- The European session ended with gains across major indices, despite ongoing volatility in the oil market and a cautious stance from central banks. The FTSE 100 rose by 1.6% after the Bank of England kept its key interest rate unchanged. Germany’s DAX gained 1.4%, while France’s CAC 40 added 0.5% following the ECB’s decision to leave rates unchanged.

- Decisions by the ECB and the Bank of England fit into a broader pattern of central bank caution, following earlier moves by the Federal Reserve and the Bank of Japan to hold policy steady. In Asia, sentiment was weaker: Hong Kong’s Hang Seng fell 1.3%, while Shanghai indices edged up 0.1% after data pointed to a slight slowdown in China’s manufacturing activity.

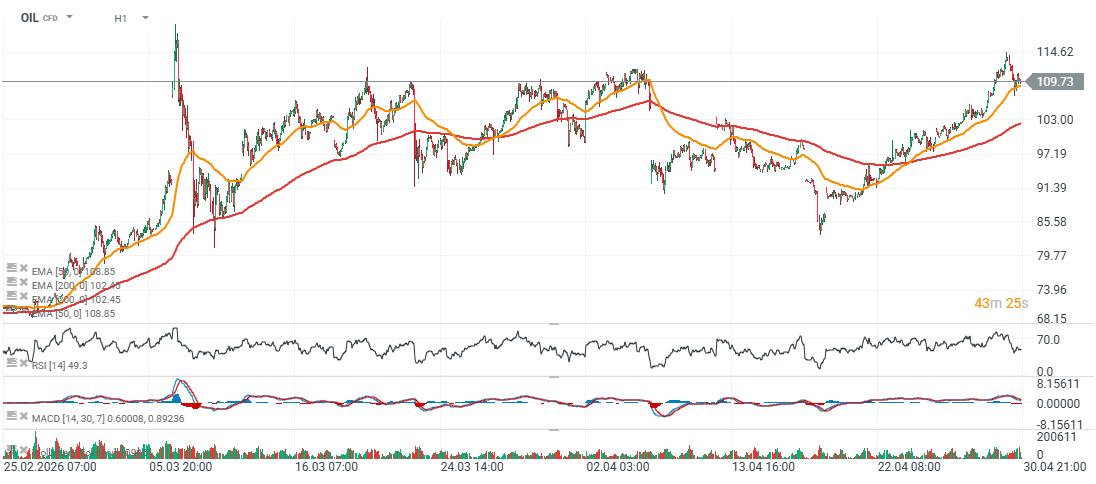

- The oil market remains highly volatile, with Brent prices surging overnight on concerns about prolonged supply disruptions linked to the war with Iran. The most actively traded July Brent contract briefly rose to $114.70 per barrel before pulling back toward $107 and stabilizing around $110.03, down 0.4%. Brent prices remain significantly above pre-war levels, when oil traded near $70 per barrel.

- Wall Street is holding near record highs, supported by strong corporate earnings despite elevated oil prices and macroeconomic uncertainty. The S&P 500 is up 0.6% and sits slightly above its record from earlier this week, while the Dow Jones is gaining 732 points, or 1.5%. The Nasdaq Composite is rising more modestly, by 0.2%, as pressure on some large-cap tech names limits the upside.

- Alphabet is gaining 7.5% after reporting earnings that nearly doubled analyst expectations. Caterpillar, Eli Lilly, and Royal Caribbean are also advancing following better-than-expected results. In contrast, Meta Platforms is down 8.9% despite strong earnings, as investors focus on higher planned capital expenditures related to AI. Microsoft is falling 5.5% after raising its capex outlook, although analysts highlight improving momentum in its Azure segment. Amazon is also down nearly 1.5% despite beating expectations, suggesting that positive earnings surprises alone may not be sufficient at elevated valuations.

- US Treasury yields are easing as oil prices pull back, with the 10-year yield declining to 4.39% from 4.42%. US macro data showed slower-than-expected growth acceleration in Q1, while inflation metrics for March deteriorated broadly in line with expectations. Labor market data remain relatively strong, with initial jobless claims declining, indicating limited layoffs despite announced workforce reductions by some companies.

- Gold and silver are posting solid gains in response to a weaker US dollar, while EURUSD is rising more than 0.5% toward 1.173. Bitcoin is advancing more cautiously and remains near $76,000, suggesting a still-limited risk appetite in the crypto market.

OIL (H1 interval)

Source: xStation5

Technical analysis 📈 Gold gains 1.5% amid weakening US dollar

📈 EURUSD gains 0.5%

US Open: Wall Street gains lose momentum 📉 Caterpillar shares rally after earnings

Oil price retreat from high, as FTSE 100 surges and UK yields fall

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.