Today, Wall Street investors received mixed signals from the U.S. economy, analyzed against the backdrop of fragile geopolitical conditions in the Middle East and persistently high oil prices. Data showed that U.S. consumer spending in February rose as expected by 0.5% month-over-month, while core PCE inflation remained at 0.4%, indicating that consumption continues to support the economy despite significant cost pressures on households. Personal income fell by 0.1%, and initial jobless claims came in above forecasts, suggesting that the labor market is beginning to show signs of slight cooling.

Gross Domestic Product in the fourth quarter grew more slowly than previously estimated, reaching just 0.5% annualized. During the same period, household spending increased by only 1.9%, signaling a clear slowdown in economic growth, although consumers continue to support expansion. Inflation, measured by the GDP deflator and core PCE, remains moderate at 3.7% quarter-over-quarter and 2.7% year-over-year.

These figures are overlaid with a highly fragile geopolitical situation. After the announcement of a conditional ceasefire between the U.S. and Iran, which was meant to give markets some relief, the parties’ statements proved contradictory. Iran accuses Israel of continuing attacks in southern Lebanon, threatening to withdraw from the truce, while the U.S.-Israeli side maintains that Israel’s actions in Lebanon were not part of the formal agreement and therefore do not violate its terms. This discrepancy keeps peace fragile and regional escalation risks high.

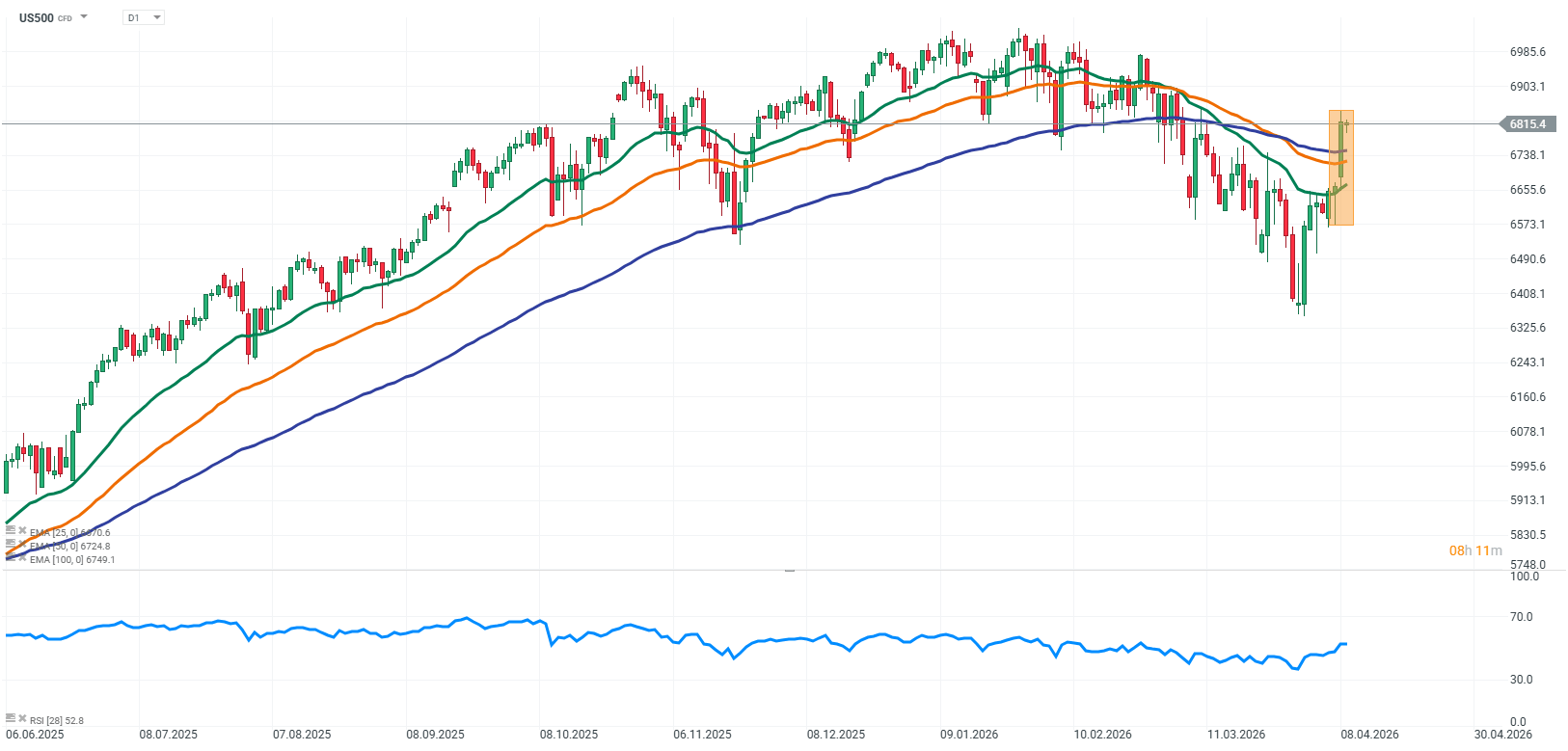

Oil prices remain elevated, sustaining cost pressures in the economy and impacting inflation. High energy costs translate into higher transport and production expenses, limiting room for interest rate cuts and dampening investors’ risk appetite. Equity markets are cautious, with the S&P 500 and Nasdaq slightly down, reflecting investor uncertainty as they balance solid yet slowing macro readings against an unstable geopolitical backdrop.

GDP growth in Q4 was weaker than initially estimated, and private consumption is growing moderately. Inflation remains stable but is not falling enough to clearly indicate the Fed’s next moves. Today’s data do not make the Federal Reserve’s interest rate decisions any easier, but markets agree that upcoming releases will be far more important and likely to provide clearer signals about the direction of monetary policy.

Source: xStation5

U.S. Equity Futures

S&P 500 (US500) futures are showing slight losses today. The market is reacting not only to moderately weaker U.S. macro readings, which suggest a slowdown in economic growth, but primarily to rising geopolitical uncertainty around Iran and the Middle East. Regional tensions and conflicting statements regarding the conditional ceasefire maintain investor caution, limiting risk-taking.

Source: xStation5

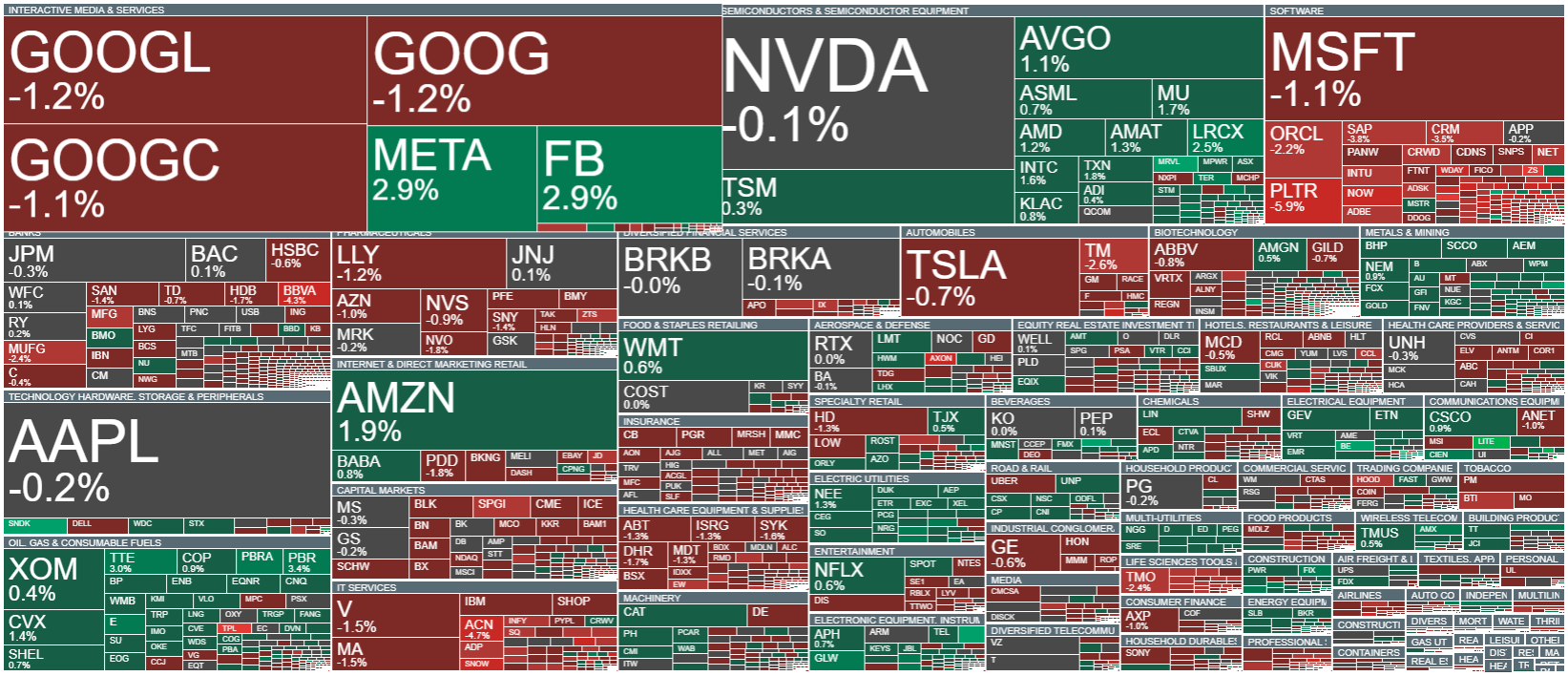

Company News

CoreWeave (CRWV.US) announced an expanded long-term partnership with Meta Platforms (META.US) through a new deal worth approximately $21 billion, providing cloud computing power for AI projects through the end of 2032. The agreement builds on the existing partnership and underscores Meta’s growing AI infrastructure needs and CoreWeave’s role as a key computing provider.

Chevron (CVX.US) is gaining in pre-market trading after announcing that although Q1 production fell partly due to the impact of the Iran war, higher oil and gas prices significantly boosted upstream earnings. The company expects extraction profits to be $1.6–2.2 billion higher than in the previous quarter, despite volume constraints from downtime in Central Asia and lower output in the Middle East.

Applied Digital (APLD.US) shares are down following its Q3 fiscal results, despite revenue growth and improved operating performance. Net income remains negative, but adjusted EBITDA is rising, and management emphasizes expansion in the AI data center segment and the development of new AI infrastructure campuses.

Oracle (ORCL.US) is expanding its AI-based offerings, introducing a suite of agent-driven applications designed to automate tasks in finance, HR, supply chain, and customer service. The new tools aim to enhance operational efficiency for companies using Oracle Cloud and attract more clients to the platform.

Amazon (AMZN.US) and Eli Lilly (LLY.US) are in the spotlight after Amazon Pharmacy announced it will begin selling a newly FDA-approved weight-loss pill. The product will be available in Amazon locations with same-day delivery, opening a new market segment for Amazon and potentially impacting demand for Eli Lilly products.

A New Chapter for BlackBerry: QNX at Record Levels

Stock of the Week – ASML: The Silent Monopolist Behind AI

Intel on a winning streak 📈

BREAKING: U.S. PCE Data In Line with Expectations. EURUSD shows no reaction!

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.