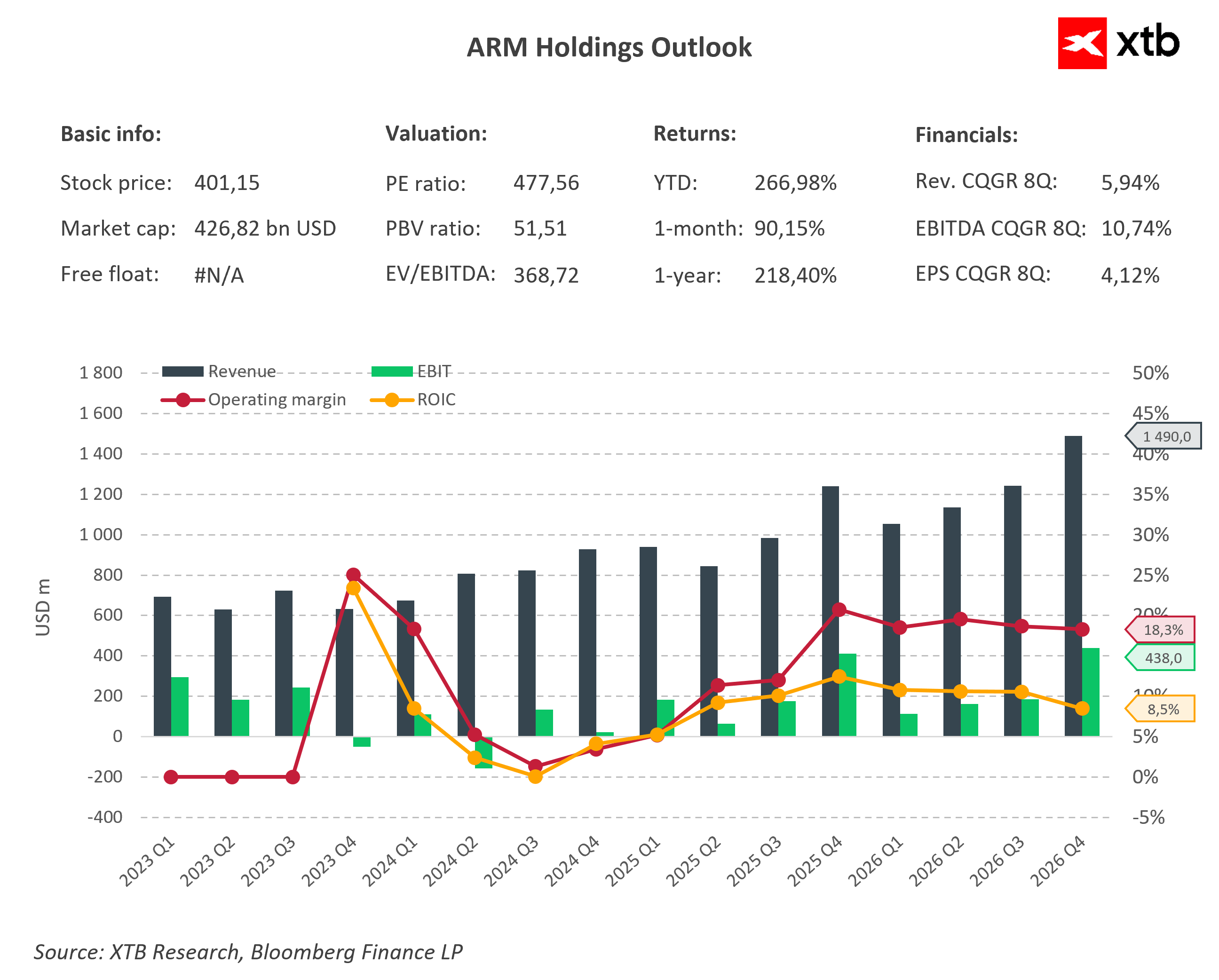

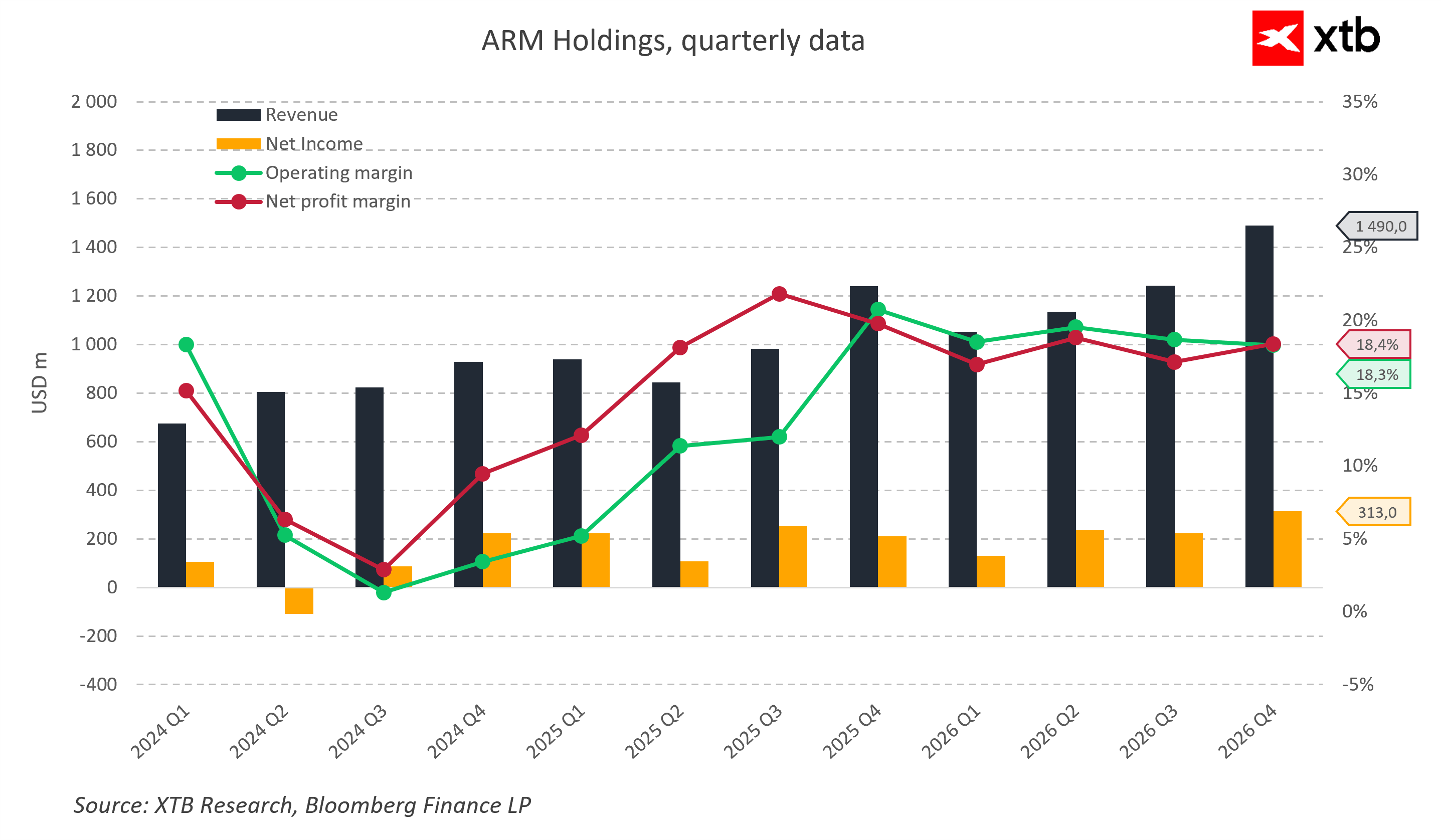

The information shared by ARM Holdings CEO Rene Haas clearly indicates that the company has reached a pivotal turning point in its history. The firm is no longer perceived solely as an architecture designer for integrated circuits, but is instead becoming a fully fledged participant in the artificial intelligence chip market. The declaration that the target of reaching $15 billion in revenue from its own chips will be achieved much earlier than anticipated completely rewrites the current market narrative. It demonstrates that investors may have significantly underestimated the pace of this transformation until now. Massive demand driven by the artificial intelligence revolution is rapidly accelerating the commercialization of this new business segment, translating into tangible and highly optimistic expectations for future margins and cash flows.

The foundation of this market story lies not only in the success of the new product business, but above all in the unprecedented scale of ARM architecture adoption across the world's largest data centers. The largest global cloud computing providers, including AWS with its Graviton processors, Microsoft Azure deploying the Cobalt chip, Google Cloud with the Axion solution, as well as Oracle and Alibaba Cloud, are already building their core infrastructure on British technology. This means that these solutions have ceased to be merely an interesting alternative to traditional x86 architecture and have become a strategic element in the plans of tech giants. In mid-2026, these corporations are investing hundreds of billions of dollars in artificial intelligence infrastructure, and a significant portion of these massive budgets is indirectly flowing through licensing fees and the ecosystem tied to ARM.

The market introduction of a new central processor called the AGI CPU represents the second, critical piece of this puzzle. For the first time in its 35-year history, the company has decided to launch production of its own, finished chip instead of limiting itself exclusively to selling intellectual property rights. Meta has become the first major customer for this innovative processor, and other entities have quickly joined the ranks of early business partners. This selection of counterparties proves that ARM does not intend to operate in isolation, but is instead consistently building a powerful technological alliance around its new product. The AGI CPU itself was designed specifically for AI agents, meaning systems capable of operating fully independently as virtual assistants that execute complex tasks without continuous human intervention.

Official specifications show that the new chip offers more than 2-fold higher performance per server rack compared to x86 solutions, which directly translates into lower internal costs and a significantly higher compute density in modern data centers. This drastic energy advantage is becoming a key argument at a time when data centers are grappling with astronomical power bills and transmission capacity limits. When cloud providers are forced to buy tens of thousands of processors for their servers, higher energy efficiency generates savings reaching tens of millions of dollars annually. This makes ARM technology simply impossible for modern businesses to ignore.

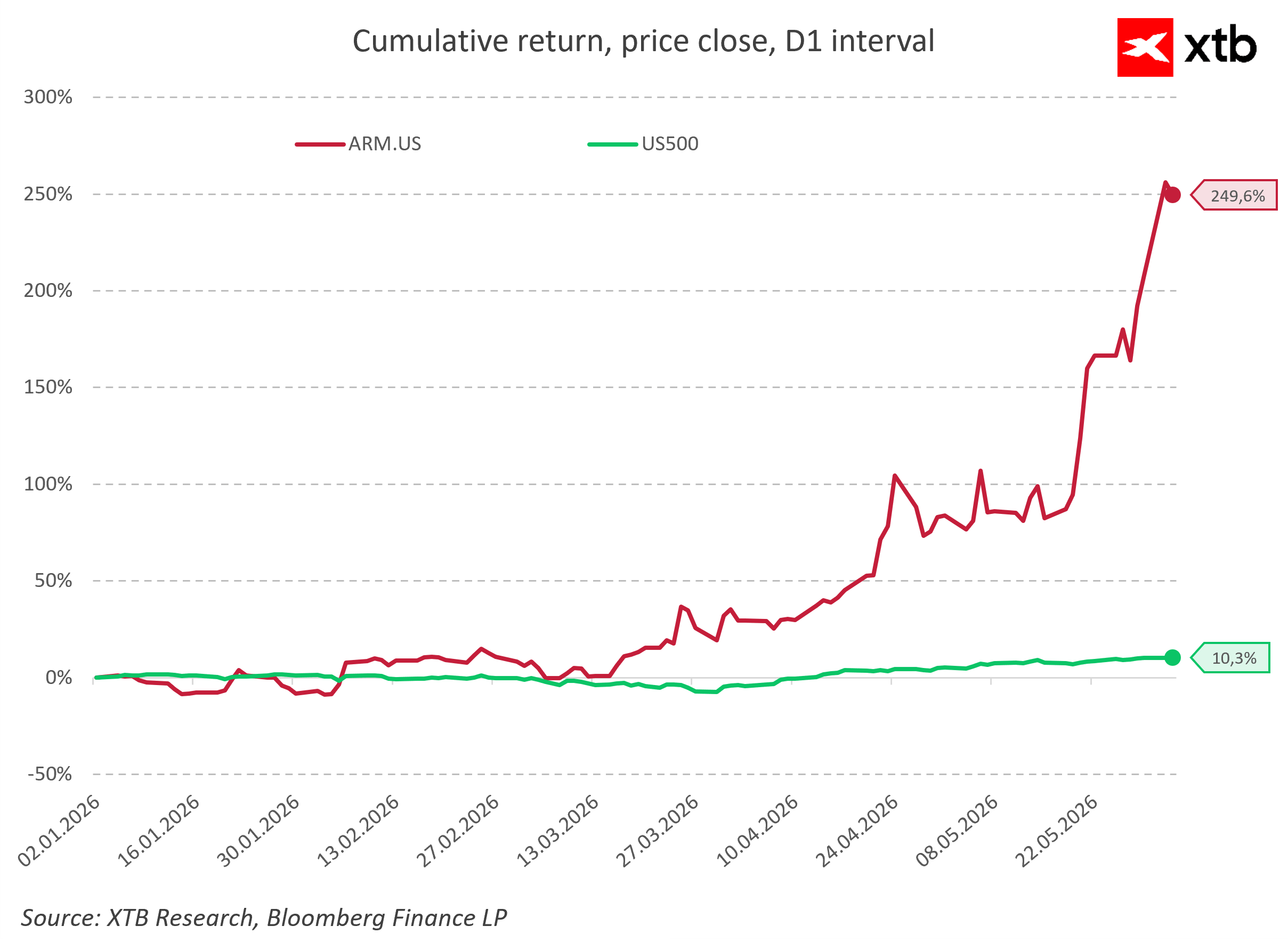

The market reaction suggests that investors are very quickly beginning to price in a profound shift in the company's business model. A business that used to be associated with high margins but stable, limited volume growth is now becoming a direct beneficiary of the entire value chain in the artificial intelligence sector. Revenue will no longer be generated solely from licenses and royalties, but from the sale of its own physical silicon. Crucial to the stock market valuation is the fact that direct sales of advanced chips carry an incomparably greater financial potential, which fully justifies higher valuation multiples in the long run.

However, caution is warranted, and one must remember that the current stock market success relies heavily on promises, with forecasts being highly forward-looking in nature. The future of this segment depends on many variables, among which the most critical risks remain the pace of software adaptation, compatibility with existing systems, and the ability to efficiently scale mass production. ARM is also entering into a direct clash with giants like NVIDIA, AMD, and Intel. Furthermore, transitioning from a safe intellectual property sales model to a complex manufacturing business drastically increases operational complexity and capital requirements, and the market may need several more quarters to gain confidence that this model is stable.

The ultimate balance of rewards and risks shows that ARM is emerging as one of the most important winners of the current tech boom. The company is not only providing the foundations for other players' systems, but is actively and successfully building its own product arm. Widespread adoption of the technology by cloud market leaders and contracts with entities such as OpenAI or Meta realistically increase the chances for a rapid monetization of the entire ecosystem. The fact that financial forecasts are being revised upward so early may be a clear signal that the phase of strongest growth lies ahead. Investors should now closely follow quarterly reports, as they will ultimately determine whether the company permanently joins the top ranks of AI infrastructure providers, or whether Wall Street's expectations have turned out to be overextended.

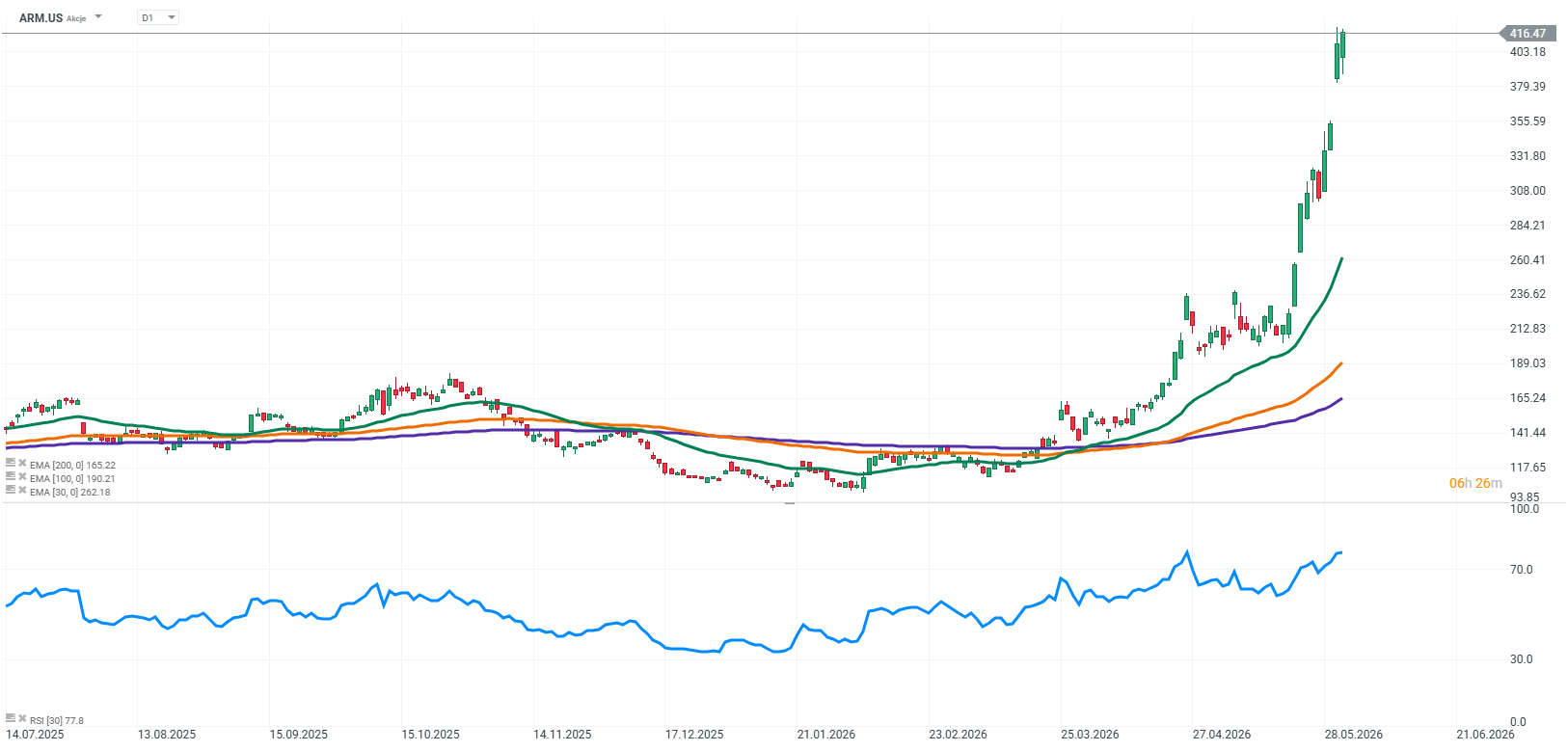

Source: xStation5

Daily Summary: The Two Faces of AI – Market Fuel and Costly Burden

AI War: Nvidia's Chinese Paradox and the Myth of Technological Decoupling

US Open: Wall Street loses momentum as AI costs and Middle East tensions cool sentiment

Marvell Technology Anointed by Nvidia as the Next Chip Giant!

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.