📈 Markets (Indices, FX, Commodities)

-

Eurozone futures rebound as regional divergence widens: Broad European index futures post a mixed recovery, led firmly by the Euro Stoxx 50 (EU50: +0.82%), alongside solid gains in France (FRA40: +0.63%) and Germany (DE40: +0.52%). Meanwhile, regional laggards weigh heavily on the periphery, with Spain's IBEX 35 (SPA35: -0.66%) and Poland's WIG20 (W20: -1.30%) falling deepest into the red.

-

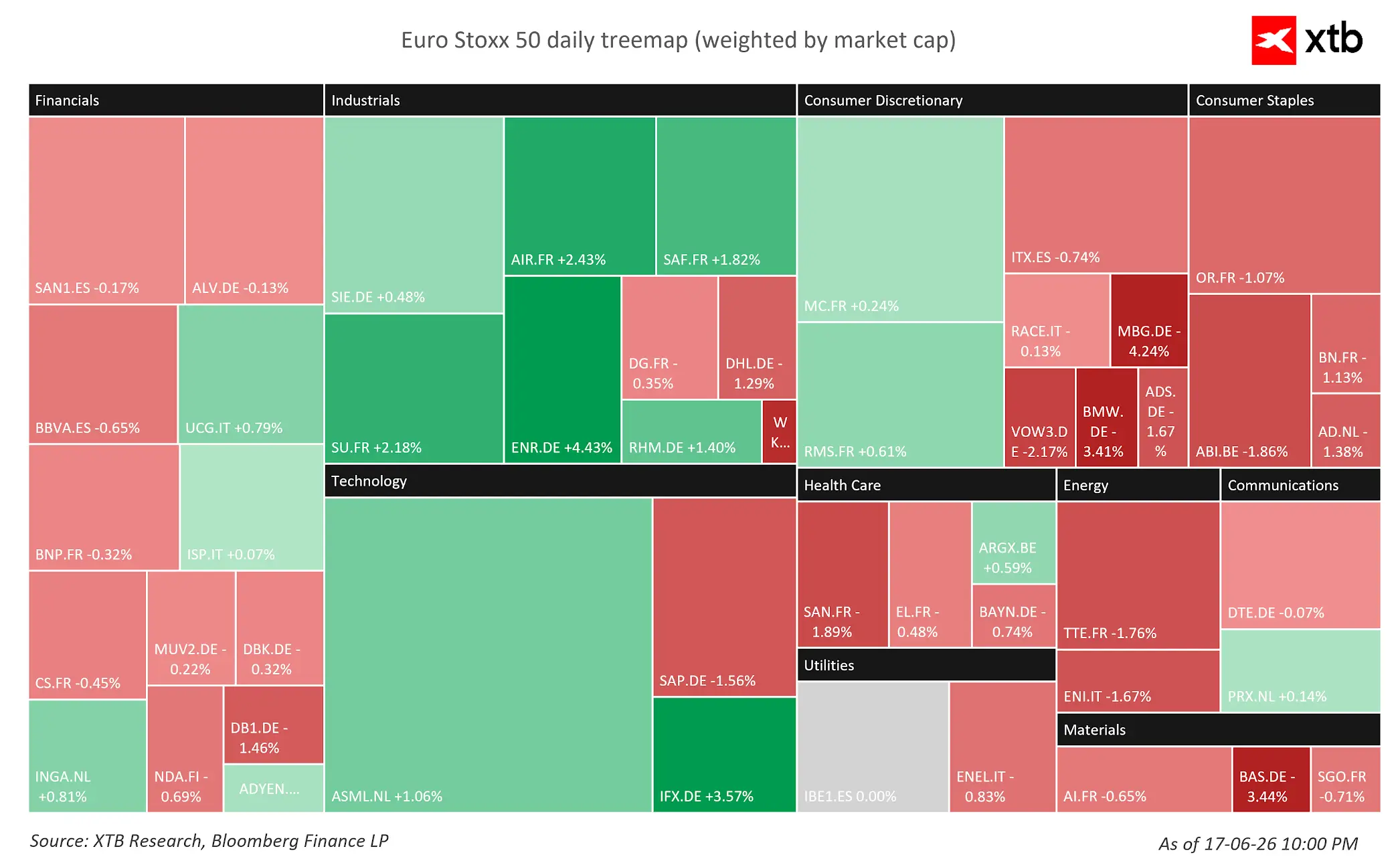

Euro Stoxx 50 splits on sharp sector divergence: European markets are highly fragmented. Industrials and Technology lead the green block, driven by strong gains from Airbus (AIR.FR: +2.43%), Schneider Electric (SU.FR: +2.18%), and chipmaker Infineon (IFX.DE: +3.57%). Conversely, severe selling pressure weighs down Consumer Discretionary and Materials, dragged lower by heavy bleeding in the automotive camp and chemical giant BASF (BAS.DE: -3.29%).

-

FX — Dollar surges on hawkish FOMC pivot: The U.S. dollar index surged (USDIDX: +0.3%) to its highest level since May 2025 following yesterday's unexpectedly hawkish Fed dot plot and Donald Trump's "green light" on potential rate hikes. Scandinavian currencies (USDSEK, USDNOK: +1.0%) and the Swiss franc (USDCHF: +0.7%) are the weakest performers today. The pound extended losses following the BoE hold (GBPUSD: -0.5%), while EURUSD dropped 0.35% to 1.1460.

-

Energy — Crude steady as natural gas gains: Crude oil slightly extended its recent losses, with Brent futures (OIL) dropping 0.35% to $74.70 per barrel as geopolitical premiums ease. Conversely, natural gas (NATGAS) futures added 1.4%.

-

Precious Metals — Dollar strength hammers gold and silver: Precious metals are trading in the red, facing severe headwinds from rising real yields and a dominant greenback. Gold (GOLD) fell 0.3% to $4,244/oz, while silver (SILVER) plummeted 1.5% to $66.91/oz.

USDIDX (weekly interval) trades at at highest since May 2025, supported by a hawkish dotplot from Fed, with almost half of the policymakers seeing a rate hike before the end of 2026. Dollar strength exercises a downward pressure on GOLD (yellow, inverted). Source: xStation5

🏢 Company News

-

Airbus defies macro downturn on Kepler upgrade: Airbus (AIR.FR) shares rose 2.8% to €192.24 after Kepler Cheuvreux upgraded the stock to Buy (PT €212). Analysts noted that easing geopolitical tensions and lower fuel costs will boost aerospace, while long-term sentiment was reinforced by Qantas utilizing its A350s for ultra-long-haul routes and a $1.4B KKR aircraft leasing injection.

-

Auto stocks keep plunging on BMW’s warning: A shock profit warning from BMW (BMW.DE: -4.23% to €59.61) citing a collapsing Chinese market continues to hammer the automotive sector. Direct contagion dragged down Mercedes-Benz Group (MBG.DE: -4.56% to €44.62) and Stellantis NV (STLAM.IT: -3.65% to €5.57), while Volkswagen (VOW3.DE: -2.45% to €84.42) fell as its virtual AGM failed to calm investors.

-

Carrefour tumbles on JPMorgan warning: Carrefour (CA.FR) shares plunged 6.5% to €15.38 after JPMorgan placed the French grocer on its Negative Catalyst Watch ahead of July earnings, maintaining a Sell rating. Wall Street analysts cite potential H1 profit downgrades, stiff domestic competition, and a broad global market risk-off mood as primary drivers.

-

Edenred shares surge on buyout rumors: Shares of the French employee benefits provider surged over 16% to €24.07 in Paris following reports that UK private equity firm BC Partners is exploring a takeover bid. Analysts note Edenred's strong cash flow and low debt make it highly attractive despite regulatory risks, suggesting an opportunistic valuation.

-

L'Oreal deepens India bet with Innovist buyout: French beauty giant L'Oreal (OR.FR) has agreed to acquire a majority stake in Innovist, the digital-first parent company behind popular science-led Indian brands Bare Anatomy and Chemist at Play. Innovist will join L'Oreal’s Consumer Products Division, giving the multinational direct access to India's high-growth $20B beauty market.

-

Tesco slides on soft Q1 UK sales: Shares in Tesco Plc (TSCO.UK) fell over 2.5% to 445.00p after reporting a weaker-than-expected 1.8% UK like-for-like sales growth. Easing food inflation and poor weather hit its wholesale unit, Booker (-3.2%). However, management maintained its FY26/27 operating profit guidance of £3.0B–£3.3B, backed by robust Irish sales (+3.3%) and surging online demand (+17.4%).

Today's volatility in Stoxx 50 (EU50) sectors. Source: XTB Research

🌍 Economics & Politics

-

U.S. and Iran sign historic preliminary peace deal: U.S. President Donald Trump and Iranian President Pezeshkian signed a 14-point MoU, halting military operations and establishing a 60-day window to negotiate a final deal. Iran will allow immediate, toll-free commercial vessel transit through the Strait of Hormuz for 60 days in exchange for immediate U.S. Treasury sanction waivers on oil exports.

-

BoE holds Bank Rate at 3.75% amidst Middle East volatility: The Bank of England's MPC voted 7–2 to maintain interest rates at 3.75%, with two hawkish dissenters pushing for a 25 bps hike. While headline CPI fell to 2.8%, the Committee warned inflation will likely rise later this year due to volatile energy markets and potential second-round wage-setting effects.

-

SNB holds policy rate at 0% with slight inflation upgrade: The Swiss National Bank maintained its quarterly interest rate at 0.0%, marking a full year of unchanged policy. Despite a Middle East energy shock lifting May CPI to 0.6%, inflation remains comfortably within the 0–2% target. The SNB slightly lifted its inflation forecasts to 0.6% for 2026/2027 and 0.7% for 2028, while keeping GDP growth estimates steady at 1.0% for 2026.

-

Schlegel vows FX intervention to fight Franc strength: SNB Chairman Martin Schlegel shrugged off second-round inflationary effects but expressed heightened readiness to intervene in the foreign exchange market to curb rapid Swiss franc appreciation. Board members noted that domestic recovery remains solid, shielded by hydro and nuclear power insulation from energy shocks, though fragile global growth and Middle East tensions persist as key external risks.

-

Norges Bank delivers hawkish hold at 4.25%: Norway's central bank kept its policy rate unchanged at 4.25%, but firmed up explicit guidance for another rate hike at an upcoming meeting. The updated policy path was revised upward, now projecting a peak rate of 4.55% by year-end (up from 4.35% in March) to rein in persistent inflation.

Amazon Eyes External Sales of Custom AI Chips, Threatening Nvidia’s Dominance

US100 rallies 2.7% before the weekend 🚀

NATGAS spikes following EIA report 📈 Inventories decelerate

Stock of the Week: KLA Corporation and the Economics of Error in the Age of Artificial Intelligence

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.