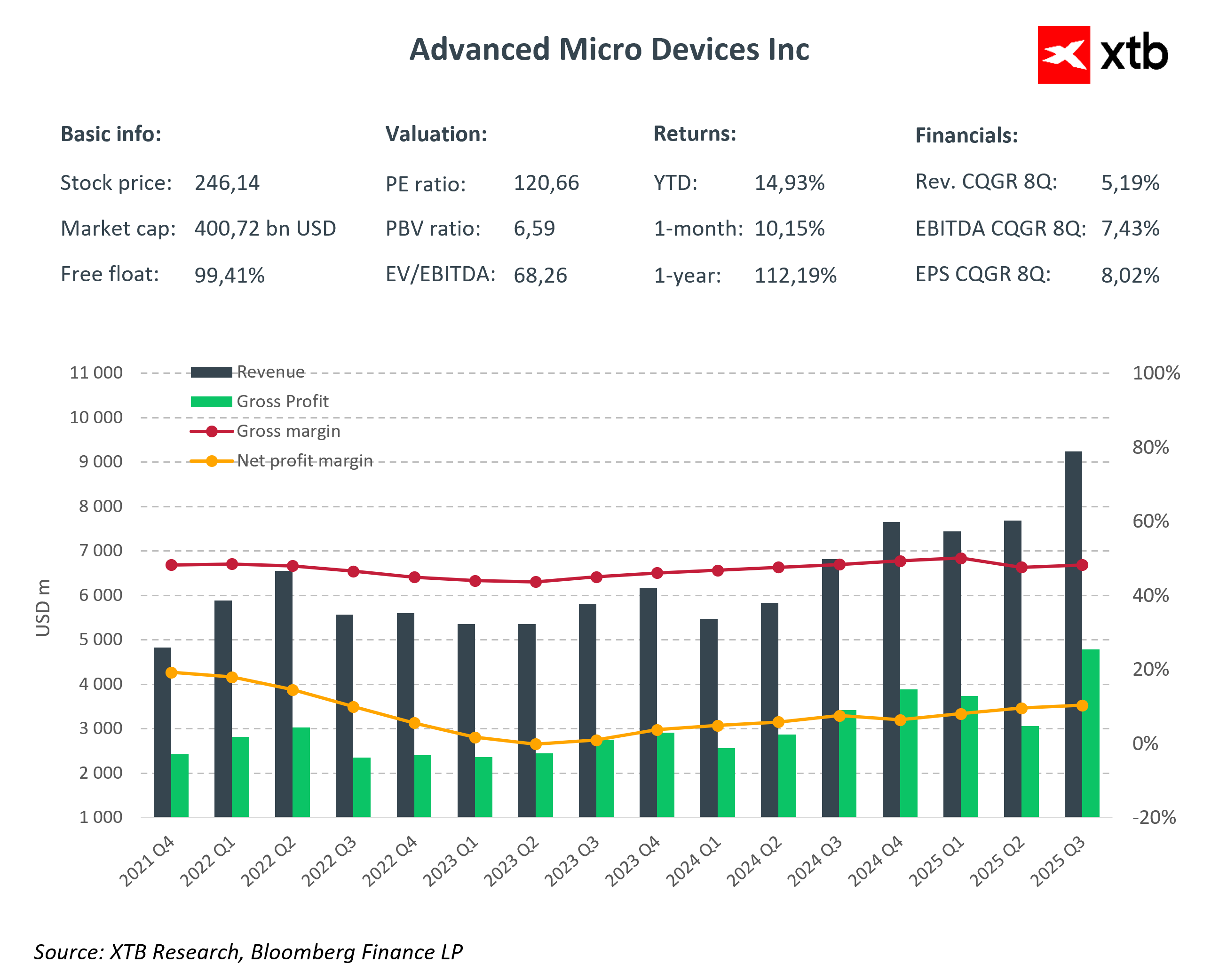

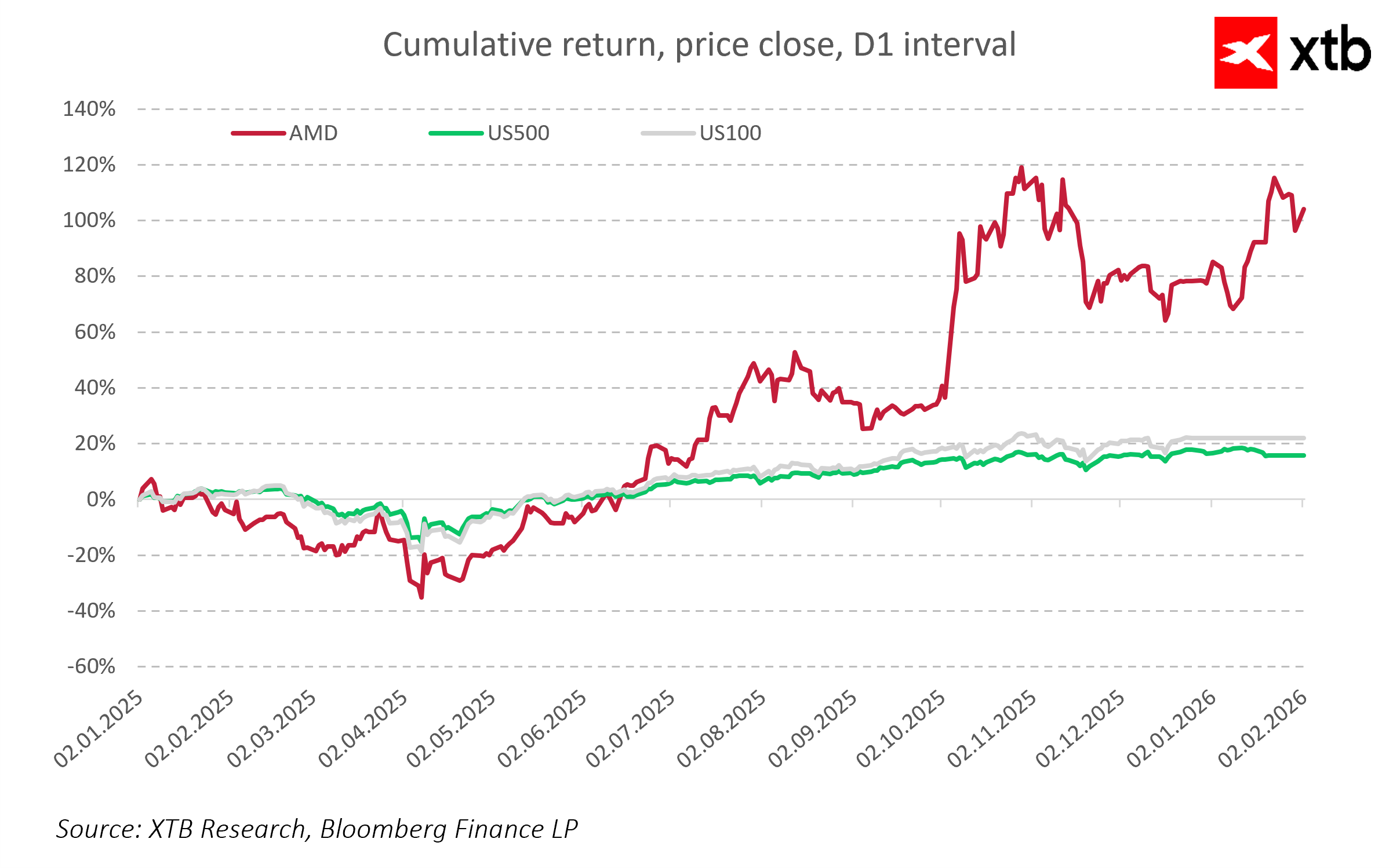

Why AMD’s Results Matter

AMD enters earnings season as one of the key players in the global semiconductor sector. The company balances between the traditional CPU market and the dynamically growing GPU and AI accelerator segment, where it competes with giants such as Nvidia. After years of consistent expansion in data centers and increasing AI engagement, the market expects concrete evidence of AMD’s ability to maintain its competitive edge under conditions of high stock valuations, limited chip supply, and rising competition. Q4 2025 results will serve as a test of growth quality and will show whether the company can convert momentum in the CPU segment and developments in GPU and AI into tangible financial results while maintaining control over costs and investments in the future.

Q4 2025 Financial Forecasts

-

Adjusted EPS: 1.32 USD

-

Total revenue: 9.65 billion USD

-

Data center revenue: 4.97 billion USD

-

Gaming revenue: 855.3 million USD

-

Client (PC) revenue: 2.89 billion USD

-

Embedded revenue: 960.7 million USD

-

Operating income: 2.47 billion USD

-

Operating margin: 25.4%

-

Gross margin: 54.5%

-

CapEx: 231.4 million USD

-

R&D expenses: 2.16 billion USD

Q1 2026 Forecasts

-

Total revenue: 9.39 billion USD

-

Gross margin: 54.3%

-

CapEx: 213.9 million USD

CPU – The Core of the Traditional Market

AMD continues to gain market share in server processors, where its x86 chips show performance advantages over Intel. Intel’s supply constraints and growing demand for high-performance servers create an opportunity for AMD to further strengthen its position. Momentum in CPUs remains the main driver of revenue growth and a key factor the market will closely monitor.

GPU – Competing with Nvidia

In the graphics processor segment, AMD is still catching up to Nvidia, particularly in the server GPU market. The launch of new Instinct MI455 chips and preparations for Helios deployments for OpenAI show that the company is targeting the growing demand for AI workloads. The pace of GPU adoption in data centers will be an important indicator of AMD’s ability to compete in the artificial intelligence segment.

AI and Collaboration with OpenAI

AMD has invested significant resources in AI development, planning deployments of six-gigawatt systems for OpenAI. This partnership represents the first major test of AMD’s AI strategy and could define growth momentum in this segment. Key questions for the market include whether AMD will expand its AI customer base, how quickly it can scale deployments, and whether investments in GPUs deliver adequate returns.

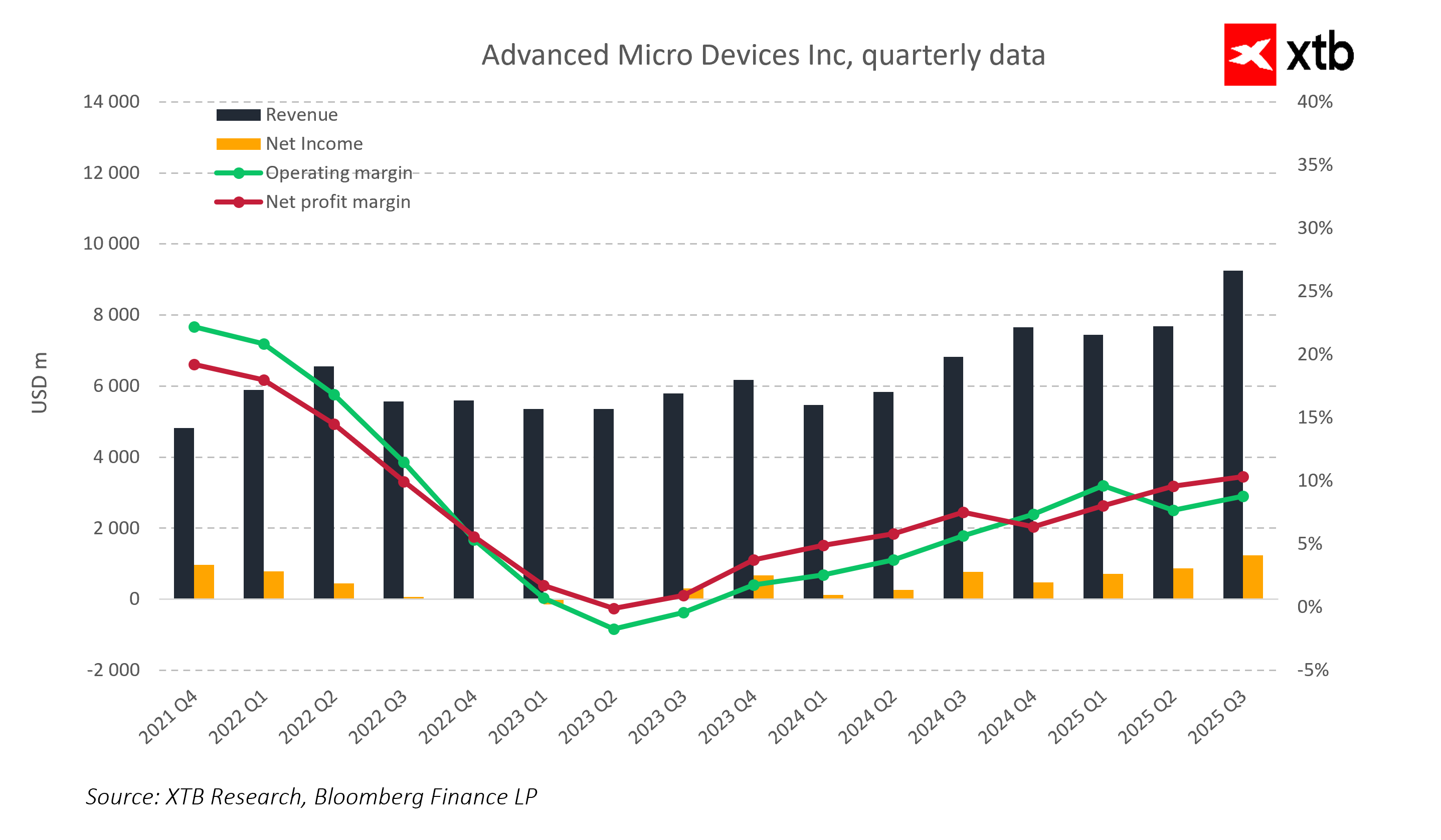

Growth Dynamics and Competitive Analysis

AMD remains a leader in the server CPU segment, leveraging performance advantages over Intel and its rival’s production constraints. This allows the company to gain an increasing share of the data center market, where processor performance and energy efficiency are key selection criteria. In GPU and AI, AMD is still trailing Nvidia, but the OpenAI partnership and the development of new Instinct MI455 and MI400 models create a real opportunity for breakthroughs in server AI workloads. Helios deployments could be a milestone in AMD’s AI strategy, demonstrating how the company handles growing demand for generative AI. The market will closely watch revenue growth from data centers and GPUs, the effectiveness of AI deployments, the ability to expand the customer base in this segment, and the dynamics of the PC market, which continues to support revenues but may be constrained by rising memory costs and consumer demand fluctuations.

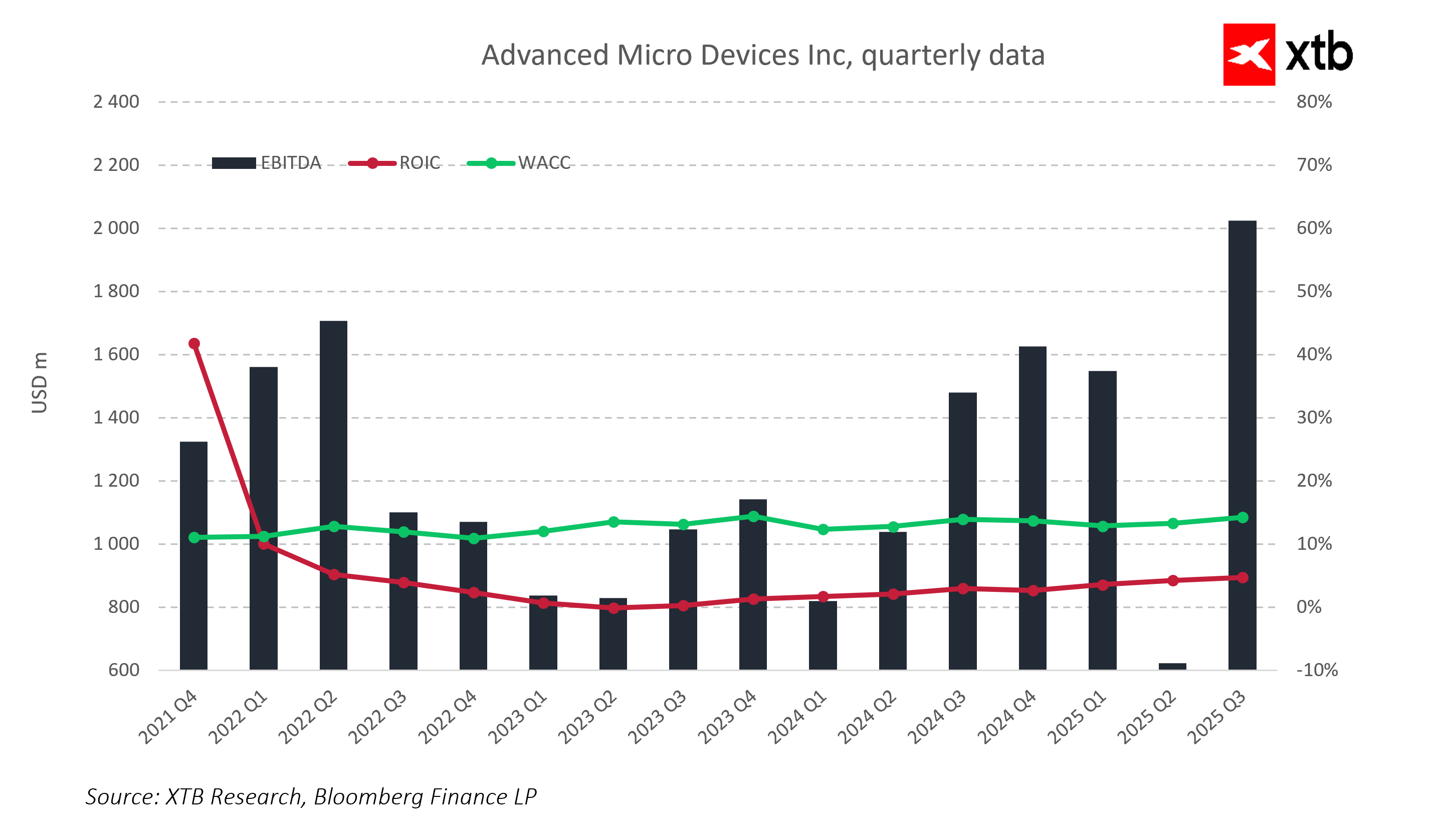

CapEx and Margins

Investments in data centers, GPUs, and AI are growing faster than revenues, creating cost pressures and requiring careful margin management. Investors will focus on management commentary regarding ROI, the schedule for AI GPU deployments, and the efficiency of new technology expenditures. Not only the speed of growth is important, but also its quality and AMD’s ability to scale operations profitably. Analyzing gross and operating margins alongside investments will help assess whether the company can effectively convert spending on data centers and AI into real financial results without compromising long-term profitability.

Investor Risks

Despite its strong market position, AMD faces several challenges. Competition in the CPU segment from Intel and in GPU and AI from Nvidia remains intense. Additionally, the entry of Arm into the server segment may increase pressure. High dependence on a key AI client, OpenAI, means the pace of partnership execution will significantly impact company results. Risks are further heightened by chip supply constraints, rising memory and energy costs for data centers, and potential regulatory and geopolitical changes that could affect raw material availability and operational costs.

Strategy Quality Test

Q4 2025 will be a test of whether AMD can effectively scale CPU and GPU sales in servers, expand AI partnerships with rising investment levels, maintain its competitive edge, and simultaneously generate free cash flow amid rising costs. The results of this quarter will show how well AI and data center investments translate into tangible financial outcomes, whether the company can maintain CPU growth momentum, expand its GPU and AI customer base, and control margins. Success in this quarter could confirm the effectiveness of AMD’s strategy, signaling to the market a durable competitive advantage and preparing the company for the next stage of value expansion.

Key Takeaways

-

AMD must prove it maintains performance advantages in server CPUs and can continue growing in the data center market.

-

The company must show that revenue growth from GPUs and AI deployments, including the OpenAI partnership, translates into tangible financial results.

-

AMD must demonstrate it can control costs amid rising investment levels, which will test the quality and efficiency of growth.

-

The company must prove that stability in PC and gaming segments allows aggressive AI and data center investments without excessive risk to cash flow.

-

Today’s Q4 2025 report will be an opportunity for AMD to confirm its lasting competitive advantage and show that its strategy drives further value growth.

US Open: US100 slides 0.5% under pressure from IT sector 📉ServiceNow drops 6%

Palantir after earnings: another quarter, another record

Merck: Mixed Results, but Key Drugs Continue to Drive Growth

Polish stocks lead gains in Europe 📈W20 surges 2%

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.