Cryptocurrencies and commodities are leading the gains at the start of the day, whilst the main stock market indices remain slightly in the red ahead of the opening of the European cash market.

Today’s key macroeconomic figures

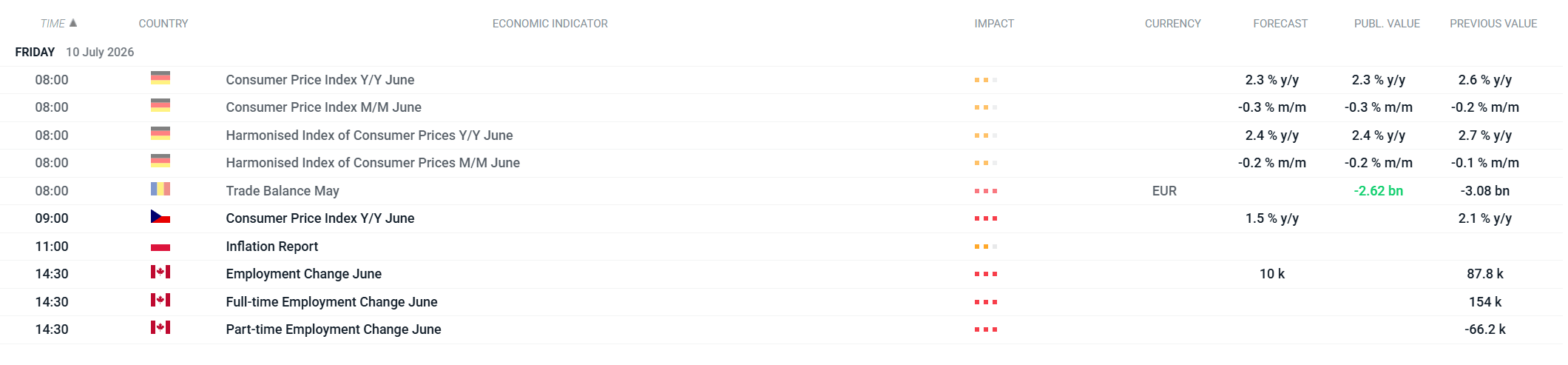

The day will be dominated by inflation data from Europe – the German CPI and HICP figures for June confirmed final readings of 2.3% y/y (CPI) and 2.4% y/y (HICP), down from May’s 2.6% and 2.7%. The Czech CPI for June (09:00) is expected to slow to 1.5% y/y from 2.1% y/y, which, alongside Poland’s reading of 2.5% y/y and Governor Glapiński’s dovish tone yesterday, is in line with the regional trend of disinflation. This afternoon (14:30), attention will turn to the Canadian labour market report – the forecast is for just 10,000 new jobs, compared with 87,800 the previous month, which, given the risk of a negative surprise, could reinforce expectations of interest rate cuts by the Bank of Canada.

Source: xStation

Market sentiment ahead of the opening

Bitcoin is up 1.00% and is trading around $63,760–$63,950, continuing the positive sentiment in the cryptocurrency market seen in recent days. WTI crude oil (+0.57%, $72.22–$72.28) and Brent crude oil (+0.49%, $76.42–$76.47) are rising following a week of recovery from their lows, buoyed by tensions surrounding the Strait of Hormuz. Silver (+0.30%) is gaining ground, whilst gold (-0.27%, approx. $4,112) is down slightly, suggesting limited appetite for safe-haven assets compared with recent weeks.

Indices and currency pairs – the highest volatility

Futures on US indices are clearly in negative territory – the US100 (-0.37%) and US500 (-0.16%) are falling the most among the indices, in contrast to Thursday’s solid rebound, which was driven by a rally in semiconductor stocks. European futures remain more stable: the UK100 is up 0.36%, whilst the DE40, EU50 and SPA35 are recording slight falls of between 0.07% and 0.26%. In the foreign exchange market, USDJPY is showing the most significant movement (-0.45%, 161.60), confirming the yen’s strengthening following Finance Minister Katayama’s announcements regarding an increase in the GPIF’s investment in domestic assets.

Corporate events in the spotlight

SK Hynix’s Nasdaq debut via ADRs is the main event of the trading session – the offering attracted more than seven times the demand during the book-building process and is expected to raise as much as US$24.5 billion. The market will also be watching Delta Air Lines’ quarterly results, which will set the tone for the aviation sector at the start of the US trading session.

Daily Summary: The week ends on a positive note. SK Hynix up 14% on Nasdaq. Energy down (10.07.2026)

Three markets to watch next week (10.07.2026)

Fed presents its semi-annual report. Stocks are expensive but no bubble?

BREAKING: Iran and US are back at the negotiation table?! Oil takes a step back, stocks tick up!