The private credit and private equity markets are not new, but what is relatively new is how they are perceived and how visible they have become to the broader market. Today’s issues in this segment stem partly from that shift.

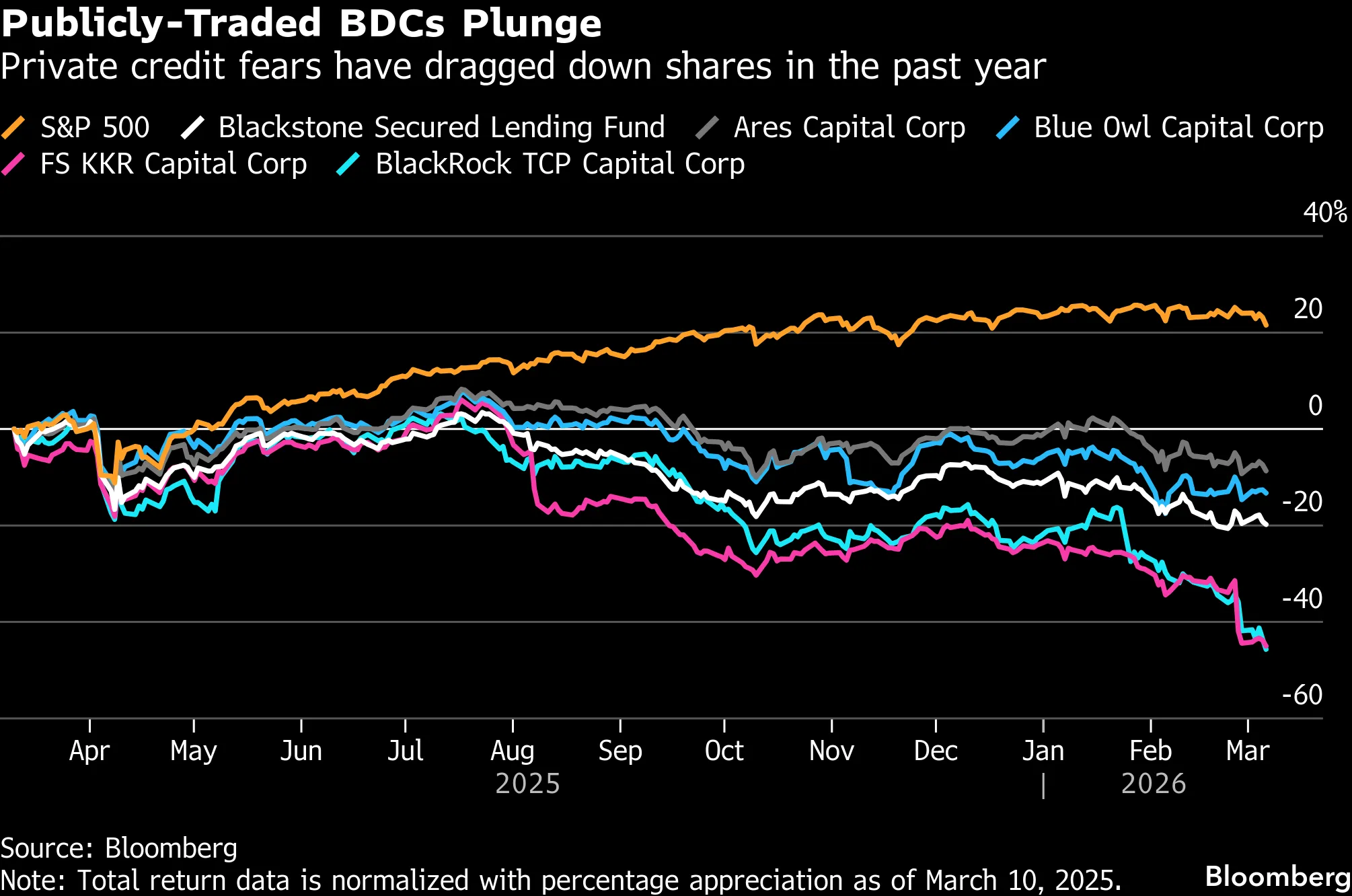

Private credit/private equity firms have seen significant declines in recent months. BlackRock, the world’s largest asset manager, has already lost over 20% of its valuation over the last two months. This is not an isolated case, but a clearly sector-wide trend.

Source: Bloomberg Finance LP

Where are the declines and rumors coming from?

Private equity and private credit firms are known for several things. Among their key characteristics are a lack of transparency and oversight comparable to what is required of other institutions, as well as an above-average tolerance for risk. Risk combined with weaker oversight is, more often than not, a mix that can be disastrous for valuations.

At this stage, however, one should not expect an inevitable financial crisis, as a large part of the market seems to do. The decline in valuations is primarily a reassessment of a business model that had come to rely on assumptions that cannot hold, combined with a meaningful degree of overinterpretation by some market participants.

A series of events, such as limiting redemptions from funds by companies like BlackRock or Blue Owl, or occasional markdowns of assets held in funds, has fuelled concerns about liquidity and asset quality.

The point is that this is a correction in perception, not necessarily in the underlying assets themselves.

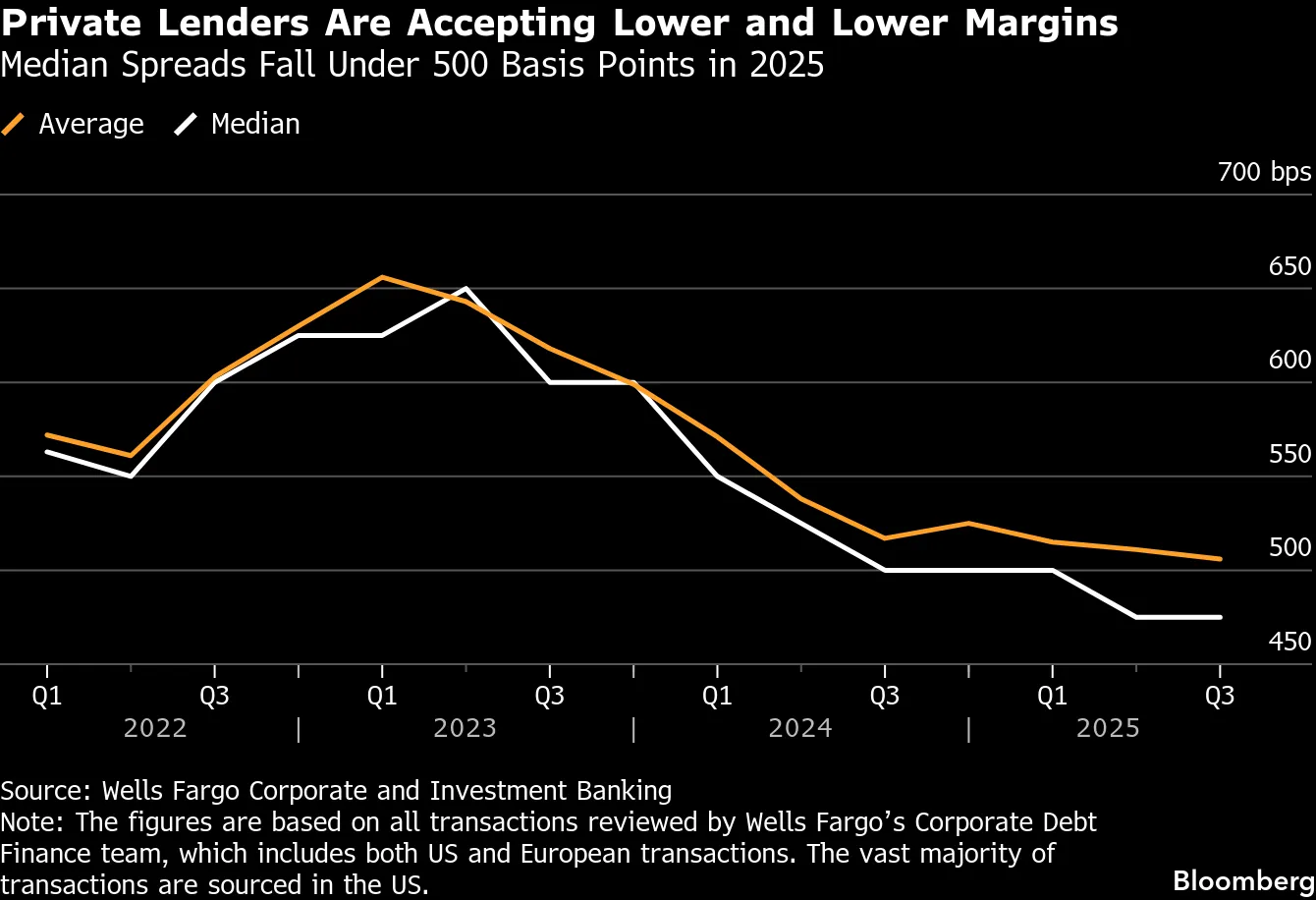

The private credit/private assets market and its investors tried to pretend this was a capital allocation method “like any other”: without meaningful risk or constraints, but with higher returns. Unfortunately, that’s not how markets work. Private credit and private assets are now showing their true nature: the market is illiquid by design, and the holdings on these funds’ balance sheets are often there for a reason.

Source: Bloomberg Finance LP

This repricing of risk is also reinforced by technology exposure. As Finch reports, PC/PE firms may have significantly higher exposure to technology companies than they disclose to clients. Tech valuations do not, in themselves, signal an imminent collapse, but the market’s perception of risk is fundamentally different, and higher risk requires higher compensation.

Paying for risk is the core fundamental justification for the declines. These firms turned out to be riskier in many ways than investors initially assumed. After the fact, investors are demanding higher returns or seeking to withdraw capital, both of which clash with the structure and strategy of most funds in this sector.

Where is the biggest problem?

The biggest issue concerns BlackRock and Blue Owl, not because these companies show any signs of illiquidity or imminent failure, but because they must deal with the consequences of expanding the market beyond reasonable limits by (mainly) enabling retail investor exposure to products whose risk profile is fundamentally incompatible with the nature of “private” market investments.

It’s time to look at the metrics. BlackRock’s current P/E is around ~26, compared to the S&P 500’s ~28. Its dividend yield is about 2.5% (paid quarterly), and its gross margin exceeds 47%. Many things can be said about BlackRock, but it cannot reasonably be called overvalued or “in crisis.”

Finally, it’s worth remembering the scale of the company and its potential “problems.” BlackRock manages $14 trillion in assets. The private credit market totals roughly $3–5 trillion, while the entire private assets market is around $10–20 trillion, bearing in mind that parts of these markets overlap.

If the market were pricing in a loss of value across most of the firm’s assets on a scale that could threaten liquidity, derivatives markets would be showing something close to Armageddon. Nothing like that is happening. Expectations are stable, volatility is moderate, and CDS remain at their typical, still low, levels.

Daily summary: Week ends with Brent at 100$ and indices in the red

AUDUSD loses nearly 1% 📉

Three markets to watch next week (13.03.2026)

Amazon: The Beginning of the End of AI Dreams?

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.