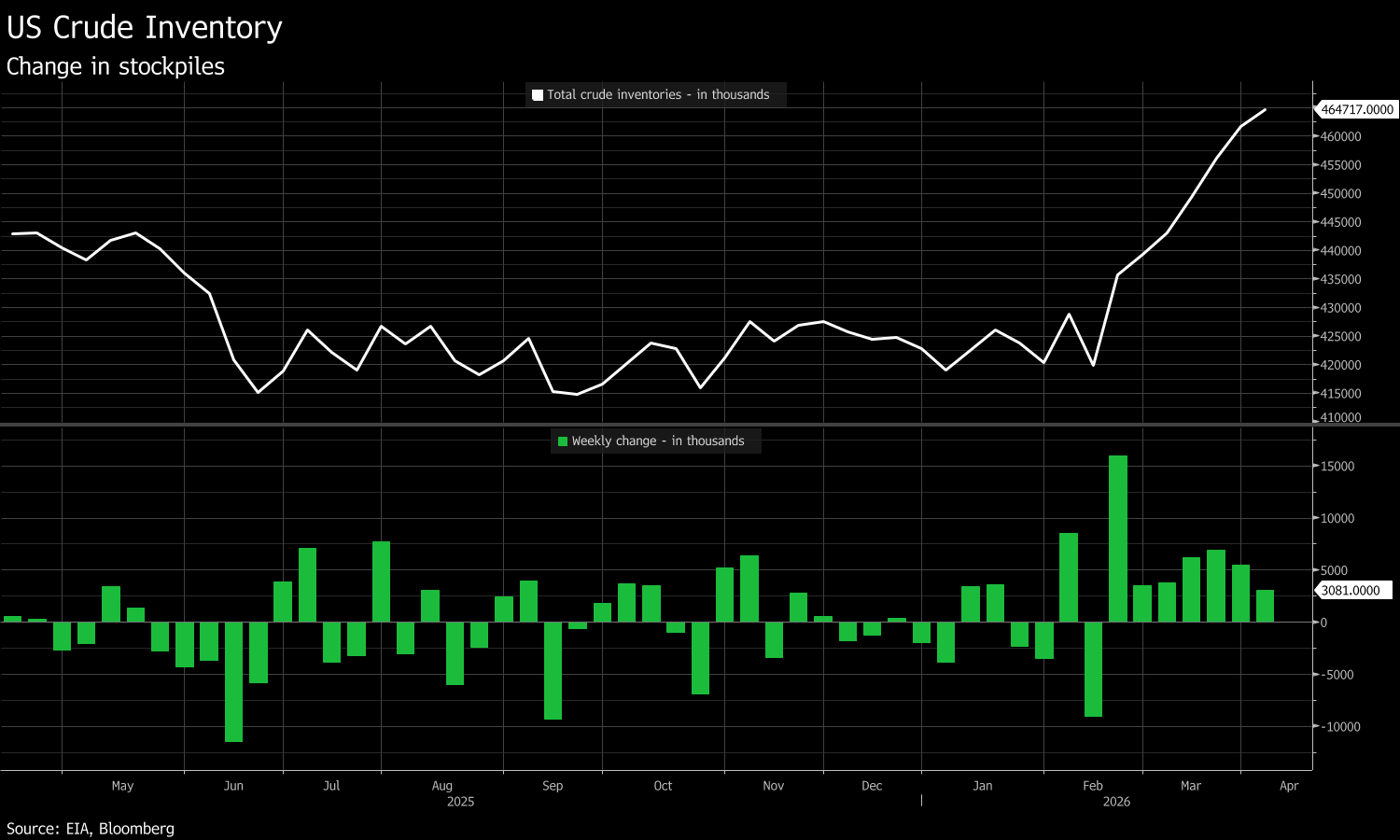

- Crude oil inventories: +3.08 million barrels (expected: +0.5 million). This is a significant increase, exceeding the market consensus by more than sixfold (Bloomberg).

-

Distillate inventories: -3.14 million barrels (expected: -1.25 million). A very deep decline, suggesting strong demand for diesel and heating oil or production issues.

-

Gasoline inventories: -1.59 million barrels (expected: -1.55 million). The result is almost perfectly in line with expectations, indicating stable seasonal demand.

-

Refinery utilization: -0.1 percentage points (expected: +0.8 percentage points). A surprising drop in refinery activity, which partially explains the rise in crude oil inventories (unprocessed crude).

-

Imports from Mexico: -59% (drop to 165k b/d). This is a historically low level, resulting from Mexico's policy of limiting exports in favor of its own refineries (including Dos Bocas).

This marks the 7th consecutive increase in U.S. crude oil inventories. Source: Bloomberg Finance LP, XTB

Crude is piling up, but fuels are depleting

The EIA report paints a picture of a "two-speed" market, which, in the context of the recently announced ceasefire between the US and Iran, may further complicate valuations:

-

Supply shock in raw material: The increase in oil inventories by over 3 million barrels at a time when the market expected a symbolic rise is a bearish signal. This results mainly from lower refinery throughput (utilization) and solid imports from Canada, which cushioned shortages from other directions. We have observed a continued strong increase in inventories over recent weeks.

-

Distillate crisis: While crude oil is increasing, stocks of finished fuels (especially distillates) are melting away rapidly. This is a bullish signal for refining margins. The product market remains extremely tight, which may prevent fuel prices at gas stations from falling, even if the price of Brent crude itself plummets in response to the truce.

-

Mexican "detox": The drastic drop in imports from Mexico (by 233k b/d) is a structural change. The US must look for heavy crude elsewhere (e.g., the increase in imports from Venezuela to 321k b/d), which increases logistical costs for refineries in the Gulf Coast (PADD 3).

-

Geopolitical context: These data hit the market just as the "war premium" is evaporating following the April 7 truce. The oversupply of crude in the US (+3 million bbl) gives the Trump administration an additional argument in negotiations—America is showing that it has reserves, which weakens Iran's negotiating position regarding the Strait of Hormuz.

-

Release of reserves: Since March 20, only 2 million barrels of oil have been released from the Strategic Petroleum Reserve (SPR), despite an announced release of as much as 172 million barrels.

It is worth emphasizing that oil is reacting today to issues concerning Iran. The latest news indicates that Iran demands Israel stop attacking Lebanon. Without a cessation of attacks, Iran would reportedly decide to abandon the ceasefire quite quickly.

Daily Summary - Crude oil below $100 amid ceasefire

BREAKING: Outdated "hawkish" minutes fail to move the dollar

➡️EURUSD below 1.17 ahead of FOMC Minutes

Iran threatens to end ceasefire, as markets remain sensitive to news flow

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.