Around midday, sentiment in global equity markets is moderately positive. There are signs of a tentative return to risk assets: the VIX volatility index has pulled back nearly 10% from its recent local peak, while Nasdaq 100 (US100) futures are up around 0.5%, with Bitcoin breaking above the $70,000 level. Gains are also visible in the precious metals market, where silver is jumping about 5% after yesterday’s decline.

- Investors are awaiting ADP employment data from the US private sector as well as the final ISM services reading. In Europe, PPI inflation declined less than expected (-2.1% y/y versus -2.6% forecast), while the unemployment rate came in at 6.1% compared with expectations of 6.2%. Final German PMI data were slightly higher than the preliminary readings and relatively strong (53.2 for the Composite index and nearly 52 for services). The Eurozone PMI also exceeded expectations.

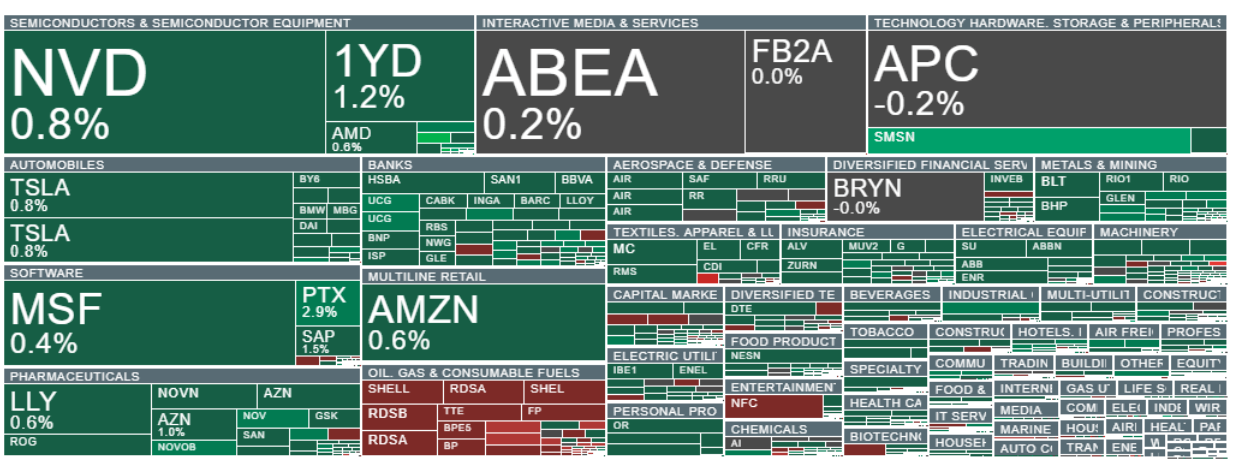

- The European session is currently dominated by buyers. Futures on the German DAX are rising, while the Euro Stoxx 50 gains nearly 1.8%. Losses are being recovered across sectors such as banks, mining companies and automakers. Meanwhile, Samsung ADRs are rebounding nearly 7% after the panic-driven selloff on the Korean market, during which trading in the KOSPI index was halted after it plunged more than 10%.

- Oil (OIL) is pulling back from around $85 to $82 per barrel, while Henry Hub US natural gas futures have dropped more than 5% from their recent local highs. Financial media reported that Iranian authorities may have begun negotiations with the US CIA, although Israeli IDF officials stated that bombing of targets in Iran will continue for at least two more weeks. At the same time, Turkey intercepted an Iranian missile that entered NATO airspace.

- Part of the stabilization in sentiment followed remarks by Donald Trump, who assured markets that energy flows and commercial trade through the Persian Gulf would remain uninterrupted. However, oil prices are again rising about 3% today, suggesting that a geopolitical risk premium remains embedded in commodity prices.

Analyst commentary

-

Kion: Jefferies upgraded the stock to “hold”, citing more limited downside risks from current levels.

-

European banks: Morgan Stanley notes that the sector could remain under short-term pressure if the Middle East conflict persists.

-

Thales: JPMorgan downgraded the stock to neutral, citing weaker prospects for the cyber & digital division despite the company’s strong defense business.

-

EuroAPI: guidance for 2026 implies a roughly 29% downgrade to consensus core EBITDA expectations.

-

ASM International: the Dutch semiconductor equipment maker issued stronger-than-expected guidance for Q1 2026 and expects even stronger revenue in the second half of the year. Shares are up about 6% in pre-market trading.

Key corporate news

-

Siemens Energy plans a share buyback program of up to €2 billion.

-

EQT announced a new share repurchase program.

-

Quilter announced a £100 million buyback.

-

Bayer forecasts 2026 EBITDA of €9.6–10.1 billion.

-

Adidas expects 2026 operating profit of around €2.3 billion, below the market consensus.

-

Continental forecasts an adjusted EBIT margin of roughly 11–12.5% in 2026.

-

Traton expects an adjusted operating margin of 5.3–7.3%.

-

Symrise forecasts organic sales growth of 2–4%.

-

Redcare Pharmacy reported a significant year-over-year improvement in EBITDA.

-

NKT signed a €2.2 billion contract for the UK’s Eastern Green Link 3 energy project.

-

BAE Systems secured a seven-year A$163 million contract with the Australian government.

-

Capita won a £370 million outsourcing contract.

-

Maersk introduced an additional freight fee for container shipments to the Middle East.

Market implications

Global markets remain highly sensitive to geopolitical developments. The sharp selloff in Asia increases the risk of renewed volatility in Europe, while energy prices and developments in the Middle East conflict remain the key drivers of investor sentiment. At the same time, select positive corporate developments are emerging, particularly in the semiconductor and energy sectors.

Analyst recommendation changes

Upgrades

-

AMG: upgraded to buy at Deutsche Bank; target price €42.

-

Clas Ohlson: upgraded to hold at SEB Equities; target price SEK 360.

-

Danone: upgraded to outperform at BNP Paribas; target price €83.

-

Emeis: upgraded to reduce at AlphaValue/Baader.

-

Kion: upgraded to hold at Jefferies; target price €56.

-

Nexans: upgraded to overweight at Barclays; target price €157.

Downgrades

-

BW LPG: downgraded to hold at ABG; target price NOK 191.

-

BW LPG: downgraded to hold at Arctic Securities; target price NOK 185.

-

Dassault Systèmes: downgraded to neutral at Goldman Sachs; target price €20.

-

Eezy: downgraded to reduce at Inderes; target price €0.60.

-

Equinor: downgraded to hold at ABG; target price NOK 300.

-

Kuehne + Nagel: downgraded to reduce at HSBC; target price CHF 160.

-

PhotoCure: downgraded to hold at ABG; target price NOK 72.

-

Segro: downgraded to neutral at UBS; target price 840 pence.

-

Syensqo: downgraded to neutral at UBS; target price €54.

-

Thales: downgraded to neutral at JPMorgan; target price €275.

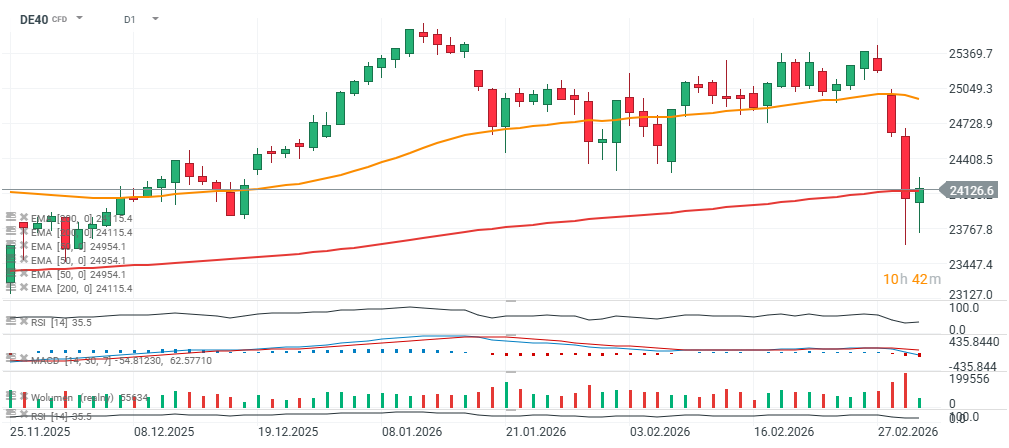

DE40 (D1 timeframe)

The German DAX futures contract (DE40) has moved back above the 200-session exponential moving average (EMA200). The chart shows a long lower wick, signaling that buyers remain active despite the prevailing broader downtrend.

Source: xStation5

Source: xStation5

Navigating Middle East uncertainty and tariff risks

US Raises Tariffs to 15%

VIX struggle to rise higher despite uncertainty on Wall Street 🔎

Trump’s plan for Strait of Hormuz fails to stop gains in oil price, as investors pause European sell off

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.