massive debt situation and further fiscal expansion plans. Source: Bloomberg Finance LP, XTB

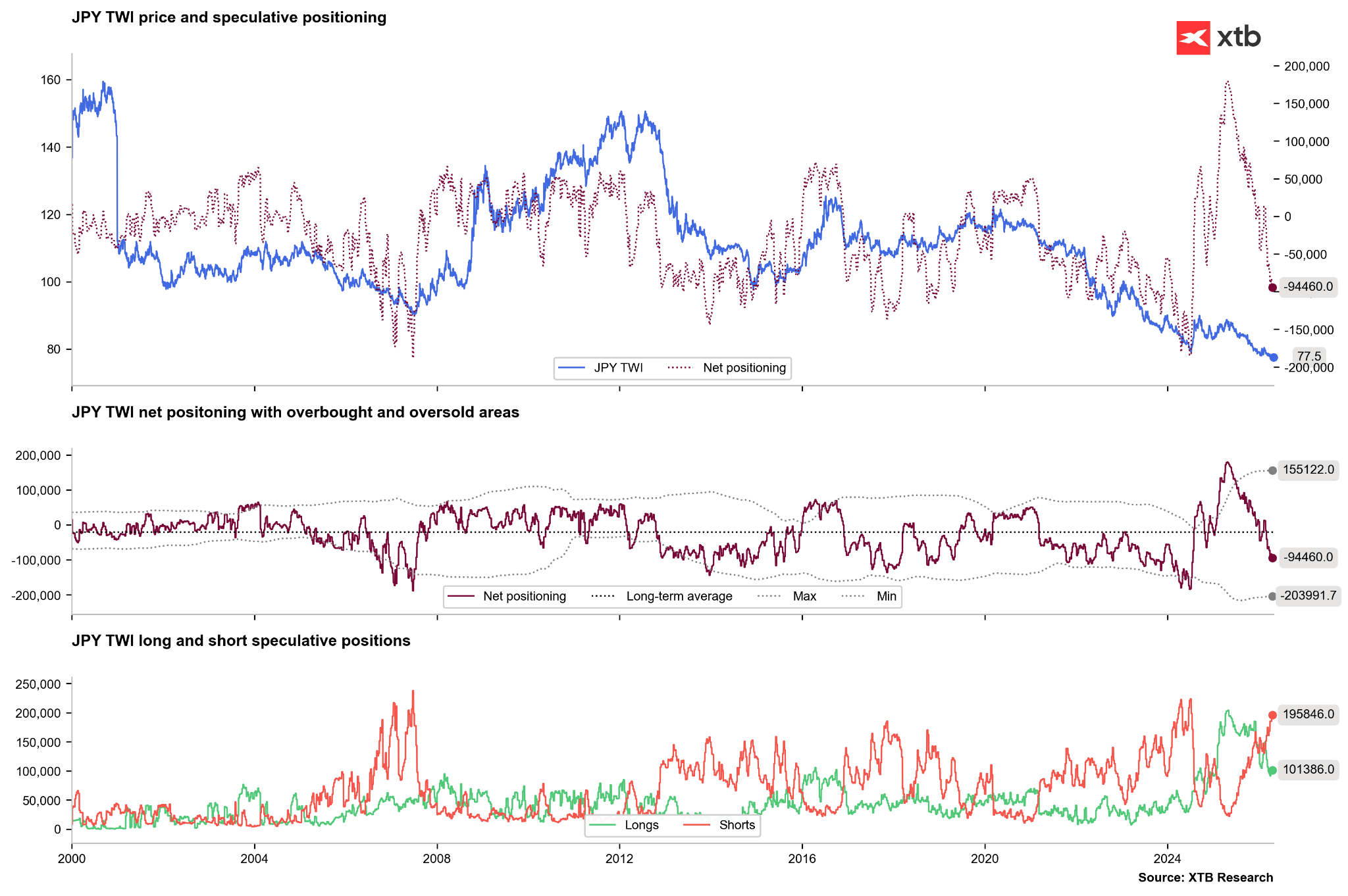

Furthermore, after the previous intervention in 2024, speculators changed their stance and a sharp short-squeeze on the yen began, with the market shifting from a net negative to a positive positioning for the first time since 2016. Currently, however, we are seeing an increase in short positions to almost the extreme high levels of 2024 or 2007. Source: xStation5

Furthermore, after the previous intervention in 2024, speculators changed their stance and a sharp short-squeeze on the yen began, with the market shifting from a net negative to a positive positioning for the first time since 2016. Currently, however, we are seeing an increase in short positions to almost the extreme high levels of 2024 or 2007. Source: xStation5

Bank of Japan Strategy: An Extremely Slow March Toward Normalization

While the Ministry of Finance fights on the front line with billions of dollars from reserves, the Bank of Japan (BoJ) is conducting an operation to normalize monetary policy after decades of maintaining extremely low interest rates. Nevertheless, due to the state of the Japanese economy, this process is very slow.

-

Where are we? After the December hike in 2025, the main interest rate in Japan stands at 0.75%—its highest level in three decades, yet still one of the lowest in the world. Japan is still being used for carry trade transactions.

-

Divisions in the board: Recent meetings have shown a growing hawkish camp. As many as three out of nine board members favor an immediate move to the 1.0% level. This means that the probability of a hike this year is high.

-

Inflationary pressure: The BoJ forecasts core inflation (core CPI) for 2026 at 2.8%, which, with current rates, means that real interest rates remain deeply negative.

What’s Next for Rates?

The base scenario assumes that the BoJ will raise rates to 1.0% still in 2026. The weak yen is a key catalyst here: expensive energy and food imports are draining the wallets of the Japanese people, becoming a political issue that the central bank cannot ignore.

Does the Yen Have a Chance for a Permanent Recovery?

The intervention at the end of April is a clear sign that Tokyo's threshold of patience lies around the 160 level. However, the fundamentals remain relentless. For the yen to gain value permanently, the market must believe in two factors: a change in BoJ communication to a more hawkish tone, which must be handled cautiously to avoid a crisis in yields; and a change in sentiment regarding the dollar. If the crisis in the Strait of Hormuz ends, the dollar will no longer be as necessary as a safe haven. On the other hand, if the Fed begins to communicate possible hikes, USDJPY could permanently find itself above 160.

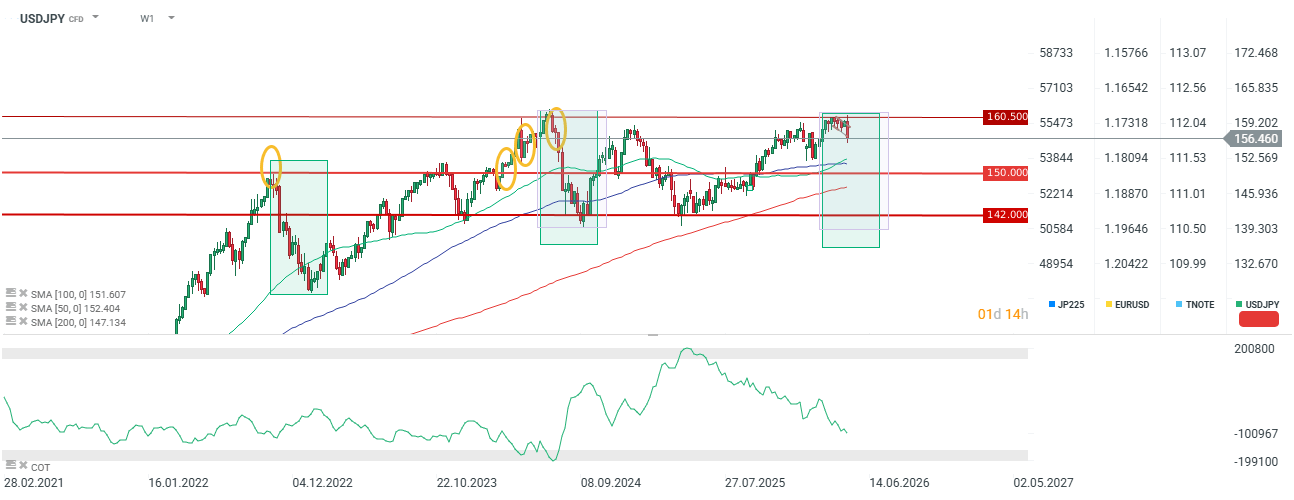

The pair is currently in an important area of potential extreme overbought conditions. Interventions would need to be carried out regularly, and additionally, we would need to see a fundamental shift on both the Japanese and global sides. Source: xStation5

The pair is currently in an important area of potential extreme overbought conditions. Interventions would need to be carried out regularly, and additionally, we would need to see a fundamental shift on both the Japanese and global sides. Source: xStation5

⏰US500 nears record highs ahead of Fed

Daily summary: Uncertainty grips the market amid earnings season

Costly war and lucrative contracts: Rebuilding ammo stocks after the Iran War

US OPEN: Concerns about OpenAI’s drag the whole market lower

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.