The foreign exchange market has turned defensive following a sudden escalation in the conflict between Iran and the United States. Iran’s attack on commercial vessels in the Strait of Hormuz brought an end to the month-long ceasefire that had been in place. As a result, the geopolitical risk premium has returned to the FX market, draining capital from most currencies and redirecting it toward the U.S. dollar.

Timeline of the escalation: How did the memorandum collapse?

The renewed escalation followed the sequence of events below:

-

Signing of the memorandum: Last month, the United States and Iran reached a temporary 60-day agreement. The deal guaranteed safe, toll-free passage for ships through the Strait of Hormuz in exchange for the temporary suspension of U.S. sanctions on Iranian oil exports and the launch of negotiations over Tehran’s nuclear program.

-

Iran attacks commercial vessels (beginning of the escalation): Iran violated the agreement by targeting three commercial ships transiting the Strait of Hormuz, including an LNG tanker carrying liquefied natural gas.

-

U.S. retaliation: In response to the attacks on commercial shipping, U.S. forces launched a large-scale retaliatory strike against more than 80 targets across Iran. Washington also immediately reinstated sanctions on Iranian oil trade.

-

Iranian counterattack: Tehran responded with another wave of strikes, this time targeting sites in Bahrain and Kuwait.

-

Official end of the ceasefire: Speaking to reporters during the NATO summit in Ankara, Donald Trump ended any speculation by declaring that the ceasefire was over ("as far as I'm concerned, it's over"). The President sharply criticized the Iranian leadership, calling them "scum" and "liars," effectively ruling out any near-term return to diplomacy.

FX market reversal: Risk aversion weighs on emerging-market currencies

Smaller emerging-market currencies are the biggest losers of today's session, rapidly surrendering the gains accumulated during the past several weeks of relative geopolitical calm.

The Hungarian forint is the weakest performer today (EUR/HUF: +0.85%, USD/HUF: +1.0%), falling to a two-month low against the euro and a three-month low against the U.S. dollar. However, the forint entered this new phase of the Middle East conflict from a position of considerable strength, retreating from multi-year highs reached on the back of investor optimism following Peter Magyar's party's victory in the parliamentary elections. For the HUF, the current move may represent a justified correction after most positive developments had already been priced in. Any further appreciation will likely depend on more structural improvements in the Hungarian economy, particularly stronger foreign direct investment.

Alongside the forint, the South African rand (USD/ZAR: +0.6%, EUR/ZAR: +0.4%) and the Indian rupee (USD/INR: +0.5%) are also posting broad losses. India remains directly dependent on crude oil shipments passing through the Strait of Hormuz, while South Africa relies heavily on refined petroleum products. Meanwhile, the Polish zloty is down around 0.3% against both the euro and the U.S. dollar.

Chart 1: EUR/HUF and USD/HUF exchange rates (yellow)

Source: xStation5

EUR/USD: Bears regain the upper hand

The increase in risk aversion is also weighing on the broader G10 currency complex. The only notable exceptions are the New Zealand dollar, supported by the Reserve Bank of New Zealand's recent rate hike to 2.50% and hawkish remarks from the RBNZ Governor, and the Norwegian krone, which continues to benefit from renewed upward pressure on oil prices.

The resumption of hostilities in the Middle East has effectively erased a week's worth of gains on EUR/USD. The world's most traded currency pair has declined by roughly 0.4% since yesterday and, despite relatively flat trading today, remains vulnerable to further downside. This is especially true given that the European Central Bank is unlikely to respond with the kind of reactive hawkish rhetoric that would provide meaningful support for the euro.

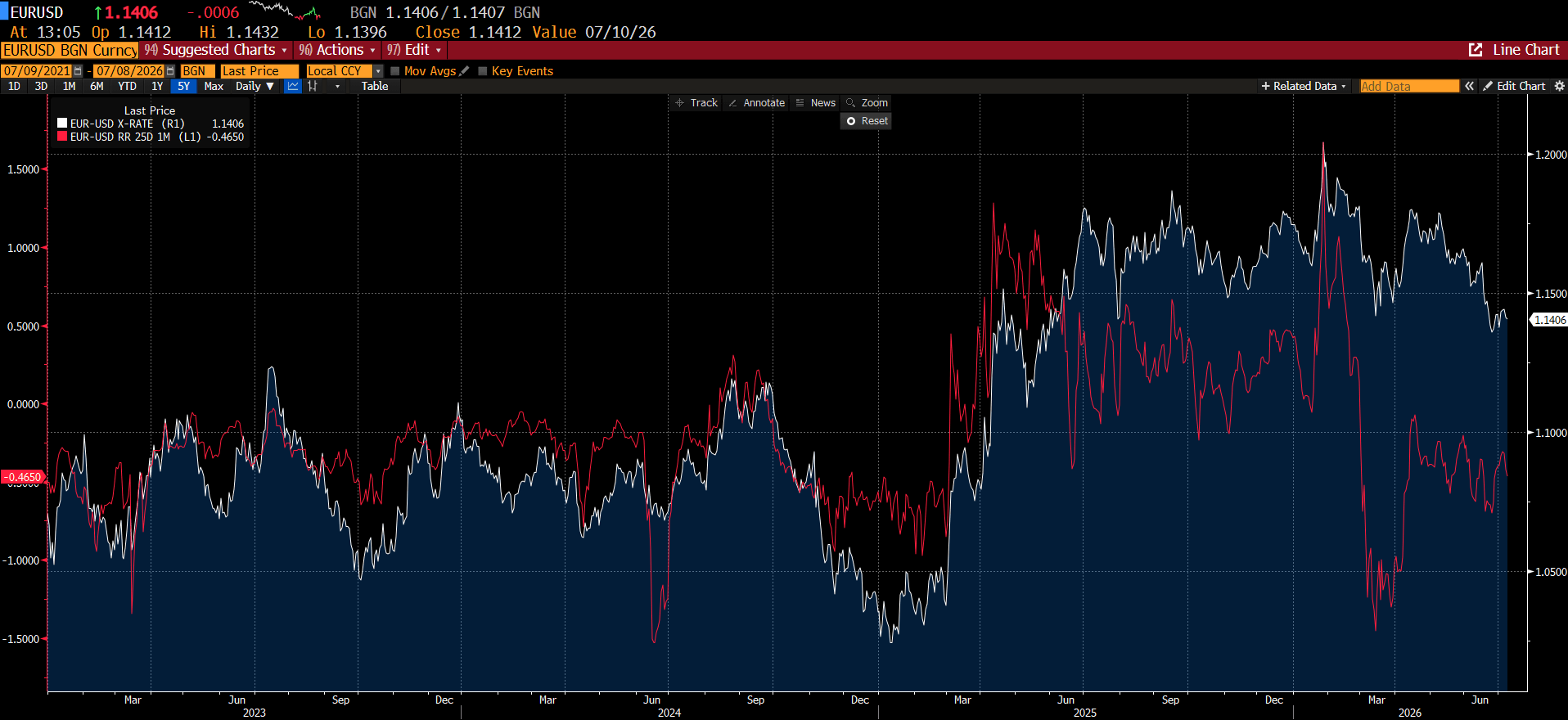

Options market participants are also increasingly hedging against further EUR/USD declines. The one-month Risk Reversal indicator has remained below zero almost continuously since March 2026, indicating that demand for EUR/USD put options exceeds demand for call options. In other words, investors are showing a greater preference for contracts that protect against further euro weakness.

Chart 2: One-month EUR/USD Risk Reversal and EUR/USD spot

Source: Bloomberg Finance LP

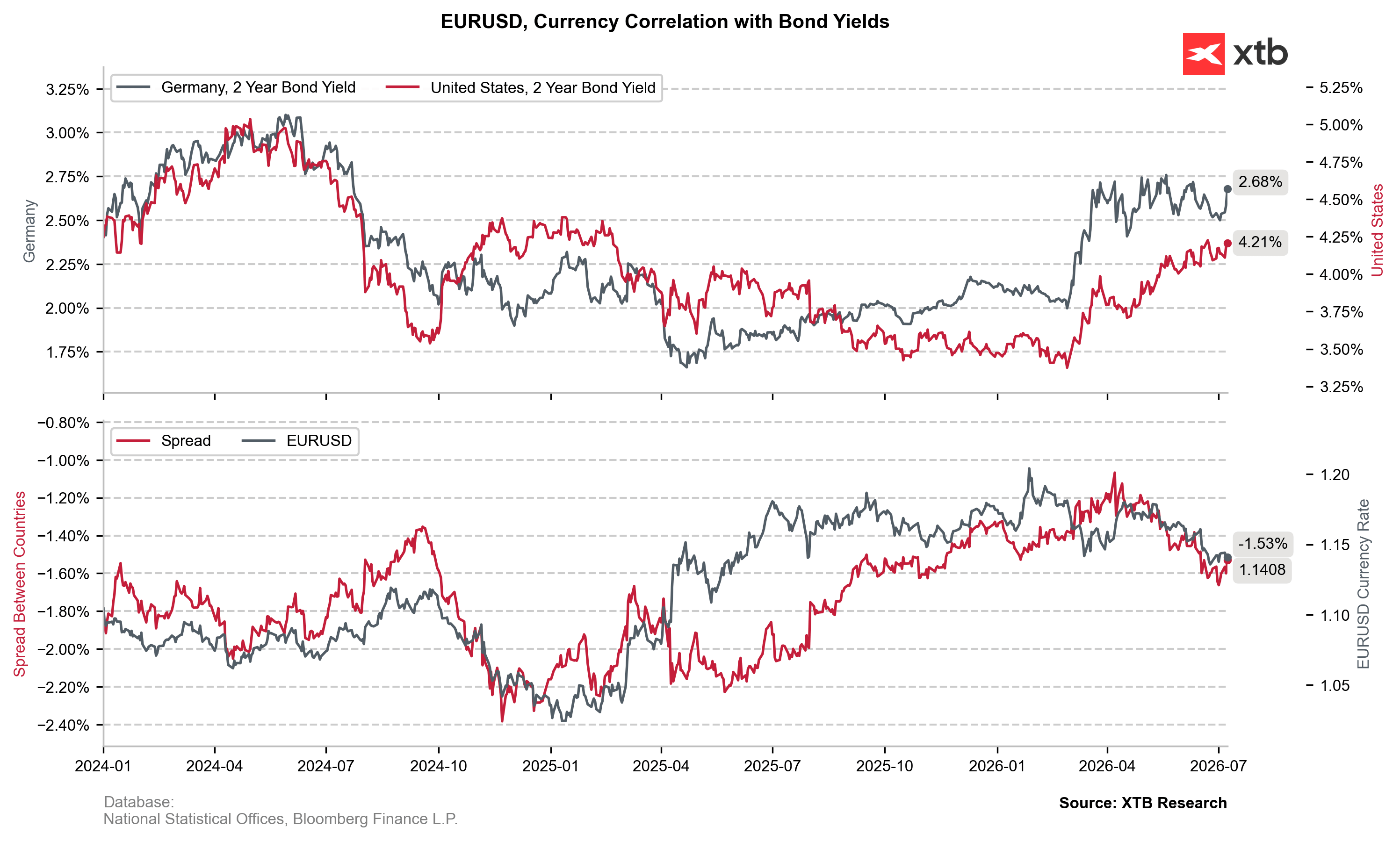

On the other hand, developments in the bond market may provide fundamental support for EUR/USD. Yields on two-year German government bonds have rebounded much more sharply (around +10 bps) than their U.S. counterparts, reflecting the euro area's significantly greater sensitivity to a prolonged energy shock. If military tensions persist over the longer term, the ECB may be forced to adopt a more hawkish, inflation-focused stance. Even without additional rate hikes, such a shift in communication could help EUR/USD defend support around 1.1400.

Chart 3: EUR/USD and the yield spread between two-year German and U.S. government bonds

Source: Bloomberg Finance LP

🛢️Will oil return to $100 per barrel? Trump points to the end of the ceasefire

Oil price surge on US/Iran

Market wrap: European stocks slide amid renewed US - Iran conflict

Chart of the Day: EURUSD Caught Between the Fed, ECB and Middle East Risks

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.