Accenture shares are down around 15% in pre-market trading following the publication of its Q2 2026 results. Although the company beat market expectations on earnings per share and delivered a full-year outlook better than consensus, the stock is falling.

The negative investor reaction was mainly triggered by a series of large acquisitions in the cybersecurity sector. The market is currently bearish on cybersecurity, assuming that further AI development will make the industry lose its relevance.

Earnings

- Revenue came in at $18.7bn, below the consensus of about $18.8bn, but still 6% higher y/y.

- EPS was $3.80 versus $3.72 expected.

- New bookings totaled $19.3bn, compared with $19.7bn a year earlier.

- Operating margin increased by 20 basis points to 17.0%.

Guidance

- The company now expects full-year EPS of $13.78-$13.90, versus market expectations of $13.80.

- Accenture also expects FY 2026 revenue growth of 3-4%.

- Free cash flow guidance was maintained at $10.8-$11.5bn.

Controversial purchases

The transactions announced alongside the results drew the most market attention. Accenture announced plans to acquire a majority stake in Dragos and to acquire runZero and NetRise in full.

The combined enterprise value of these transactions is about $4.17bn. Closing is expected in August or September 2026, subject to regulatory approvals.

Accenture’s management presents these deals as a strategic strengthening of its position in operational technology security (OT Security). CEO Julie Sweet said the acquisitions are intended to increase the company’s market share and create a new growth platform.

The market, however, sees the purchases mainly as short-term pressure on results and large spending on a sector viewed as lacking strong prospects. Integration of the new businesses into the company’s operations is also being questioned.

Context

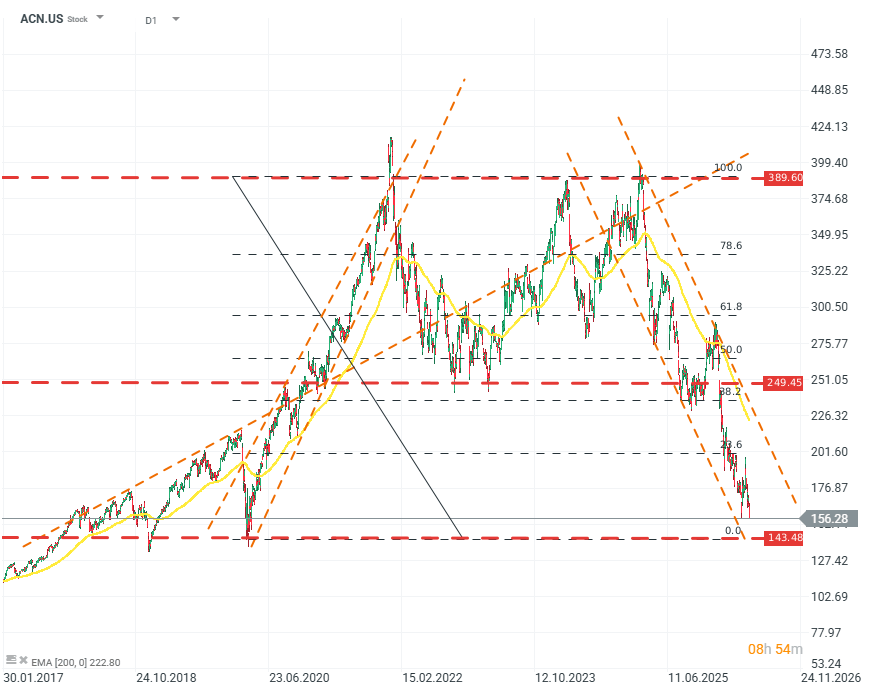

ACN.US (D1)

From a valuation perspective, the company has not had a good period. It is now trading close to the valuation levels seen at the bottom of the sell-off during the market’s reaction to the COVID-19 pandemic. From its peak, the company has lost more than 70% in valuation, and 40% in valuation this year alone. Importantly, profits and profitability do not indicate a decline or a significant loss of growth momentum. The company has reached a P/E of 13 and a price-to-sales ratio of 1.4. Source: xStation5.

Morning Wrap – Market Returns to Normalcy After Hawkish Fed Forecasts and a Mixed Warsh (11.08.2026)

Daily Summary - Oil Nearly Erases War Gains as Wall Street Pulls Back Ahead of Fed Decision (16.06.2026)

US OPEN: SpaceX pushes Amazon off the TOP 5 podium. Wall Street awaits Warsh's debut

OpenAI heads into a price war ahead of an IPO?

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.