- Netflix shares fall nearly 9% after earnings as investors fail to see convincing evidence of accelerating profitability

- The company beat earnings-per-share expectations, while revenue came in broadly in line with forecasts

- Netflix maintained its target of approximately $3 billion in advertising revenue for 2026 but disappointed investors with weaker-than-expected earnings guidance

- Netflix shares fall nearly 9% after earnings as investors fail to see convincing evidence of accelerating profitability

- The company beat earnings-per-share expectations, while revenue came in broadly in line with forecasts

- Netflix maintained its target of approximately $3 billion in advertising revenue for 2026 but disappointed investors with weaker-than-expected earnings guidance

Netflix reported second-quarter 2026 results that were broadly in line with Wall Street expectations, but investors were disappointed by the company's outlook for the coming months. The streaming giant issued weaker-than-expected third-quarter revenue and earnings guidance, sending its shares down more than 9% in after-hours trading.

Netflix results: Very strong, but not strong enough

Netflix maintained its full-year guidance while continuing to expand its advertising business, live programming and artificial intelligence initiatives, arguing that it remains in the early stages of monetizing its global user base.

However, after years of rapid expansion, investors are increasingly looking for new growth catalysts. Importantly, the latest earnings report does not point to any deterioration in Netflix's underlying fundamentals.

- Despite the somewhat conservative guidance, one metric that should reassure investors is improving engagement. Total viewing hours increased by 2% year over year during the first half of 2026, compared with 1.5% growth a year earlier, suggesting that audience engagement with Netflix's content remains healthy.

- Revenue continues to grow at a double-digit pace, net income is increasing, and advertising remains one of the company's fastest-growing businesses. Yet the market reaction highlights just how demanding investors have become. Even after the stock's sharp decline, Netflix trades at roughly 21x forward earnings - its first discount to the average S&P 500 forward P/E since 2022. Investors appear to be looking for exceptional results that would justify valuation multiples typically reserved for high-growth companies.

- That would require much stronger evidence of accelerating growth, and this quarter failed to deliver it. Slightly weaker-than-expected revenue and EPS guidance, combined with Netflix's decision to reduce the frequency of viewership disclosures, reinforced concerns that the company is entering a more mature phase of its development, where sustaining its historical growth trajectory may become increasingly difficult.

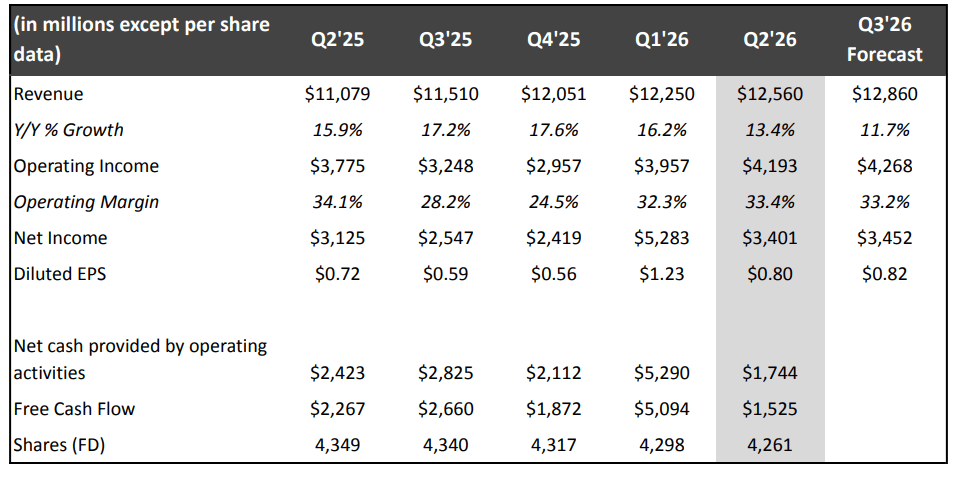

Overall, Netflix generated $12.6 billion in revenue during the second quarter, in line with its own guidance and up 13% year over year, or 12% on a foreign exchange-neutral basis. Growth was driven primarily by higher membership, subscription price increases and rising advertising revenue. Revenue increased at a double-digit pace across every region, with quarterly sales surpassing $4 billion in EMEA for the first time and exceeding $1.5 billion in both Latin America and the Asia-Pacific region.

In the US and Canada, revenue rose 10%, reflecting only a partial-quarter impact from recent price increases, which management said have performed in line with expectations. The company also expects content amortization growth to slow during the second half of the year, with full-year growth of approximately 10%. Diluted EPS increased 11% to $0.80 from $0.72 a year earlier, slightly exceeding the company's internal forecast.

Key takeaways from Netflix's earnings

- Revenue increased 13% year over year to $12.56 billion, broadly in line with analyst expectations.

- Earnings per share came in at $0.80, compared with the consensus estimate of $0.79.

- Net income rose to $3.40 billion from $3.13 billion a year earlier.

- Netflix expects third-quarter revenue of $12.86 billion and EPS of $0.82, below Wall Street expectations of $13.0 billion and $0.84, respectively.

- The company maintained its target of generating approximately $3 billion in advertising revenue during 2026.

- Total viewing time exceeded 97 billion hours during the first half of the year.

- Beginning in 2027, Netflix will publish its "What We Watched" report only once a year, shifting investor focus toward financial performance.

Source: Netflix Quarterly Earnings

Third-quarter and full-year guidance

Netflix expects third-quarter revenue of $12.86 billion and diluted earnings per share of $0.82, compared with Wall Street consensus estimates of approximately $13.0 billion and $0.84, respectively. Revenue is expected to increase 12% year over year, or 11% on a foreign exchange-neutral basis, driven by continued membership growth, subscription price increases and higher advertising revenue. The company also expects its operating margin to improve to 33.2%, up from 28.2% a year earlier, indicating further profitability gains despite slightly softer-than-expected revenue growth.

For the full year, Netflix narrowed its revenue guidance to $51.0-51.4 billion from the previous range of $50.7-51.7 billion, implying annual growth of 13-14%, or roughly 12% excluding currency effects. The company reaffirmed its expectation that advertising revenue will roughly double to approximately $3 billion in 2026 and forecast a full-year operating margin of 31.5%, up from 29.5% in 2025.

Management also expects operating income to grow by more than 20% this year, outpacing revenue growth. The market's disappointment therefore stems less from any deterioration in Netflix's long-term outlook and more from the fact that third-quarter guidance failed to meet Wall Street's elevated expectations. Netflix continues to improve profitability, but as the business matures, it has less room for execution missteps.

Second-quarter results remain solid

Netflix's revenue increased 13% year over year to $12.56 billion. The company said growth was driven primarily by continued expansion of its paying membership base, earlier subscription price increases and the rapidly growing advertising segment.

Net income rose to $3.40 billion from $3.13 billion a year earlier, while earnings per share increased to $0.80 from $0.72.

Netflix also emphasized that the subscription price increases introduced earlier this year have performed in line with expectations and have not materially affected customer demand.

Advertising remains a key growth driver

Expanding the advertising business remains one of Netflix's most important strategic priorities.

The company continues to expect advertising revenue to reach approximately $3 billion in 2026, representing nearly a doubling from the previous year. Management also highlighted strong advertiser demand for live sports and live events, including NFL and MLB games, WWE programming and the FIFA Women's World Cup.

During the earnings call, executives acknowledged that they continue to evaluate the possibility of launching a free ad-supported tier in selected markets. However, they stressed that no near-term launch is planned because such a model requires a sufficiently scaled advertising business while minimizing the risk of cannibalizing paid subscriptions.

Netflix reduces viewership disclosures

One of the most closely watched announcements was Netflix's decision to change how it reports engagement metrics.

Beginning in 2027, the company's "What We Watched" report, which provides detailed viewing-hour data for individual titles, will be published once a year instead of twice annually.

Management said the goal is to keep investor attention focused primarily on financial metrics such as revenue and operating profit.

The move is consistent with Netflix's broader communication strategy. The company stopped reporting quarterly subscriber numbers in 2025 and is increasingly emphasizing profitability and monetization rather than headline subscriber growth.

Management seeks to ease engagement concerns

Wall Street has become increasingly focused on engagement trends, particularly after reports suggesting weaker viewership for second seasons of some series.

Netflix said viewers watched more than 97 billion hours of content during the first half of 2026, representing 2% growth compared with 1.5% a year earlier.

Co-CEO Greg Peters emphasized that viewing hours alone are not directly linked to financial performance. According to management, live programming generates fewer viewing hours than traditional series but is significantly more effective at attracting new subscribers and advertisers. Although live events account for roughly 1% of viewing hours, they represent more than 5% of Netflix's content budget because their primary purpose is to strengthen the overall value of the platform.

Netflix also highlighted the broader adoption of generative artificial intelligence across its production workflow. During the first half of 2026, GenAI tools were used in approximately 300 productions, primarily during post-production. The technology helps create expensive crowd scenes, visual effects and large-scale world-building shots, while Ted Sarandos emphasized that AI is intended to enhance creators' capabilities rather than replace them.

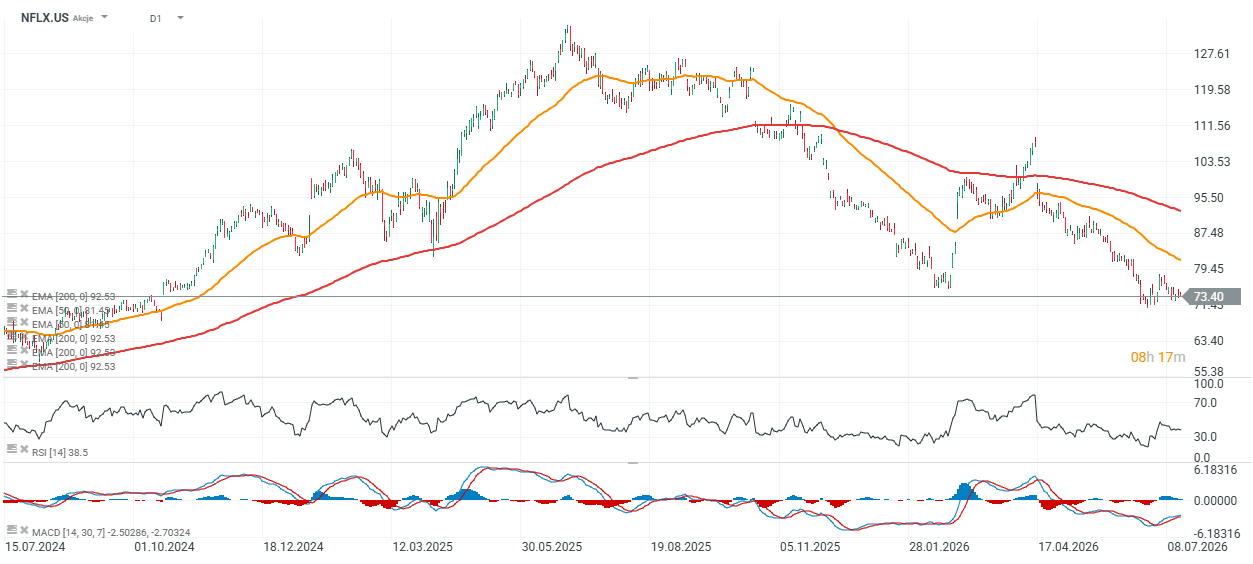

Netflix share price chart (D1 timeframe)

Following the earnings release, Netflix shares fell to approximately $67 in after-hours trading and are now trading around 30% below the 200-day EMA (red line), indicating a medium-term downtrend. The 50-day EMA near $81 currently represents the key resistance level, while the RSI stood at a near-neutral reading of 41 at yesterday's close. If Netflix begins raising guidance and demonstrates stronger growth in its advertising business, investors could become more constructive on both the stock and its valuation.

Source: xStation5

The chart suggests that despite an almost 42% decline in the share price over the past 12 months, Netflix's fundamentals remain relatively resilient. Over the past eight quarters, the company increased revenue by an average of 3.6% quarter over quarter, EBIT by 6.2% and earnings per share by 9.9%, indicating that profitability has been expanding faster than sales.

Meanwhile, the decline in the share price has reduced Netflix's forward P/E ratio to approximately 21, well below its historical average. The current valuation reflects considerably more investor pessimism than the underlying financial performance would suggest. Investors appear to view the weaker-than-expected guidance as evidence that more conservative valuation multiples are justified at Netflix's current stage of development.

Source: XTB Research

Netflix slumps, as SpaceX and chip stock sell off continues

Market Wrap: European indices decline amid US - Iran tensions📉 Semiconductors under pressure

Morninga Wrap: Wall Street Under Pressure. AI Loses Momentum, Netflix Disappoints, and the Persian Gulf Erupts

Daily Summary: 📉 A Red Day Across Markets. AI Sector Weighs on Wall Street, Precious Metals Under Pressure

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.