The May NFP report has triggered a rally in the US dollar of over 0.7% against the euro, alongside significant declines in the US stock market (with the NASDAQ dropping 1.7%). The state of the US labor market has turned out significantly better than expected. In the face of persistent inflationary pressures, this should prompt the Fed to hike interest rates. The pivotal question now is not "if," but "when" – and to what extent the new Fed Chair, Kevin Warsh, will attempt to push back against monetary policy tightening.

A few words on the data

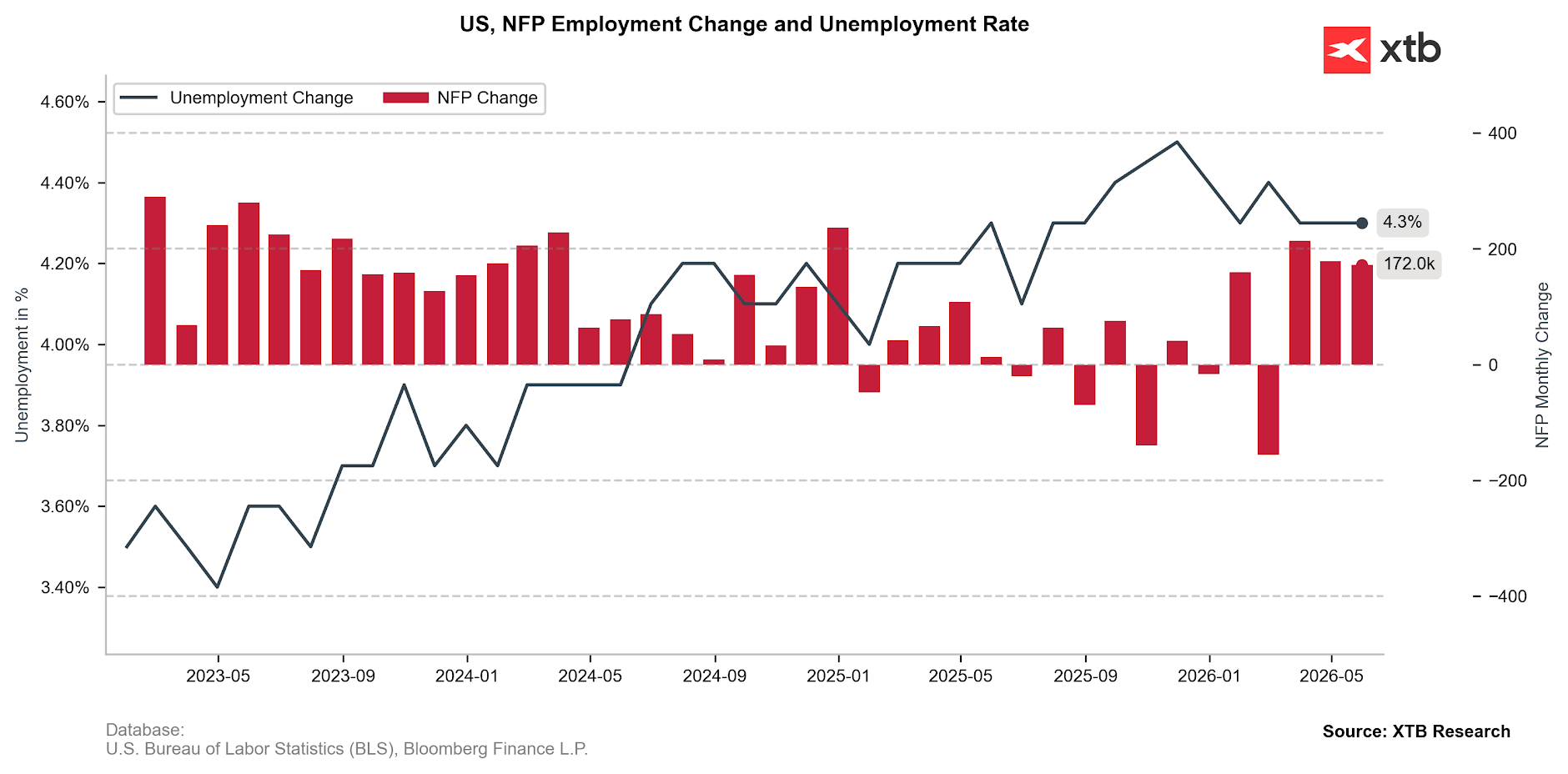

The number of non-farm payrolls in the US labor market increased by 172k. This figure not only beats the consensus estimate (86k) but vastly exceeds even the most optimistic forecasts (125k). To make matters worse for market bulls, data for the previous two months was revised upward by 93k. Given that the Bureau of Labor Statistics has accustomed us to substantial downward revisions, this comes as an exceptionally large surprise. Meanwhile, the unemployment rate remained unchanged at 4.3%.

Figure 1: Change in Non-Farm Payrolls (NFP) and the Unemployment Rate in the US (2023 - 2026)

Source: XTB Research, 05.06.2026

Source: XTB Research, 05.06.2026

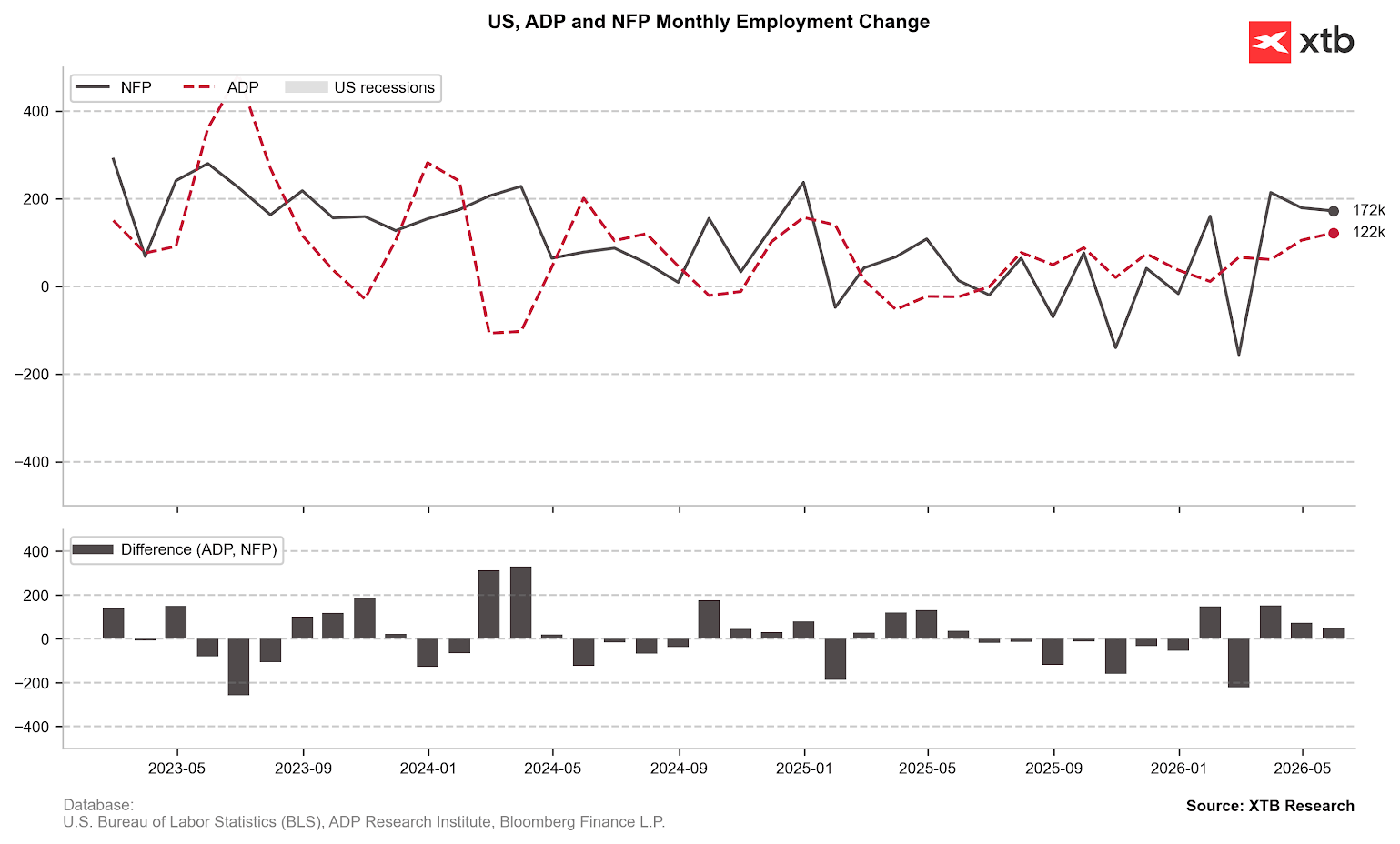

The report aligns perfectly with the broader picture painted by recent labor market data. Weekly jobless claims remained near multi-year lows, while ADP and JOLTS data both surprised to the upside – the latter particularly strongly, though it is worth noting that JOLTS data is significantly lagged compared to the rest. It is also consistent with the narrative from the latest FOMC minutes, where Fed analysts indicated that after a period of cooling, labor market conditions had "stabilized." Even then, for some policymakers, this served as an argument that the economy is not on the verge of a sudden slowdown and does not require the support of cheaper money.

Figure 2: NFP and ADP Data (2023 - 2026)

Source: XTB Research, 05.06.2026

Source: XTB Research, 05.06.2026

A 2026 rate hike fully priced in

On June 17, the FOMC will meet once again, this time chaired by its new leader. Kevin Warsh was supposed to represent the promise of long-awaited monetary easing for the markets. However, he takes over Jerome Powell's legacy at a time when discussions regarding rate cuts can be considered highly outdated.

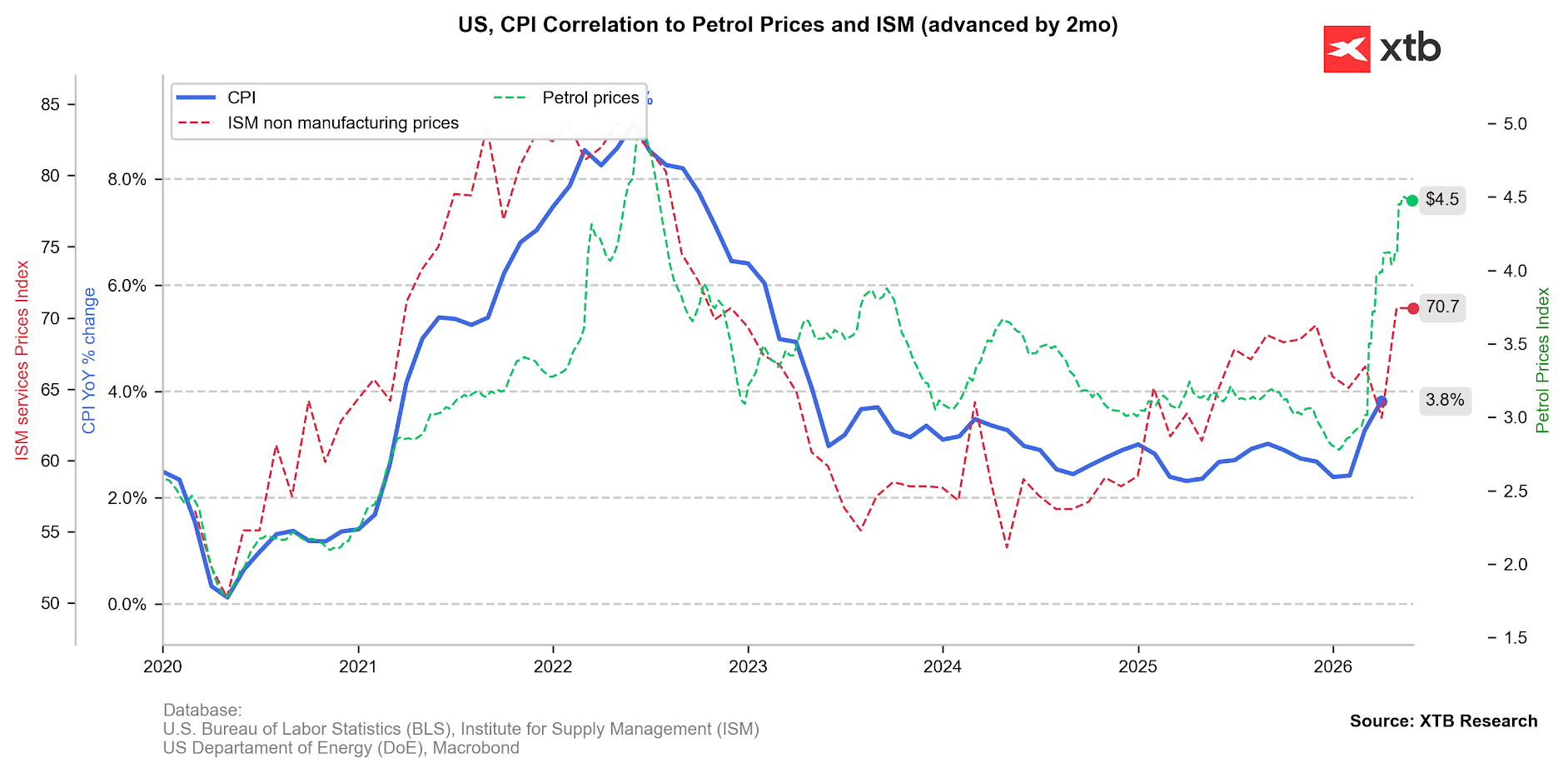

With labor market concerns fading significantly, the Fed will be able to focus almost entirely on the second part of its mandate: ensuring price stability. In light of the faster-than-expected transmission of higher energy commodity prices to other sectors of the economy, this is a critically important issue.

Figure 3: Headline CPI Inflation, ISM Services PMI Price Index, and US Gasoline Prices (2020 - 2026)

Source: XTB Research, 05.06.2026

Source: XTB Research, 05.06.2026

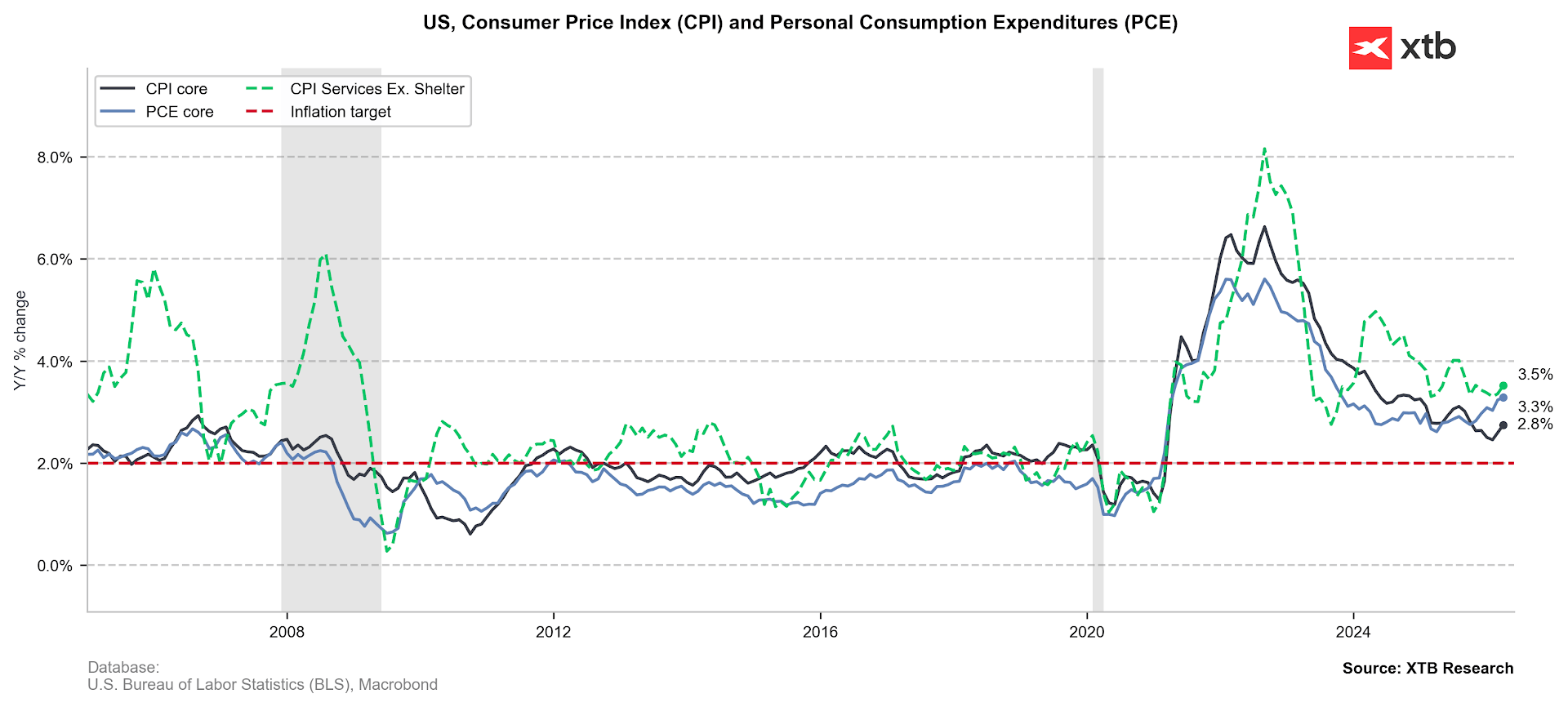

Headline CPI inflation rose to 3.8% in April. More concerning, however, is that core inflation measures have also moved significantly higher, both for CPI (2.8%) and PCE (3.3%) – the latter is published with a delay but is preferred by the Fed. At the same time, soft indicators point to further upward pressure on prices, including the price sub-index of the latest ISM PMI report, which hit a multi-year high of 70.7.

Figure 4: Core CPI and PCE Inflation in the US (2020 - 2026)

Source: XTB Research, 05.06.2026

Source: XTB Research, 05.06.2026

The dollar is well positioned

It appears that the labor market is finding its footing, and prolonged negotiations between the US and Iran (and the resulting prolonged disruption of the Strait of Hormuz) could hit US inflation harder than originally expected. Therefore, in the absence of de-escalation, the greenback should receive a three-pronged boost: from a more hawkish Fed, the US's position as a net exporter of energy commodities, and its safe-haven status, which attracts investors amidst global turmoil and should benefit from geopolitical instability.

Markets will be closely watching the divergence in rate hike pricing on both sides of the Atlantic – the US versus the Eurozone. Next week, the ECB will most likely make an upward move. Attention will center on President Lagarde’s remarks; given weak economic data and lower-than-expected inflation figures, she may temper the still rather aggressive expectations for further tightening.

Stock market under pressure

US bond yields are rising (10-year yields up by nearly 10 basis points), which is naturally unwelcome news for equity investors. There appears to be ample room for further upward revisions in rate hike expectations. If the market indeed moves in this direction, the stock market correction that many have been anticipating could easily materialize.

Key takeaway: In this context, it will also be crucial to see whether strong labor market data will call into question businesses' confidence regarding the scale of productivity growth brought by AI technology.

Since the improvement in the US labor market partly stems from job growth in the construction sector – which is enjoying a boom due to extensive data center construction – such conclusions might be somewhat premature. This issue is fundamental: excluding companies from the broader AI ecosystem, the S&P 500 is currently flat year-to-date. With them included, it is experiencing one of its most fruitful periods in decades.

—

Michał Jóźwiak, Financial Markets Analyst at XTB

3 markets to watch next week: US100, GOLD, EURUSD (05.06.2026)

Daily summary: Nasdaq 100 drops 3%, precious metals and Bitcoin are falling amid US dollar strength

Silver slumps 7% 📉 Precious metals under selling pressure

BREAKING 🚨 Nasdaq tumbles 2.4%, Bitcoin tests key $60K support

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.