We are starting a new week on the financial markets.

Today's session will be unique because, due to bank holidays in China, the US and Canada, there will be no session on the cash markets, which may significantly reduce the volatility observed in many markets.

Interestingly, the break in China will last until the end of the week, due to the Lunar New Year celebrations.

For this reason, volatility on Asian markets was very low today. At present, Japan's Nikkei is up 0.02%, while India's Nifty 50 is up 0.2%.

This week, the dollar will remain in the spotlight, and the market will play along with the narrative of "USD rebalancing", with Credit Agricole expecting consolidation rather than major movements, unless there is clearly weaker data or dovish signals from the Fed. Key publications will include: December core PCE, preliminary PMI for February, FOMC meeting minutes and the December TIC report, which will show whether foreign demand for US bonds and equities has begun to weaken. An additional, non-calendar source of volatility could be the potential US Supreme Court ruling on tariffs, scheduled for 20 February. All these factors mean that the end of the week could bring increased volatility for the USD and Treasury yields, especially if the data and decisions deviate from the consensus.

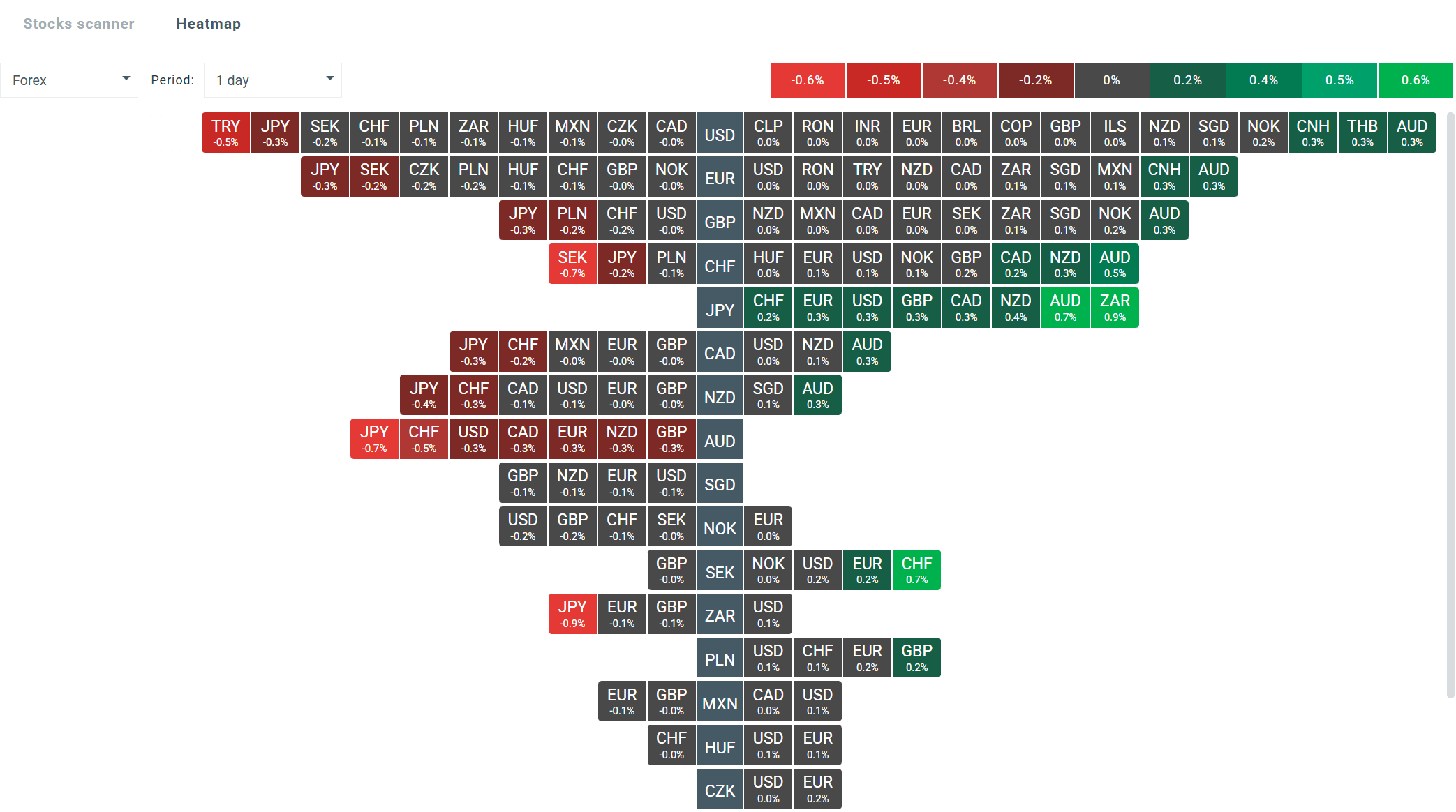

Today, however, the Australian dollar is performing best on the Forex market. Increased declines are being observed in the Japanese yen.

The yen weakened after the data was released, as GDP growth of only 0.2% annualised (0.1% month-on-month) clearly fell short of expectations, confirming the fragility of the recovery and the weakness of exports and investment. This combination – soft growth with still elevated inflation – on the one hand does not give the Bank of Japan the comfort to tighten aggressively, and on the other hand reinforces the narrative that policy will remain unchanged for longer, which the market interprets as negative for the yen. In addition, today's meeting between Prime Minister Takaichi and Governor Ueda raises concerns that the government will push for caution in normalisation, which also weighs on the currency.

The service sector in New Zealand continues to grow (PSI 50.9 – business sentiment index), but momentum is slowing, with employment and inventories contracting, indicating caution among companies and dampening optimism for the NZD. The 1.1% m/m decline in spending measured by payment card transactions in January, despite a slight y/y increase, confirms the seasonal weakness in consumption after the holidays, limiting expectations for interest rate cuts and supporting a slight stabilisation of the economy.

Both SILVER, which is down 1.2%, and GOLD, which is down 0.83%, are performing poorly on the metals market.

However, the biggest declines are seen in NATGAS, where investors are once again reacting to higher than average temperatures in the 8-14 day forecast. Prices for this commodity have already fallen by nearly 7%.

Bitcoin loses 1% and is trading close to £68,000.

Heatmap of volatility on the FX market at present. Source: xStation

Bank Holiday in USA and Wall Street is closed 🏛️

Crypto news: Will Bitcoin drop again? 🔍 Cryptocurrencies try to stabilize after the sell-off

The Week Ahead

Economic and corporate calendar: Bank holiday in China, the US, and Canada 💡(February 16, 2026)

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.