Metal prices have quickly returned to gains after a historic crash, with “dip buyers” stepping back into the market. Gold is up 5% to $4,950 per ounce, while silver is rebounding 8% to $88 per ounce, recouping part of the steepest selloff since 2013.

- Recall that in January, precious metals surged on a wave of speculation, geopolitical tensions and concerns over the Federal Reserve’s independence. That rally was cut short brutally at the end of last week. Today, the rebound is being fueled by still-large and rising positions held by Chinese funds and Western retail investors, a renewed wave of call-option activity, and fresh inflows into leveraged ETFs.

- Metals are also benefiting from a “risk-on” tone across markets and a U.S. dollar that is stabilizing after its recent rise. At the same time, Chinese state-owned banks are reportedly trying to curb volatility in precious metals — so far with limited effect. UBS said the correction could be “healthy” in the long run and offers investors an opportunity to build positions at more attractive levels.

- Some banks still expect the uptrend to resume: Deutsche Bank reiterated its forecast for gold to reach as high as $6,000 per ounce. The bank argues that history more often points to short-term catalysts, and that investor intentions and sentiment toward precious metals have not structurally deteriorated despite the sharp drop. Deutsche Bank also noted that the selloff was larger than the underlying triggers would suggest, and that speculation alone does not fully explain the violence of the move. Deutsche Bank and Barclays both maintain that gold’s fundamentals remain strong: geopolitics, policy uncertainty and reserve-diversification themes may continue to support demand.

- Silver remains more “twitchy” than gold because it is a smaller market — which typically means higher volatility and a larger share of retail participation. Current forecasts see global silver demand rising sharply by 2030 (to 48,000–54,000 tonnes per year), while supply is projected to increase only to around 34,000 tonnes, implying a potentially widening supply gap. Solar photovoltaics alone could consume 10,000–14,000 tonnes annually (up to roughly 41% of global supply). That underscores that the longer-term bullish fundamentals are still in play.

- A key question now is how strongly Chinese investors will drive the Shanghai market, especially ahead of the Lunar New Year, with reports of increased jewelry and bullion purchases in Shenzhen. Markets are also watching geopolitics: rising U.S.–Iran tensions and talk of possible negotiations on a new nuclear deal — any breakthrough could reduce safe-haven demand and weigh on gold.

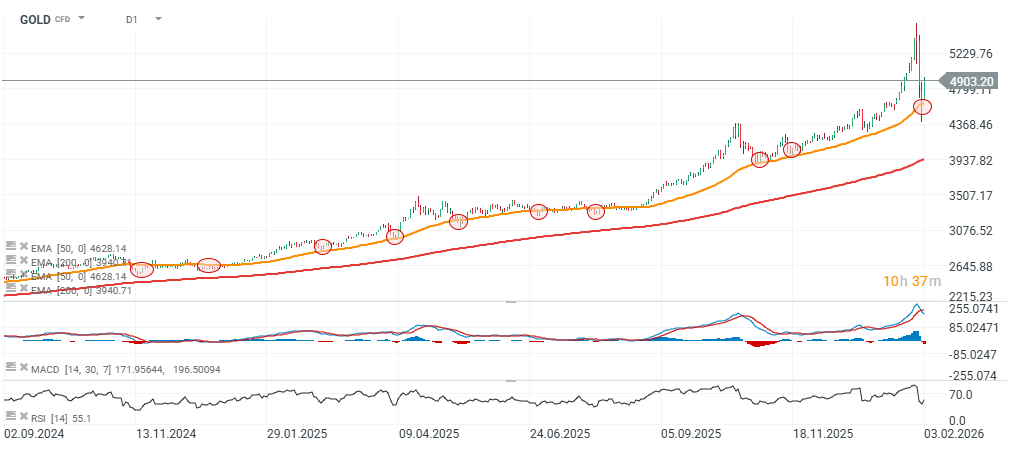

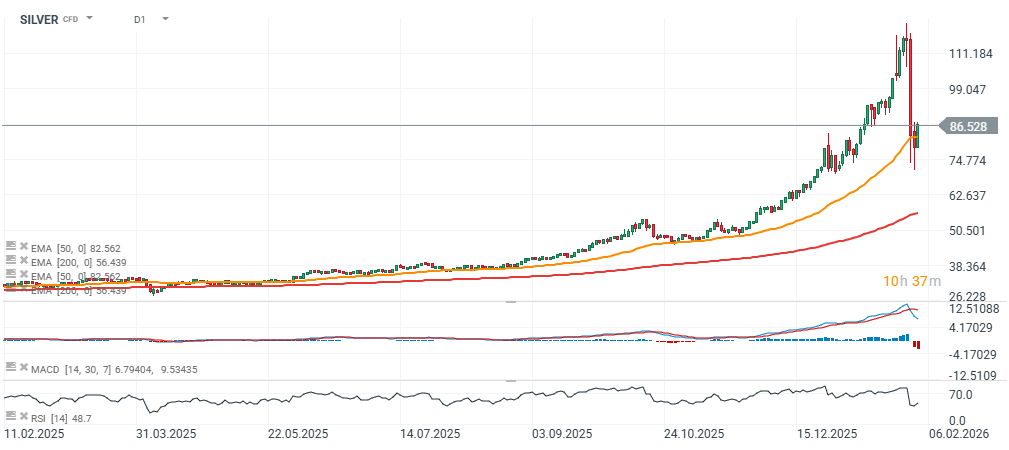

GOLD and SILVER (D1 timeframe)

Gold rebounded quickly after dipping below the 50-day EMA on the daily chart. Since the start of 2025, the 50-day EMA has repeatedly acted as strong trend support.

Source: xStation5

Silver has also rebounded after a drop below the 50-day EMA (similar in magnitude to March 2025). However, RSI has not yet managed to climb back above 50 following the latest sharp decline.

Source: xStation5

Riding gold and silver’s recovery, mining stocks and related funds are also advancing: in Europe, the Stoxx 600 Basic Resources index is up more than 2%. In London, shares such as Rio Tinto, Anglo American, Antofagasta and Fresnillo are higher. In the U.S., silver ETFs have rebounded sharply. Also, silver-focused miners are gaining including shares of Endeavour Silver, Coeur Mining, Hecla Mining and First Majestic Silver.

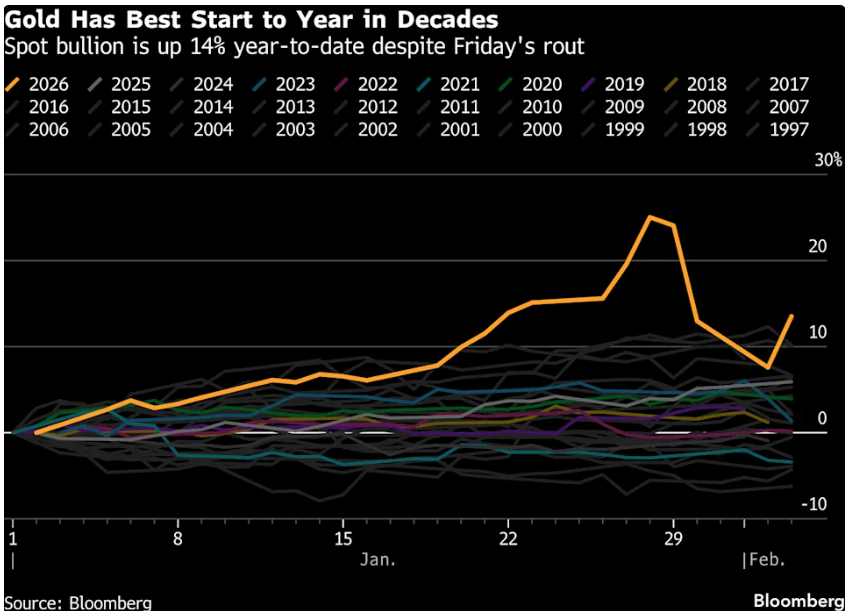

Gold is posting its strongest start to the year in decades — even after Friday’s panic selloff. Source: Bloomberg Finance L.P.

Three markets to watch next week (27.02.2026)

Daily summary: The beginning of the end of disinflation?

Wheat at its highest level in 8 months 📈

Jane Street: Legendary market maker in the court

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.