Risk sentiment is fading this morning; stocks are in the red and the Brent crude oil price is oscillating between $101 and $104 per barrel. The Iran war is not over, and the Strait of Hormuz remains closed, although the war appears to have entered a new stage. This is still a fluid situation, and markets will remain sensitive to headline risks.

The economic effects of the war are also coming to light this morning. Global PMI reports for March have been released, and they are reminding us of the wide-ranging economic risks generated by this conflict.

UK economy already showing signs of weakness caused by the war

The UK PMI for March was weaker than expected, the composite PMI fell sharply to 51.0 from 53.7 in February. Interestingly, the manufacturing survey was stronger than expected at 51.4, vs. expectations for a reading of 50. The service sector PMI reading was 51.2, weaker than the 52.9 that was expected.

The details were also worrying, input prices jumped to their highest level in 3 years, which shows how fast the conflict in the Middle East is impacting the UK economy. Business expectations for the year ahead fell sharply, there was a rapid rise in cost pressures across the private sector and the seasonally adjusted input cost index for the survey rose by a whopping 14 points between February and March, the largest monthly acceleration of input cost inflation since 1992.

Inflation pressures already building

The March PMI reading saw a decline in new work received for the first time in 4 months, and respondents noted cautious consumer spending patterns since the onset of the war. Business expectations for the year ahead fell to their lowest level in 9 months, and manufacturers also increased their output costs, which will likely add to upward pressure on the UK’s March CPI report.

The details of the UK’s PMI report were weaker than the headline figures suggest, and, for now, the headline figures remain in expansionary territory. However, the details suggest that the economic effects from the war are already starting to impact the UK economy, and inflation pressure along with weaker growth will weigh heavily on the UK economy as we move into Q2.

Donald Trump needs to show more progress on peace talks to boost market sentiment

The pound is at the weakest level of the day on the back of this data, and GBP/USD is back below $1.34, however the pound is not alone, and the USD is strengthening on a broad basis on Tuesday after Monday’s retreat, as risk aversion creeps back into the market. Although UK bond yields are stable this morning, it will take more conciliatory remarks from Donald Trump to extend Monday’s recovery rally and give hope that the war is close to wrapping up. Today’s PMI data is a sign that the longer this conflict goes on, the worse the economic outcomes will be for the global economy.

Eurozone PMIs also point to economic pain

European stocks have given up earlier gains after a raft of economic data soured the mood. Eurozone PMI readings for March suggest that corporates are struggling under the weight of higher input costs.

The French composite PMI fell deeper into contraction territory this month, the German composite PMI reading remains in expansionary territory, but it was sharply lower at 51.9 vs. 53.2 in February. This conflict in the Middle East hit just as European economies were starting to show green shoots at the macro level. The risk is that the PMI data, which is a lead indicator, is the start of a wave of weaker economic data to come down the line.

Service sector surveys show more downside pressure vs. manufacturing PMIs

An interesting development is that manufacturing surveys are holding up better than service sector surveys across the Eurozone and in the UK. This is to be expected. A backlog of orders is likely to sustain manufacturing readings, while service sector businesses will feel the immediate effects of a cautious consumer. In the last three weeks, consumers have been battered by surging oil prices and rising expectations of rate hikes, before the war rate cuts had been expected in the UK and the US. Thus, for now, the service sector readings give us a clearer view of the economic impact from the war in Iran.

European stocks at risk

The negative effects from the energy price shock have been quick, French input cost inflation rose to its highest level since November 2023, and German input costs also rose to their highest level in 3 years. For now, corporates are not passing these onto consumers. If the situation persists then profits will be squeezed, which shows how the conflict in the Middle East may continue to pose a downside risk for European stocks for as long as oil supplies remain constrained and the Strait of Hormuz remains closed.

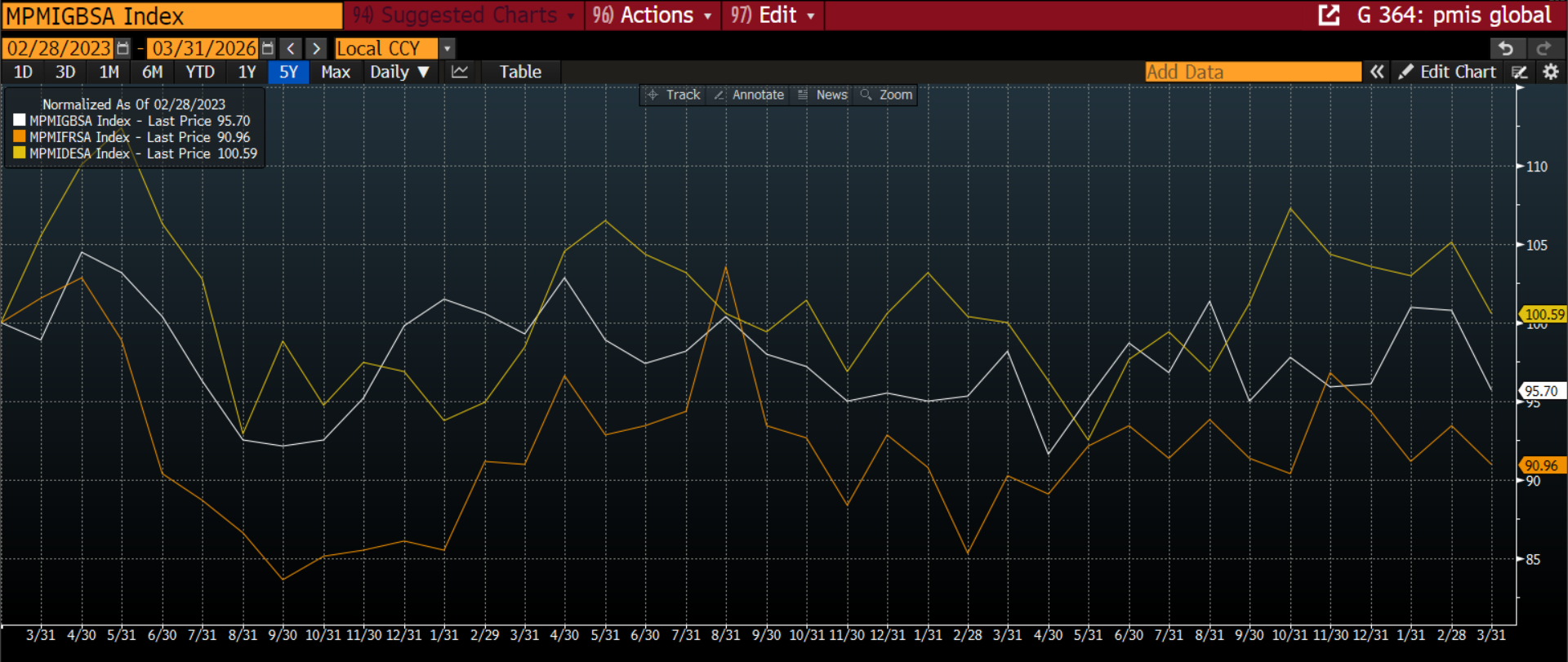

Chart 1: UK, French and German service sector PMI’s for March

Source: Bloomberg

Daily summary: Trump’s remarks give Wall Street some hope🗽 Oil hovers around $100

Oil rebounds to $100 📈Bitcoin drops below $70k

What else might we be missing from the Persian Gulf❓

📈 US500 attempts a rebound

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.