Nvidia has long been one of the most important players in the world of artificial intelligence. The company, which started in the gaming market, now accounts for a significant portion of the global computing infrastructure powering the latest generative models as well as solutions used in science and industry. Its chips drive data centers, research labs, and enterprises building advanced AI systems.

The latest financial results for the third quarter of fiscal year 2026 confirm that demand for AI accelerators continues to grow. The data center segment has not only strengthened its lead but also demonstrated Nvidia’s ability to scale operations without compromising quality and performance. The company is simultaneously developing entire technology ecosystems, including software, networks, and platforms that enable the creation and training of complex models at scale.

This report analyzes the most recent quarterly data, discusses developments across each key business area, and highlights the main factors that may influence the company’s future. Before we take a broader look, let’s start with the key financial figures for the third quarter of fiscal year 2026.

Outstanding results for Q3 2026

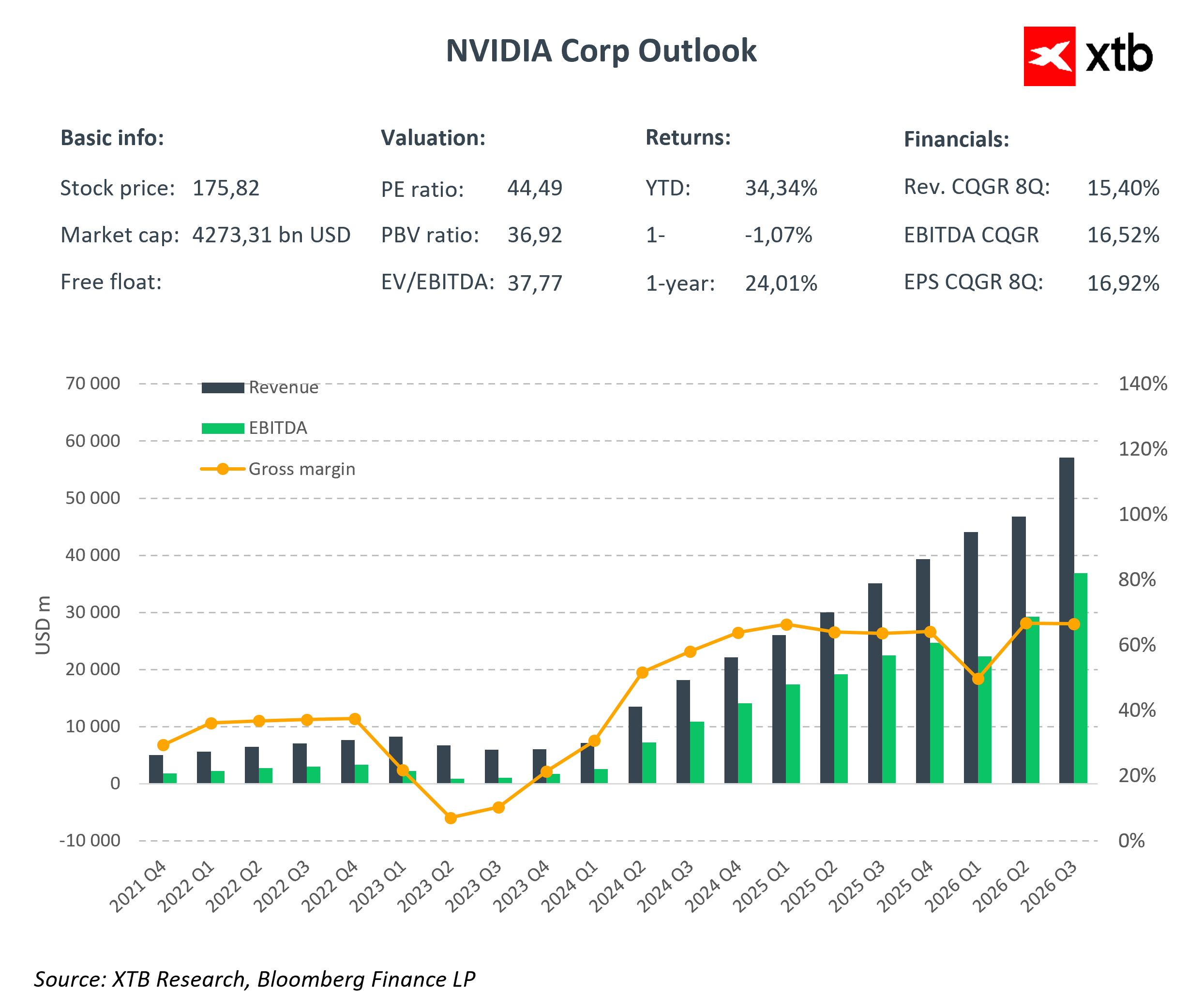

Nvidia once again proved its crucial role in AI development by posting revenues of 57 billion USD in Q3 2026. This represents a 22% increase over the previous quarter and a 62% year-over-year growth. Such growth is not just about scale; it clearly demonstrates Nvidia’s dominance in the global digital transformation.

Gross margin remains very high at around 73.4%. Despite heavy investments in research, development, and operational expansion, the company effectively converts revenue into profit. Operating expenses, including R&D and administration, totaled 5.839 billion USD, while operating income reached 36 billion USD. On a net basis, Nvidia generated nearly 32 billion USD, translating to earnings per share of 1.30 USD. This result exceeded analyst expectations and shows the company’s ability to generate strong cash flows even amid macroeconomic uncertainty.

The main growth driver remains the data center segment, with record revenues of 51.2 billion USD. This is driven not only by increasing demand but also by the innovative Blackwell GPU architecture, which combines high performance with energy efficiency, and strategic partnerships with major players in cloud and AI industries. This solidifies Nvidia’s position as the foundation of global AI infrastructure. The gaming segment also holds a strong position, generating 4.3 billion USD in revenue, reflecting a balanced business model that combines consumer innovation with the data center business.

For the next quarter, Nvidia forecasts revenues around 65 billion USD while maintaining high margins, demonstrating its ambition not only to sustain but also to strengthen its dominance.

The company’s success is not based solely on recent results. Analysis of recent years shows consistent outperformance of market expectations in both revenue and earnings per share. Before Q3 2026, forecasts projected revenues of about 55.2 billion USD and EPS of 1.26 USD; the actual results exceeded these estimates. This consistency reflects the company’s stable and sustainable growth and its ability to operate effectively in a rapidly evolving tech sector. This builds investor confidence and underscores Nvidia’s role as one of the pillars of the global technological revolution.

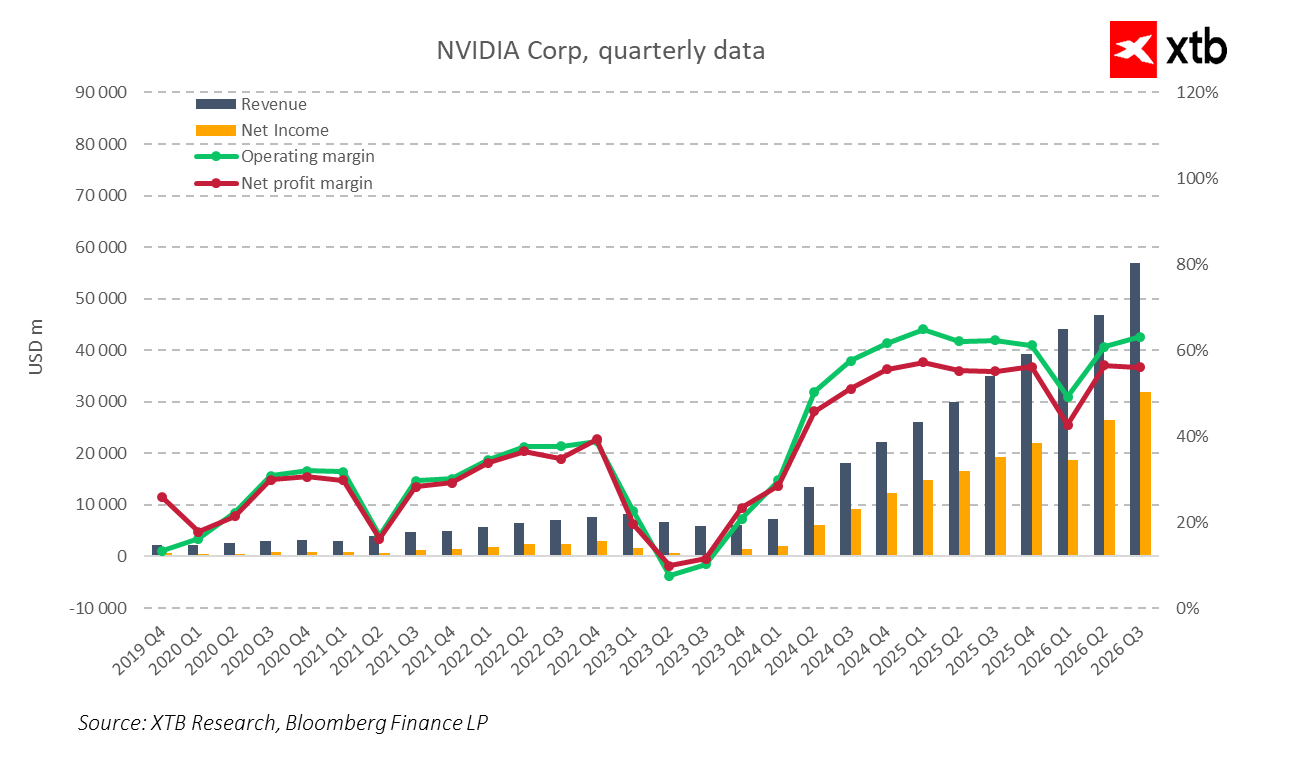

Quarterly financial data confirm the company’s impressive growth. Revenues have grown dynamically since 2023, reaching record highs. Net profits are also approaching 32 billion USD. Stable and high operating and net margins indicate effective cost control and operational efficiency.

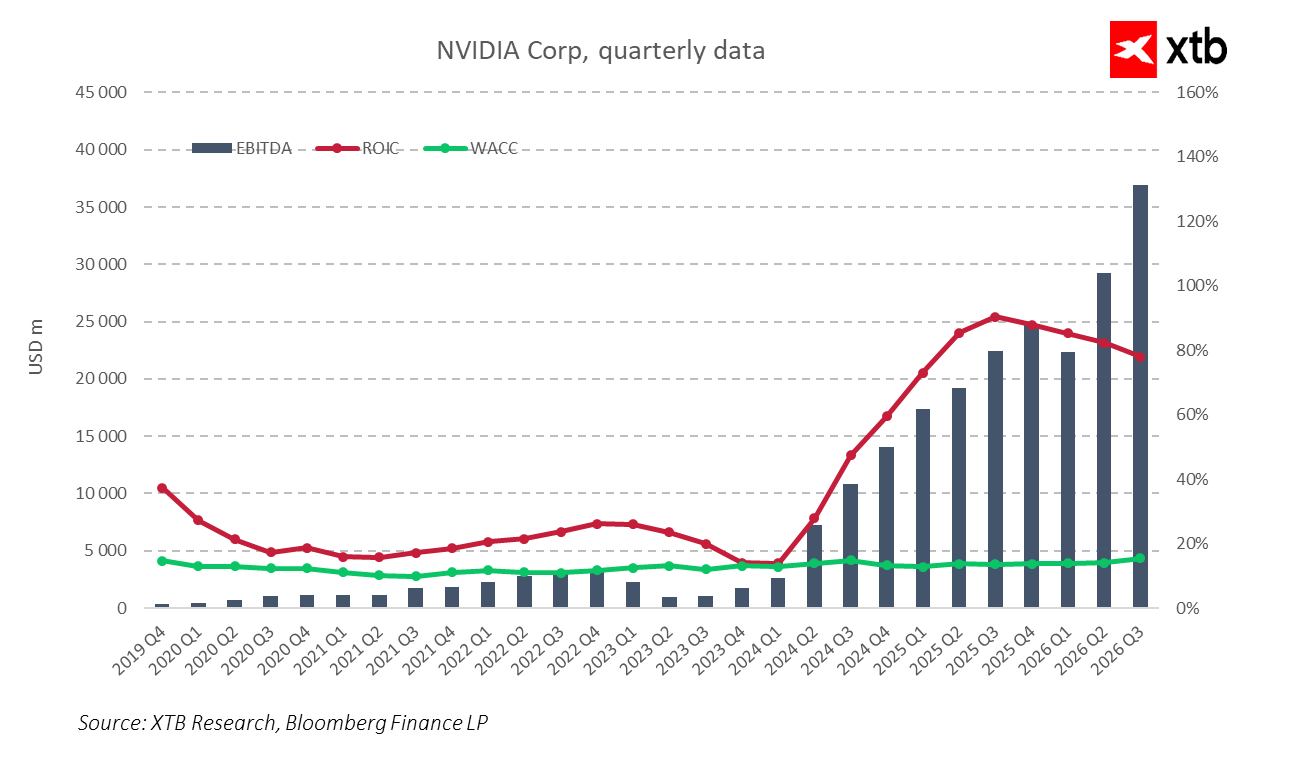

EBITDA is growing rapidly, surpassing 37 billion USD in Q3 2026. The return on invested capital remains above 80%, indicating exceptional resource management efficiency. A relatively low cost of capital highlights a strong competitive position and the ability to generate value for shareholders. This combination of growth, profitability, and efficient management forms a solid foundation for further development and leadership strengthening in the industry.

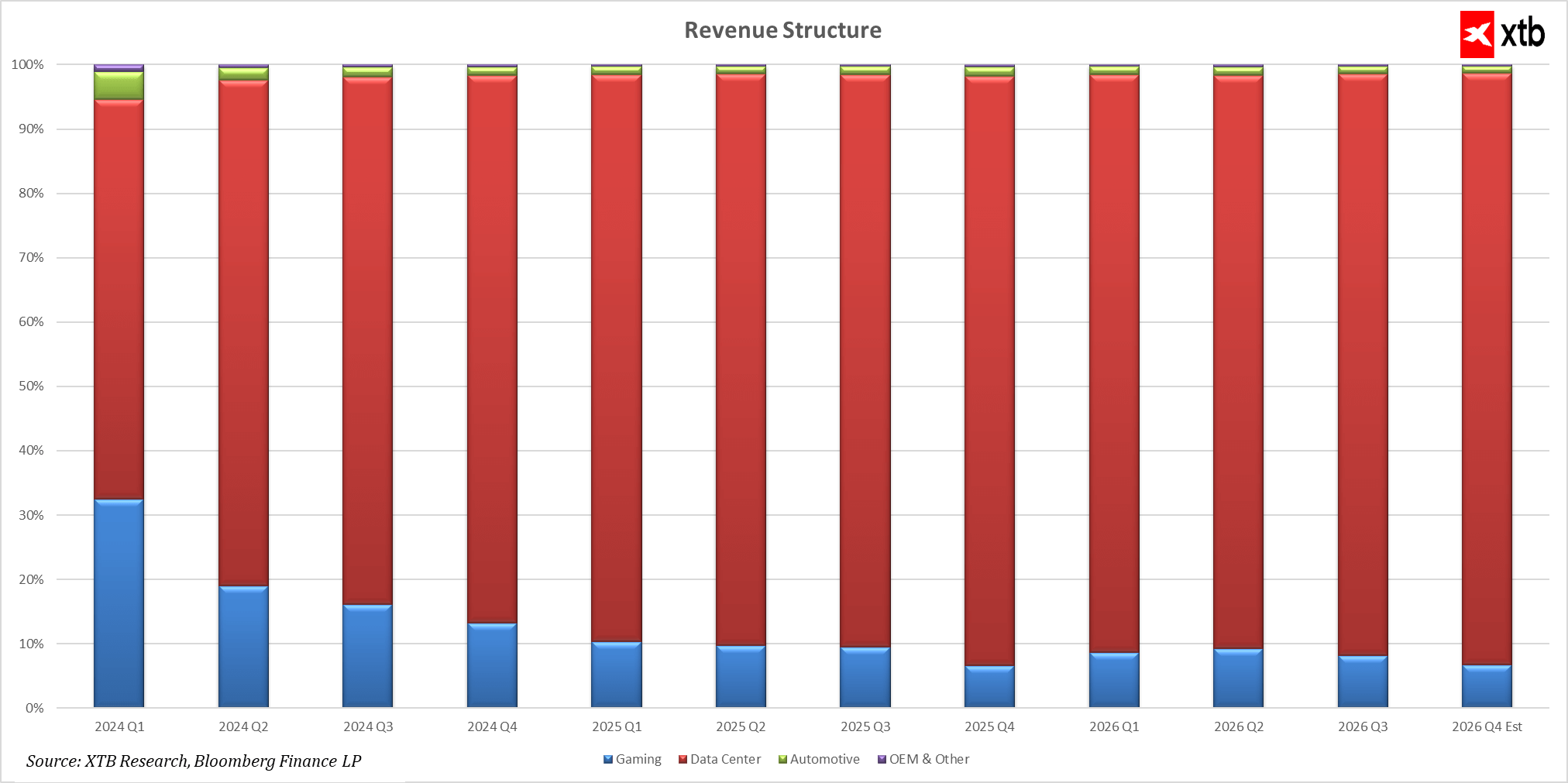

Nvidia consistently strengthens its position mainly through rapid growth in the data center segment. Since early 2024, revenues in this area have increased at an impressive pace, achieving several hundred percent year-over-year growth in consecutive quarters. This segment generates the majority of the company’s revenues and is forecast to grow to over 56 billion USD by the end of 2026.

The gaming segment, while more volatile, is recovering from declines earlier in 2024 and continues to contribute significantly, with revenues projected at around 4 billion USD by the end of 2026. The automotive segment is also growing steadily, developing from just under 300 million USD to over 680 million USD, with fluctuations indicating rising interest and investments. Other areas, such as OEM and others, though smaller, also show solid growth and increasing importance for overall operations. Together, these trends demonstrate Nvidia’s effective revenue diversification, strengthening its leadership in digital transformation and AI.

Valuation overview

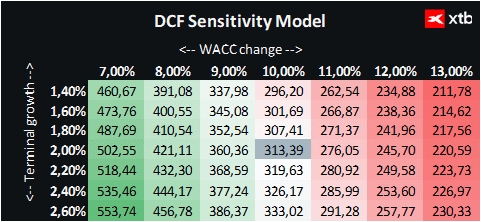

We analyze Nvidia’s valuation using the discounted cash flow (DCF) method. It is important to emphasize that this analysis is for informational purposes only and should not be considered investment advice or an exact stock price forecast.

Our projections assume an average annual revenue growth rate in the double digits, estimated at around 40 to 60 percent over the next few years. In subsequent years, the revenue growth rate will gradually decline due to market saturation and increasing competition.

The Blackwell GPU architecture is becoming a key element of Nvidia’s strategy for the coming years. The latest chips have received enormous interest, significantly exceeding the company’s initial expectations. Blackwell drives the global AI hardware boom thanks to its exceptional performance and its role in training and deploying the most advanced AI models. It is this architecture that helps Nvidia maintain a dominant position in the data center and latest chip segments, which fuel the company’s further dynamic growth.

Our valuation also incorporates a weighted average cost of capital (WACC) estimated at around 10%, reflecting current market conditions and the tech sector’s specifics. Nvidia has a moderate level of debt, which is managed effectively, so the cost of debt has a limited but meaningful impact on the overall capital cost. We assumed a terminal growth rate of 2%, with other parameters based on averages from the last five years.

Based on these assumptions, Nvidia’s valuation stands at approximately 313 USD per share, indicating a growth potential of about 78% compared to the current market price of around 175 USD. The current valuation may not fully reflect the company’s value and growth prospects. Nvidia faces the opportunity for further dynamic expansion driven by rising demand for cutting-edge AI, data center, and gaming solutions, as well as successive generations of the Blackwell architecture gaining global recognition.

BREAKING: US PMI beats expectations slightly; EURUSD with no reaction 📌

UK Budget preview

DE40: European tech and defence stocks sell-off

BREAKING: Mixed results for the UK PMI index. GBPUSD muted

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.