Nike’s (NKE.US) fiscal Q3 2026 results came in better than market expectations, which investors initially interpreted as a sign that the company is beginning to stabilize the business more effectively despite cost pressure and a more challenging operating environment. After the results were released, the stock rose 3% in after-hours trading, but ultimately the shares lost nearly 10%, falling to $47. The key positives were an upside surprise in earnings per share, revenue slightly ahead of forecasts, and improvement in inventories, which had been one of the market’s main areas of focus in recent quarters. However, the report was not without weaker elements, particularly pressure on gross margins related to tariffs in North America and higher operating costs. Likewise, the analyst call pointed to at least several negative signals for the company’s business. Management sounded as though the recovery has not yet begun in earnest and may only arrive in a few more quarters.

Nike results

-

Earnings per share (EPS) came in at $0.35 versus expectations of $0.30, representing a positive surprise of 16.7%.

- Revenue reached $11.3 billion, slightly above the consensus estimate of $11.23 billion.

- Currency-neutral sales fell 3%, although reported revenue remained flat year over year.

- North America showed relative resilience, posting 3% revenue growth, while the other regions performed more weakly.

- Gross margin came in at 40.2%, down 130 basis points, mainly due to higher tariffs in North America.

- Inventories declined 1% year over year, which can be seen as a moderately positive signal after earlier problems with excess stock.

- SG&A costs rose 2%, with results burdened by approximately $230 million in severance costs.

- The effective tax rate was 20%.

- For fiscal Q4 2026, Nike is forecasting EPS of $0.19.

- The company is also assuming a gradual improvement in revenue in fiscal 2026 and 2027, suggesting that management expects a more stable recovery after a more difficult period.

- Management emphasized the effectiveness of its “win now” actions in North America, while also indicating that tariff pressure and inventory control will remain key management priorities.

- Among the company’s main risks are the impact of tariffs on profitability, the risk of inventories rising again, currency fluctuations, and uncertainty in global consumer demand.

- Nike has maintained its dividend for 43 years, and the current dividend yield stands at 3.1%.

What did Wall Street dislike?

First and foremost, the recovery is taking longer than investors had expected. This was probably the most important negative signal from the entire call. Management explicitly admitted several times that the “comeback is taking longer than we would like” and that some actions are taking more time than expected. This extends the period of pressure on results, increases execution risk, and reduces confidence in the pace of improvement that the market typically likes to price in early.

- Revenue remains under pressure, and expectations are still cautious. Nike said that in Q3 revenue was flat on a reported basis and down 3% on a currency-neutral basis. In the next quarter, fiscal Q4, it expects revenue to decline by 2% to 4%. In the following months through the end of the calendar year, revenue growth is expected to remain in the low single digits. In other words, the company has still not returned to real growth, and the improvement is expected to be very uneven across geographies and segments.

- Sales in Greater China are falling and will continue to weigh on the company. Revenue in the quarter declined 10% year over year, wholesale revenue fell 13%, and Nike Digital sales dropped as much as 21%. What is more, the company expects revenue in the region to decline by 20%. Management is not hiding the fact that any recovery in China may not happen quickly, which is concerning because China has historically been one of Nike’s key growth engines.

- Sales of sports footwear, apparel, and equipment declined, and although this category still looks relatively solid compared with the rest of Nike’s segments, it accounts for less than half of the company’s revenue. Wall Street may worry that Nike is showing isolated successes in running or football, but that its core lifestyle and sportswear business has still not been fixed.

Finally, in the last quarter gross margin fell 130 basis points to 40.2%, with one of the main reasons being higher tariffs in North America, which alone reduced margin by 300 basis points. In Q4, margin is expected to remain under pressure, with the company guiding to a decline of 25 to 75 basis points despite sequential improvement. Sales in Nike Direct fell 7%, and Nike Digital sales fell 9%. In Europe, the Middle East, and Africa (EMEA), digital sales declined 6%. Margin recovery has been pushed out in time, while the company continues to operate in an environment of high promotional activity and markdowns.

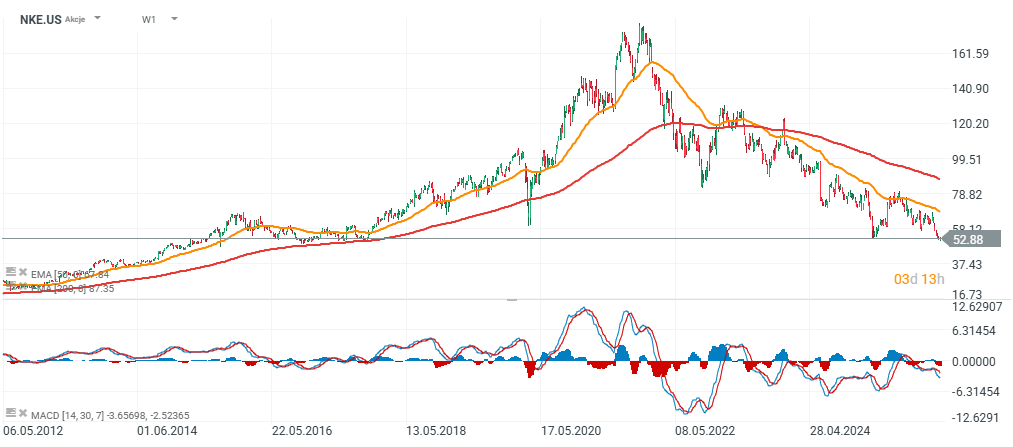

NKE (W1 interval)

Source: xStation5

Will EssilorLuxottica and L'Oréal acquire part of the Giorgio Armani brand❓

AU200.cash: mixed signals from the Australian economy ⚔️

Oracle is laying off thousands of employees — AI is replacing jobs🤖

BREAKING: IRGC threatens to attack Microsoft, Apple, and Alphabet ⚔️

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.