The second quarter of 2026 revealed a very interesting divide within the U.S. banking sector. Goldman Sachs and Citigroup released their earnings reports one after another, and both banks significantly exceeded analysts’ expectations. Despite this, the market reaction was completely different. Goldman Sachs shares were rewarded with a rise, while Citigroup faced selling pressure.

This was not a coincidence or simply a matter of the size of their earnings. Both banks benefited from improving financial market conditions, higher client activity, and a more favorable environment for investment-related businesses. The difference, however, lies in the fact that investors evaluate these two institutions using completely different criteria.

Goldman Sachs is currently viewed as one of the biggest beneficiaries of the Wall Street recovery. Increased merger and acquisition activity, a higher number of securities issuances, and favorable trading conditions are quickly translating into stronger results for the bank.

Citigroup, meanwhile, is at a different stage of its investment story. In this case, the market is no longer evaluating only a single quarter, but rather the effectiveness of its multi-year transformation, improvements in efficiency, and its ability to generate higher returns for shareholders. The same market cycle has therefore created two completely different investment narratives.

Goldman Sachs Q2 2026: A Record Quarter Confirms the Strength of Its Business Model

Goldman Sachs entered the second half of 2026 with one of the strongest quarters in its history. The bank significantly exceeded analysts’ expectations in both revenue and earnings, while also demonstrating exceptionally strong returns on capital.

Key financial results:

-

Net revenues: $20.34 billion

-

GAAP EPS: $20.98

-

ROE: approximately 23.5%

-

Global Banking & Markets: $15.52 billion in revenue

-

Asset & Wealth Management: $4.60 billion in revenue

-

Operating expenses: $11.67 billion

-

Efficiency ratio: 57.4%

-

Quarterly dividend: $5.00 per share

The scale of the earnings beat was significant enough that the report effectively removed previous concerns regarding Goldman’s ability to return to very high profitability in a more favorable market environment.

However, the most important aspect of this report is not only how much the bank earned. The key factor is its ability to convert supportive market conditions into very high shareholder returns. In the case of investment banks, revenue scale alone is not enough. What matters is capital efficiency and the ability to sustain high profitability.

Goldman Sachs once again demonstrated that its business model performs particularly well during periods of increased activity across financial markets.

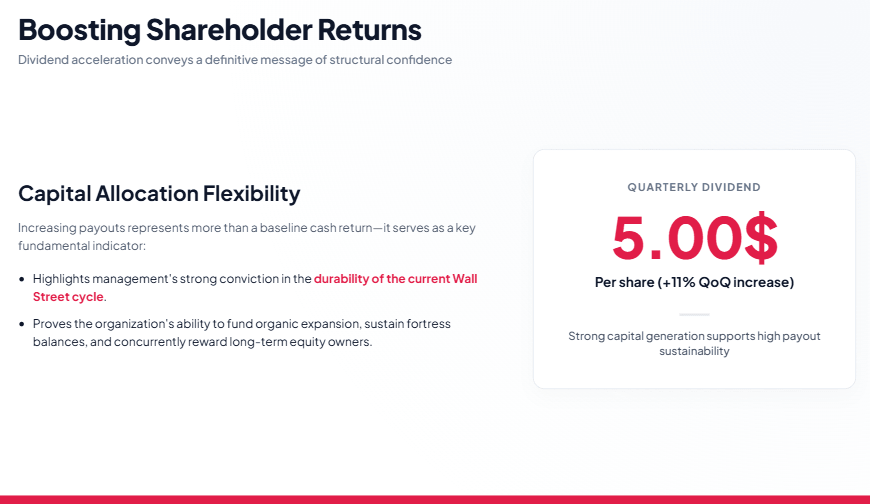

Dividend Increase as a Signal of Management Confidence

One of the most important messages from Goldman Sachs was the decision to increase its quarterly dividend to $5 per share, representing an increase of approximately 11% compared with the previous level.

Such a move carries significance beyond the direct payout to shareholders. It also provides insight into management’s view of the company’s future prospects. Goldman is signaling that it has sufficient capital strength to simultaneously grow its business, maintain a strong balance sheet, and increase shareholder returns.

The market interpreted this decision as confirmation that management remains confident in the sustainability of the current improvement in results.

What Drove Goldman Sachs’ Performance?

The main growth engine remained the Global Banking & Markets division, which generated $15.52 billion in revenue.

The key factors supporting results included:

-

higher institutional client activity,

-

improving conditions in the mergers and acquisitions market,

-

increased securities issuance volumes,

-

favorable trading conditions.

This segment remains at the center of Goldman Sachs’ investment case.

In previous periods, investors had pointed out that the recovery in earnings was uneven. Very strong equity trading performance contrasted with weaker areas of market activity. The latest report, however, shows a much broader improvement.

Goldman is no longer relying on a single source of revenue. The bank is benefiting from a broad recovery in capital markets activity and translating it into stronger results across the entire organization.

Asset & Wealth Management Improves the Quality of Goldman Sachs’ Earnings

Another important element of the report was the Asset & Wealth Management segment, which generated $4.60 billion in revenue. The importance of this business continues to grow because it provides Goldman Sachs with more stable sources of income and reduces its dependence on the most cyclical areas of its operations.

Trading and investment banking remain the most profitable segments of the bank, but they are also highly dependent on market conditions. The expansion of asset and wealth management allows Goldman to build a more balanced and resilient business model.

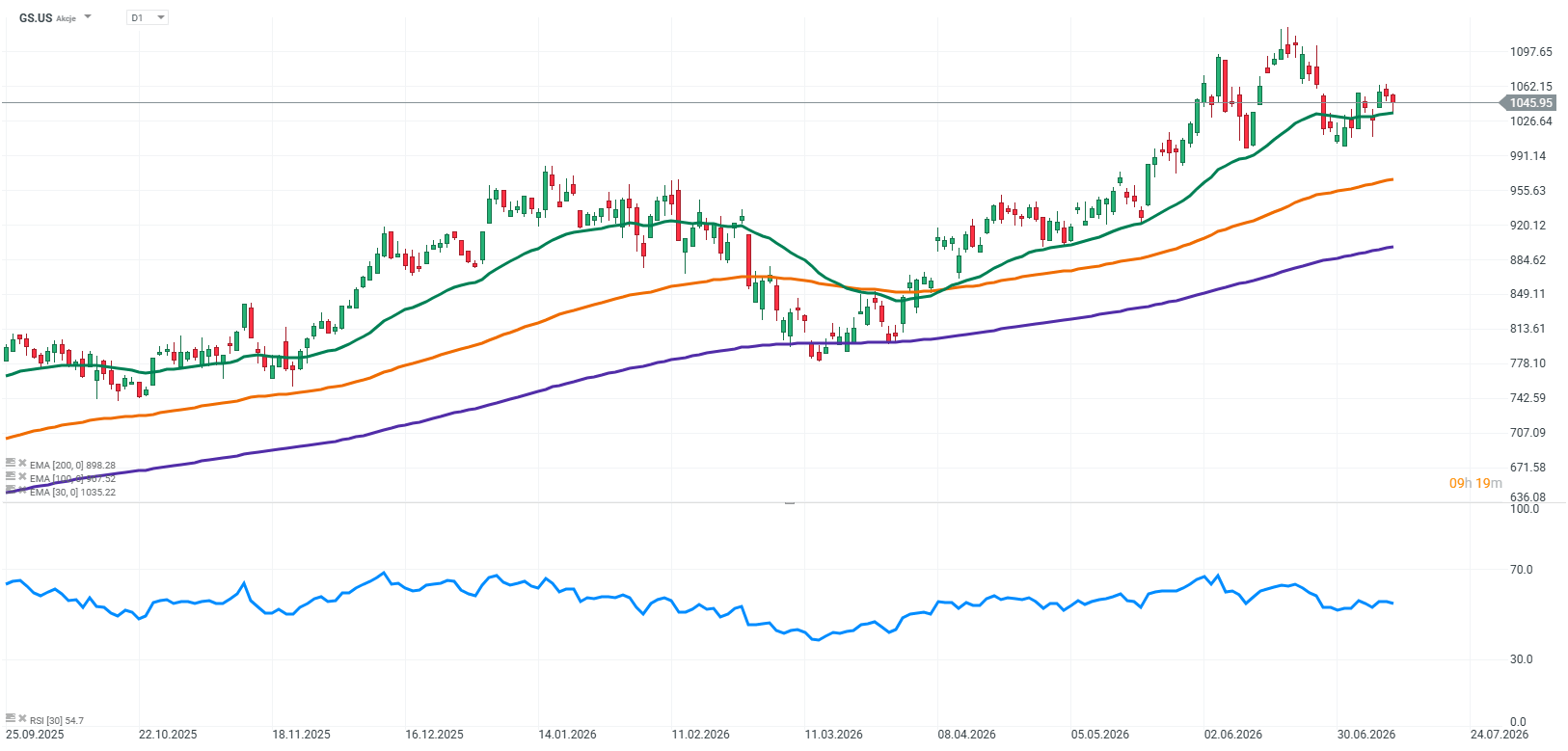

Source: xStation5

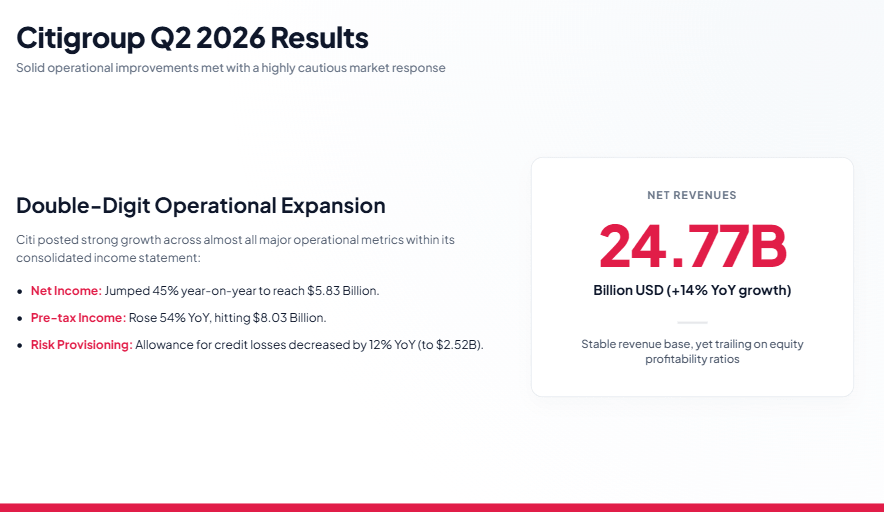

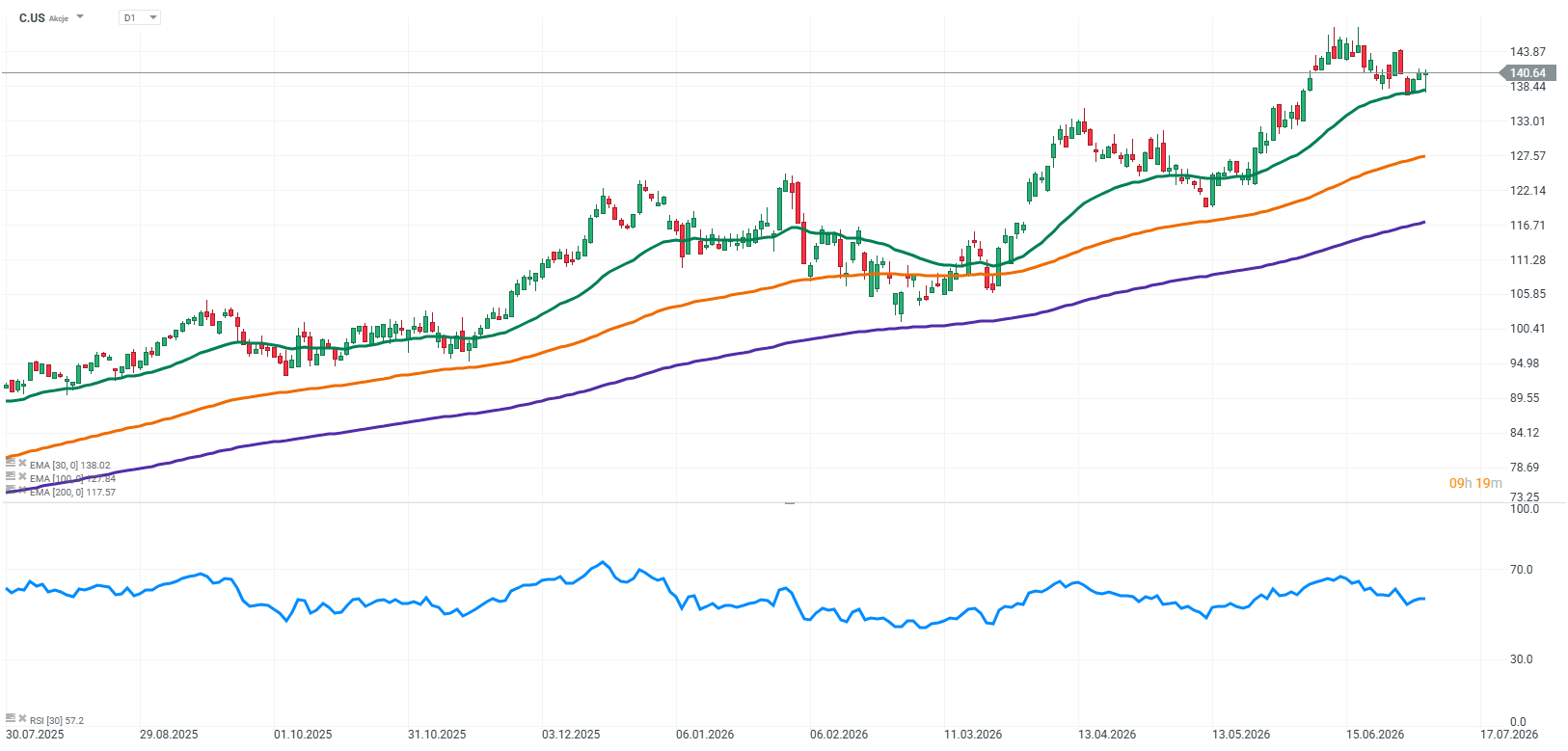

Citigroup Q2 2026: A Strong Report, but the Market Wanted More

Citigroup also delivered very solid results for the second quarter of 2026. The bank exceeded analysts’ expectations in both revenue and net income, yet the market reaction was negative.

Key financial results:

-

Net revenues: $24.77 billion (+14% YoY)

-

Net income: $5.83 billion (+45% YoY)

-

GAAP EPS: $3.15

-

Pre-tax income: $8.03 billion (+54% YoY)

-

Operating expenses: $14.22 billion (+5% YoY)

-

Credit loss reserves: $2.52 billion (-12% YoY)

-

Net credit losses: $2.40 billion (+8% YoY)

-

ROTCE: 13.0%

-

ROE: 11.4%

-

CET1 ratio: 12.8%

-

Efficiency ratio: 57.4%

The report itself was not weak. Quite the opposite — Citi demonstrated a clear improvement in financial performance. Revenue increased by 14% year over year, while net income rose by as much as 45%. Improvement was also visible at the pre-tax income level, which increased by 54%.

The issue was therefore not the quality of the quarter itself. The issue was the investment narrative.

Goldman Sachs had to answer the question of whether it could capitalize on improving market conditions. Citigroup must answer whether its current improvement represents the beginning of a lasting transformation in business quality.

This is a fundamental difference.

Costs, Efficiency, and Capital at Citi

One of the positive aspects of Citigroup’s report was cost control. Operating expenses amounted to $14.22 billion, representing only a 5% increase year over year. Cost growth was therefore significantly slower than revenue growth.

As a result, the efficiency ratio improved to 57.4%. This is a key element of management’s strategy, as one of Citi’s main transformation goals is to simplify the organization and improve the relationship between costs and revenue generation.

The bank’s capital position also remains strong. A CET1 ratio of 12.8% provides a solid safety buffer, while the increase in book value per share indicates an improvement in Citi’s capital position.

At the same time, profitability remains the key area watched by investors. ROTCE of 13% and ROE of 11.4% demonstrate improvement compared with the previous year, but they are still below the levels achieved by the most efficient investment banks.

Why Did Citi Fall Despite Beating Expectations?

The first reason is the difference in business structure.

Goldman Sachs is much more focused on investment banking, trading, and capital markets. During periods of improving investor sentiment, such a model allows the bank to generate very rapid earnings growth.

Citigroup operates a much more diversified business model, including consumer banking, corporate banking, payments, and market activities. This provides greater stability but also limits the upside during periods of a strong Wall Street rebound.

The second issue is organizational transformation.

Citi has spent several years simplifying its structure and investing in efficiency improvements. Over the long term, these changes could create a significantly better business. However, in the short term, the bank still needs to convince investors that these efforts will translate into sustainable improvements.

The third factor is Citi’s greater exposure to consumer banking.

If economic conditions deteriorate, investors will pay close attention to credit quality, loan losses, and the financial health of retail customers.

Goldman Sachs and Citigroup: Two Different Strategies Within the Same Sector

The key difference between the two banks comes down to their investment profiles.

Goldman Sachs is a direct beneficiary of Wall Street’s recovery. If the markets for mergers and acquisitions, capital raising, and trading remain strong, the bank has the potential to generate exceptionally high shareholder returns.

Citigroup, on the other hand, represents a more diversified business model. The bank is less dependent on a single market cycle, but it also requires more time for improving financial performance to translate into a more favorable perception among investors.

In other words, Goldman Sachs is a cyclical recovery story, while Citigroup is a transformation story.

Source: xStation5

Why Did the Market Buy Goldman and Sell Citi?

The most important conclusion from both earnings reports is that the market does not reward companies simply for beating expectations. What matters is whether the results change the long-term investment narrative.

Goldman Sachs demonstrated that the current market environment can translate into exceptionally high profitability and stronger shareholder returns. The report confirmed that the bank remains one of the primary beneficiaries of the ongoing recovery in capital markets.

Citigroup is improving its financial performance, but it still needs to prove that its organizational transformation will lead to a lasting improvement in the quality of its business.

Investment Takeaways

The second quarter of 2026 demonstrated that the recovery on Wall Street is real, but not every bank is benefiting to the same extent.

Goldman Sachs remains one of the biggest beneficiaries of the current market environment. The bank has once again proven its ability to convert stronger capital markets activity into exceptional profitability and higher returns for shareholders.

Citigroup also delivered a solid earnings report. However, its investment case remains far more dependent on the successful execution of its transformation strategy and its ability to achieve sustainable improvements in operational efficiency.

The results of both banks highlight one important lesson:

A recovery on Wall Street does not automatically create winners across the entire banking sector. Investors are rewarding institutions whose earnings reinforce a compelling long-term investment story—not merely those that beat quarterly expectations.

US Open: Nasdaq 100 gains 1% 🔼 Software stocks decline, JP Morgan rises after earnings

Software stocks slide on enterprise spending concerns 🚩 Microsoft drops 3%

Worse than the Dot-com bubble: IBM stock crash

JPMorgan reports strong Q2 earnings as investment banking drives growth