02:30 PM CET, United States, NFP report for March:

-

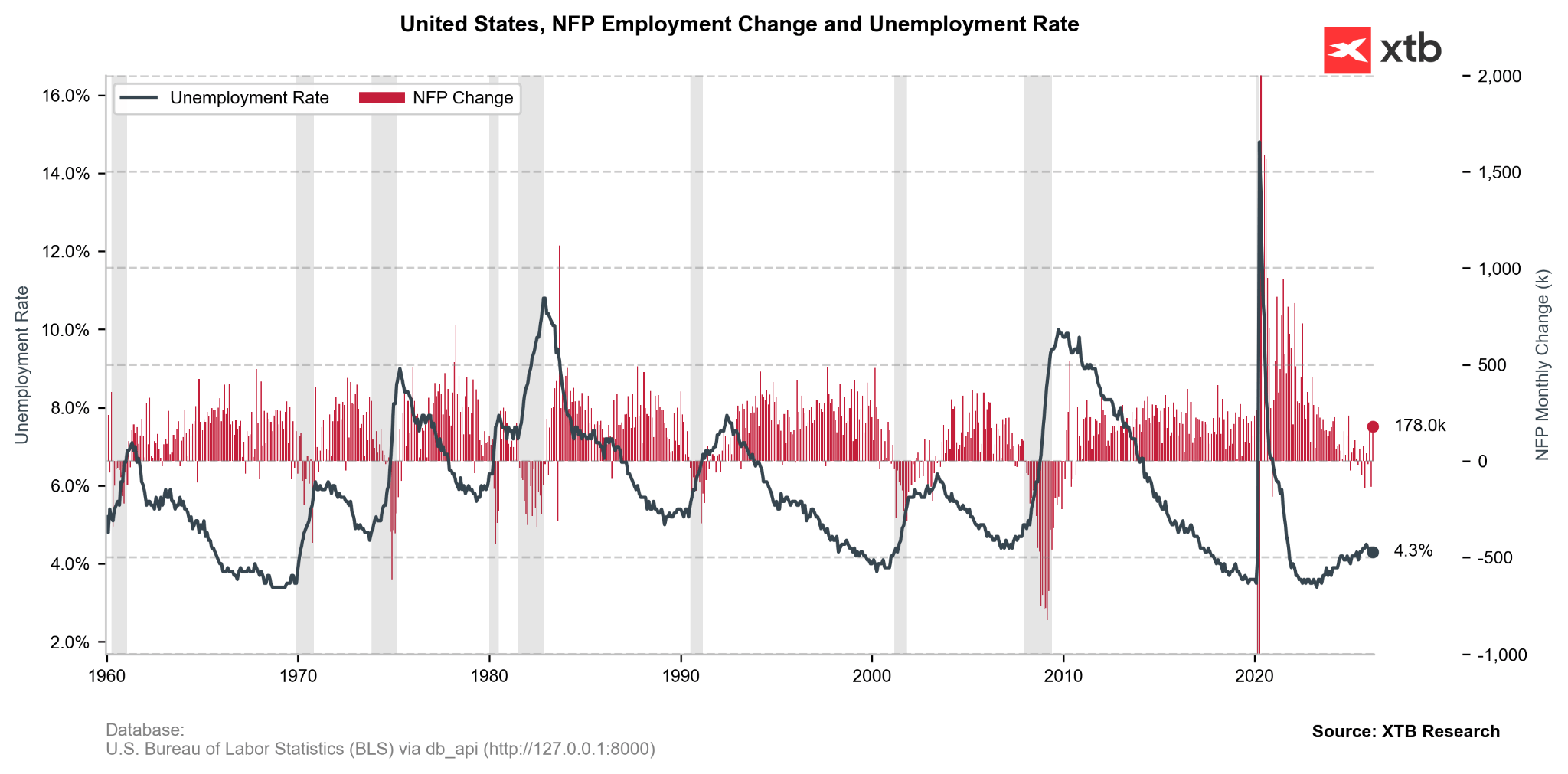

Nonfarm Payrolls Actual 178k (Forecast 65k, Previous -92k)

-

Private Payrolls Actual 186k (Forecast 78k, Previous -86k)

-

Government Payrolls Actual -8k (Previous -6k)

-

Manufacturing Payrolls Actual 15k (Forecast -5k, Previous -12k)

-

-

Unemployment Rate Actual 4.3% (Forecast 4.4%, Previous 4.4%)

-

Labor Force Participation Actual 61.9% (Forecast 62%, Previous 62.0%)

-

Average Earnings YoY Actual 3.5% (Forecast 3.7%, Previous 3.8%)

The latest NFP report delivered stunning headline numbers, though substantial revisions to the previous two months highlight ongoing data volatility and a "foggy" outlook for the economy walking into a supply energy shock.

The Highlights:

-

Massive Beat: Total payrolls crushed expectations, exceeding the consensus by nearly 3x. This surge more than compensated for last month’s negative reading.

-

Unemployment Drop: The closely watched unemployment rate unexpectedly ticked back down to 4.3%.

The Gloomy Side:

-

Participation Slump: The labor participation rate decreased unexpectedly.

-

Discouraged Workers: There was a significant spike of 144,000 "discouraged workers" (those who have stopped looking for work believing no jobs are available).

-

Slower Wage Growth: Average hourly earnings slowed more than anticipated. This suggests that despite the "stunning" headline job numbers, workers may be losing their bargaining power—likely feeling less confident about demanding raises amidst the current geopolitical and economic uncertainty.

-

The Fed's "Breathing Room": From a monetary policy perspective, this is a silver lining. It suggests that the energy price shock (driven by the Iran conflict) might not immediately trigger a "wage-price spiral," potentially giving the Fed some room to maneuver.

-

The Stagflationary Threat: However, there is a flip side for the consumer. If wage growth stalls while energy and food prices remain elevated, we face a stagflationary bottleneck. Persistent price pressure combined with weakening purchasing power could severely crimp long-term consumption.

-

-

Mixed Revisions: Revisions were a mixed bag. January was revised up to 160k, while February was slashed to -133k. The combined net effect for those two months is 7k lower than previously reported.

EURUSD (M30)

The immediate reaction brought EURUSD sharply down, as raw data pushed markets to trim their bets on Fed cutting interest rates in 2026, supporting the US dollar. The price later settled at approx. 1.1530, with details proving challenging to navigate the US economic outlook. The pair is down margianlly from yesterday's close (-0.05%).

Source: xStation5

Three Markets to Watch in the Week Ahead (03.04.2026)

Daily Summary: A Lull in the Pre-Holiday Calm

Market wrap 📌US indices in focus amid strong NFP data and $100 oil

EURUSD catches breath before NFP 📈

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.